DEEP RESEARCH · PANSTAR ENTERPRISE

PanStar Enterprise: Structural Pivot into Green Marine EPC

A special-situation review of the shift from Hesbon auto-service equipment to ship engineering and retrofit EPC

0. Bottom Line First

PanStar Enterprise is a special-situation case: a low-growth auto-service equipment company trying to become a green ship-engineering EPC company. The merger and regulation momentum are real, but working capital, CB dilution, and lock-up shares make the thesis hard.

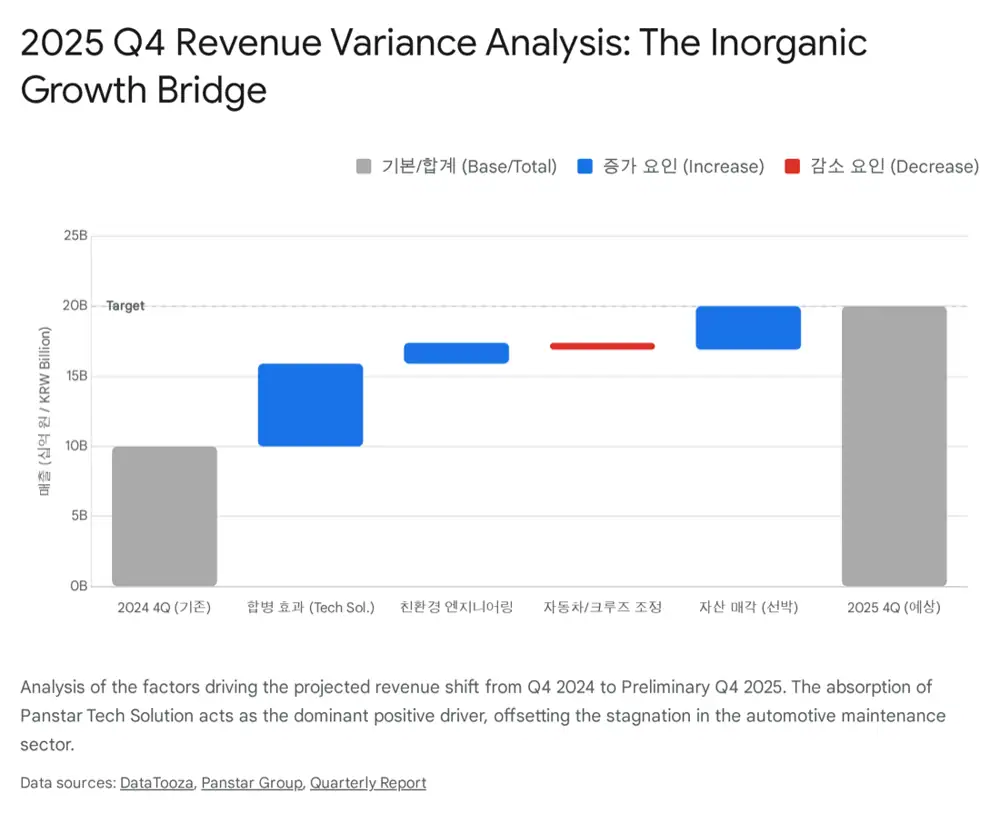

- The merger with PanStar Tech Solution was completed in May 2025, so 4Q fully reflected ship engineering and green retrofit operations.

- PanStar Tech Solution is described as having generated about KRW 23.6bn in annual revenue and around KRW 2.7bn in operating profit before the merger.

- The surge in net income was heavily affected by one-off gains on asset sales such as the Sanstar Dream vessel, so adjusted operating profit and OCF matter more.

- The core overhangs are the 24th CB with KRW 8.0bn outstanding, conversion price lowered from KRW 696 to KRW 666, convertible shares rising from about 11.49mn to 12.01mn, and about 38mn merger shares under lock-up.

1. 4Q 2025: Merger Effect and Earnings Optical Illusion

Official fact: PanStar Tech Solution was an unlisted affiliate specializing in ship engineering and green retrofit, and the merger was completed in May 2025.

Engineering revenue is project-based. Year-end milestone billing often concentrates revenue in Q4, so the Q4 revenue uplift reflects not only seasonality but a structural level-up from manufacturing into professional EPC services.

Interpretation: The problem is that revenue growth and recurring earnings power are not the same. The source says net income jumped more than 1,000% year on year mainly because of gains on selling vessels such as Sanstar Dream. Cash inflow helps the balance sheet, but it is not recurring profit.

- Operating-profit pressure came from lower cruise profits, raw-material and labor inflation, added engineering headcount, higher ship-equipment prices, and possible merger-related accounting costs.

- The IMO's one-year delay in discussing mid-term greenhouse-gas measures also weakened shipowner retrofit sentiment, limiting 4Q growth versus aggressive expectations.

2. Portfolio: Auto Equipment and Marine EPC

Auto-Service Equipment

Started as Hesbon Machinery in 1991. It makes auto lifts, wheel-alignment equipment, and tire changers, and is registered as a supplier to Hyundai Motor and Kia.

Green Retrofit EPC

Provides scrubbers, BWTS, and future ammonia/methanol engine-conversion solutions on a turnkey basis.

225+ Vessel References

The merged Tech Solution engineering team and more than 225 execution references are presented as entry barriers.

The auto-service equipment unit faces EV-related service-demand risk and delayed new-equipment spending in weak cycles, but it generates stable cash used to fund marine engineering. The marine engineering unit became the core identity after diversification in 2016 and the 2025 merger.

The cruise and logistics businesses include Busan One Night Cruise and PIEX express cargo logistics. They can benefit from post-pandemic travel recovery but are more volatile because of their B2C exposure.

3. Cash Flow and Financial Structure

| Item | Source observation | Investment read |

|---|---|---|

| 2023 OCF | Positive cash flow from stable auto-service equipment collection | Legacy defensive value |

| 2024-2025 OCF | Operating cash flow weakened or turned negative | EPC orders first create working-capital burden |

| Working capital | Upfront raw-material purchases, receivable timing gap, related-party receivables | Need to check gap between book profit and cash inflow |

| ICF | Gimpo factory land, ship acquisition for leasing, merger cost, R&D | Growth investment with cash burn |

| FCF/CFF | Repeated CB/BW issuance and more short-term borrowing | External funding and dilution risk |

Interpretation: PanStar is burning cash to secure engineering capability. This becomes sustainable only if order backlog converts into cash inflow after 2026.

4. Governance and Overhang

| Item | Source figure | Meaning |

|---|---|---|

| Largest shareholder Kim Hyun-gyeom | About 18.66% as of end-September 2025 | Strong owner control |

| PanStar Co. | 8.63% | Affiliate cross-shareholding |

| PanStar Line.com | 4.44% | Possible affiliate-risk transmission |

| Co-CEO Kwon Jae-geun | 8.61% | KR-trained engineering expert, symbol of the business shift |

| 24th CB | KRW 8.0bn outstanding | Dilution expands when conversion price falls |

| Conversion price | KRW 696 → KRW 666 | Convertible shares about 11.49mn → 12.01mn |

| Merger shares | About 38mn shares | One-year lock-up from listing; mid-2026 release burden |

Official fact: A significant share of revenue comes from affiliates such as PanStar Line.com. The captive structure provides stable revenue through ship management, ship supplies, and engineering services, but it also raises related-party transaction and transfer-pricing transparency issues.

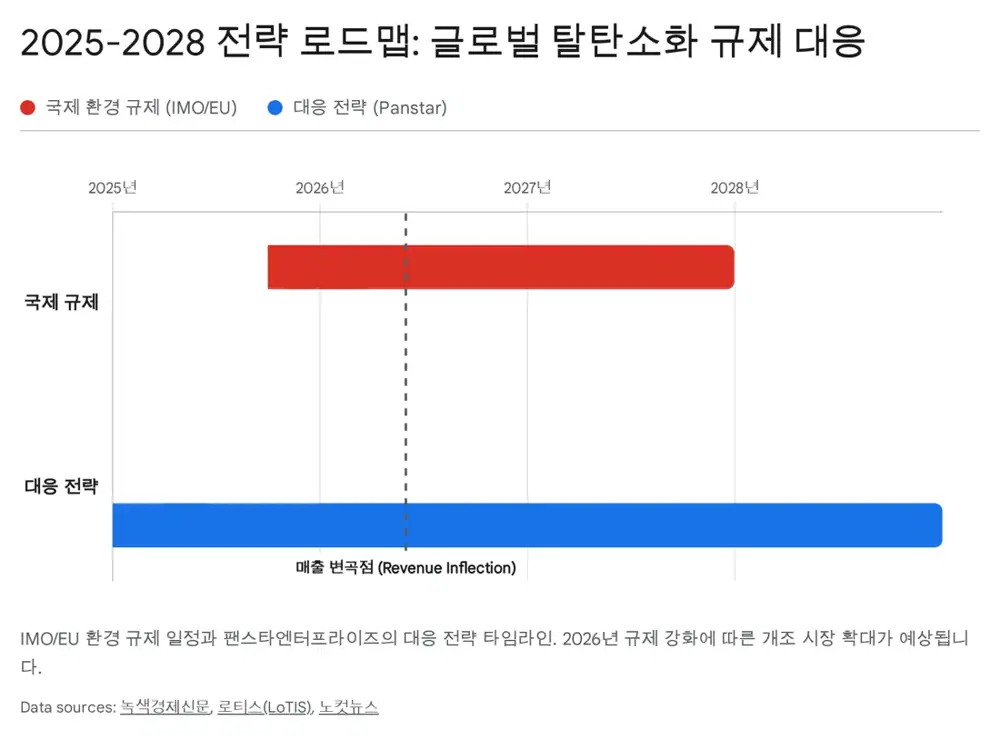

5. Competition and 2026-2028 Roadmap

In auto-service equipment, PanStar competes with small domestic firms and low-cost Chinese equipment. In marine engineering, HD Hyundai Marine Solution is the dominant provider of large-vessel total solutions. PanStar targets the middle zone: vessels too small for large shipyards but too technically complex for ordinary repair yards, using PanStar Group vessel references to approach mid-sized Japanese and Southeast Asian shipowners.

- IMO 2050 net-zero and the 2030 interim target require carbon reduction from ships already in operation.

- The CII system grades ships A-E and pressures D/E-rated vessels toward scrapping or green retrofit.

- EU ETS has included shipping since 2024, making carbon cost explicit for Europe-calling vessels.

- Korean government support for green ship technology, retrofit industry, defense encryption projects, and autonomous-ship R&D is cited as a policy tailwind.

6. Scenarios and Final View

Bull Case

- Merger synergies begin in 2026, retrofit orders surge from IMO regulation, and backlog rises sharply.

- CB and lock-up share overhang are absorbed naturally as enterprise value improves.

Bear Case

- IMO regulation delays persist, raising fixed-cost pressure from engineering personnel.

- The 24th CB and merger-share lock-up release cap the share price.

- Working-capital shortages raise the risk of another equity financing.

This stock offers high beta to the green-shipping theme, but the margin of safety is still unproven. I would prioritize OCF turnaround, engineering backlog growth, CB conversion volume, and lock-up timing over headline revenue.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224172213971

- 팬스타테크솔루션 흡수합병 추진: https://www.panstar.co.kr/media/press/?type=view&idx=313

- 팬스타엔터프라이즈-팬스타테크솔루션 합병계약 승인: https://www.panstar.co.kr/media/press/?type=view&return_url=%2Fmedia%2Fpress&idx=323

- 데이터투자, 2024년 연간 영업이익: https://www.datatooza.com/article/2025020516343895593f2b9cee90_80

- KRX 회사합병 결정 공시: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250227000857&rcpno=20250227006028&orgid=F&tran=Y&langTpCd=0

- 녹색경제신문, IMO 탄소세 논의 연기: https://www.greened.kr/news/articleView.html?idxno=332254

- 데이터투자, 2025년 연간 영업손실: https://www.datatooza.com/article/20260204172602140752ef3739c4_80

- 부산노컷, 비상장 계열사 흡수합병: https://mbs.nocutnews.co.kr/news/6300793

- FnGuide 팬스타엔터프라이즈 재무제표: https://comp.fnguide.com/SVO2/ASP/SVD_Finance.asp?pGB=1&gicode=A054300&cID=&MenuYn=Y&ReportGB=D&NewMenuID=103&stkGb=701

- Daum, CB 전환가액 666원 조정: https://v.daum.net/v/3zwGJGTsEO?f=p

- 합병등 종료보고서: https://kind.krx.co.kr/external/2025/05/15/001986/20250515004660/12000.htm

- 핀포인트뉴스, 친환경 선박 EPC 성장 모멘텀: https://www.pinpointnews.co.kr/news/articleView.html?idxno=383894

- LoTIS, IMO 중기조치 채택 1년 연기: https://lotis.or.kr/news/5977