DEEP RESEARCH · KOSTECSYS

Kostecsys: A Growth Turnaround Built on AI Data Centers and xEV Power Modules

A review of the shift from RF packages to high-heat-dissipation power-semiconductor materials and components

0. Bottom line first

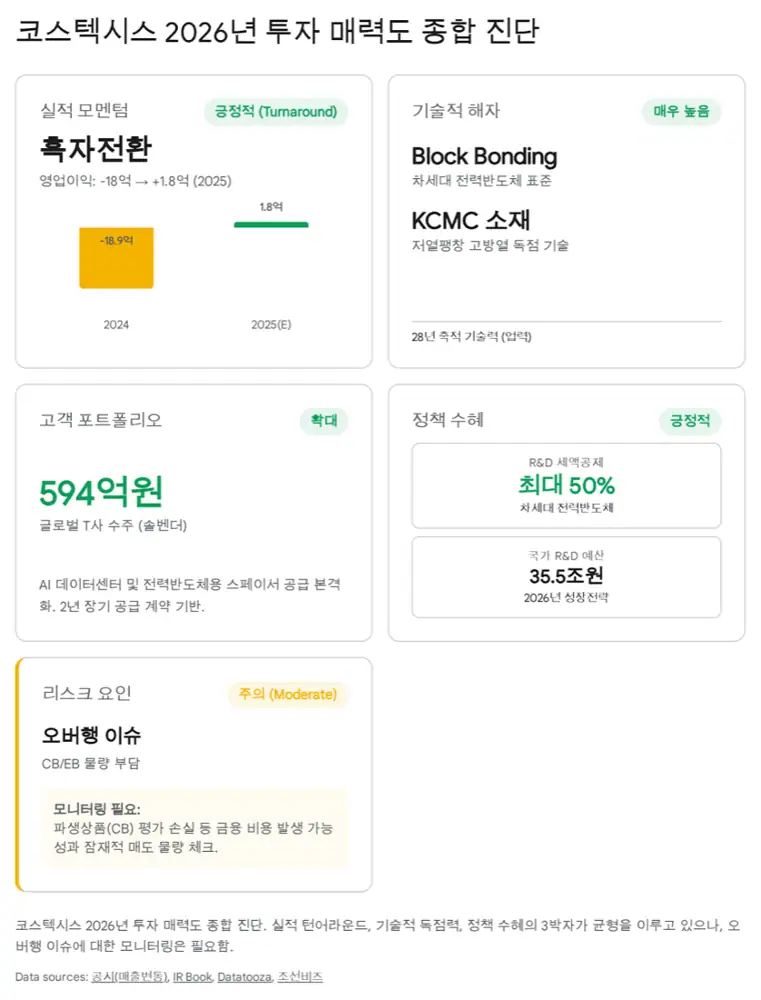

My core read is that Kostecsys' return to profit is not merely cost cutting. It reflects a product-mix shift as high-heat-dissipation spacers and block bonding enter mass production. If the KRW 59.4 billion long-term supply contract with Company T began contributing in 4Q25, 2026 becomes the year to verify a structural turnaround.

KRW 15.2B revenue

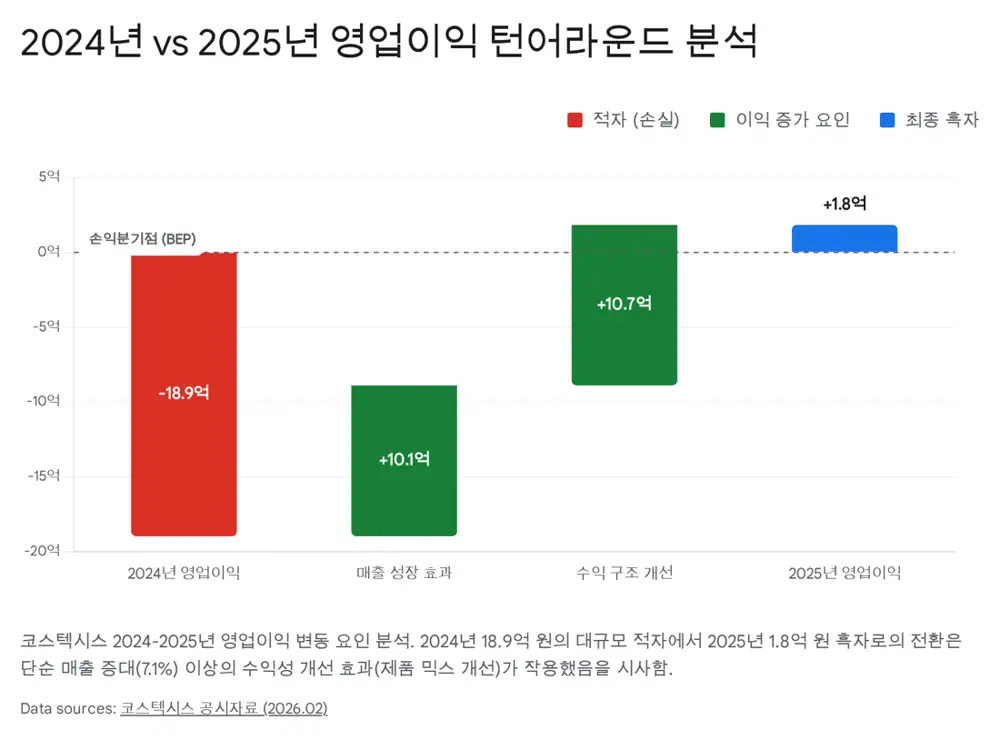

Revenue grew 7.1% from KRW 14.2B in 2024, and operating profit turned from a KRW 1.89B loss to a KRW 180M profit.

KRW 59.4B from T

The long-term contract signed on July 16, 2025 is interpreted as entering shipment phase from 4Q25.

2026-2028

The source scenario is 2026 revenue above KRW 50B, 2027 customer diversification, and 2028 mix improvement from laser-diode and GaN packages.

Official fact: The source summarizes the 2025 preliminary results disclosed on February 4, 2026 as revenue of KRW 15.2 billion, operating profit of KRW 180 million, and net income of roughly KRW 1.2 billion. In 2024, the company recorded revenue of KRW 14.2 billion, operating loss of KRW 1.89 billion, and net loss of KRW 1.79 billion.

Interpretation: Annual revenue growth alone is not dramatic. What matters is that the company moved from KRW 9.5 billion of cumulative revenue and a KRW 1.05 billion operating loss through 3Q25 to a full-year profit. By simple arithmetic, 4Q alone generated more than KRW 5.7 billion of revenue and more than KRW 1.2 billion of operating profit, making new power-semiconductor component revenue recognition the key item to check.

1. The nature of the earnings turn

| Item | 2024 | 2025 | Meaning |

|---|---|---|---|

| Revenue | KRW 14.2B | KRW 15.2B | 7.1% YoY growth |

| Operating profit | -KRW 1.89B | KRW 180M | Operating-level turnaround |

| Net income | -KRW 1.79B | About KRW 1.2B-1.23B | Likely includes FX gains and CB/EB derivative valuation gains |

| 3Q25 cumulative | - | KRW 9.5B revenue, KRW 1.05B operating loss | Baseline showing the 4Q concentration |

2025 looks like the inflection year when Kostecsys began changing from an RF communication-parts company into a core materials and components supplier for next-generation power semiconductors. The source's main judgment is that R&D investment, sustained despite delayed 5G network spending, began converting into earnings growth from 4Q25.

Interpretation: Net income running far above operating profit should not be read as pure operating strength. Export exposure, a high KRW/USD exchange rate, and potential valuation gains on convertible and exchangeable bonds should be considered. Still, the fact that operating profit turned positive first is a meaningful positive.

2. Product mix: from RF to thermal power-semiconductor parts

The historical revenue portfolio was centered on RF packages tied to 5G network investment cycles. The trigger for the 2025 turnaround is the rise of thermal components for AI data centers and electric-vehicle power semiconductors.

- Mass production for AI data-center power modules: The KRW 59.4 billion long-term contract with Company T, signed on July 16, 2025, entered full shipment phase from 4Q25 according to the source. These components are used in AI-server PSUs and EV traction inverters, with higher technical entry barriers and better expected margins than legacy telecom products.

- Third plant ramp: The block-bonding center, the company's third plant in Incheon's Namdong Industrial Complex, was completed in November 2025 and began operating in December. Producing a large 4Q profit despite early depreciation suggests secured backlog was enough to absorb fixed costs.

- Non-operating income: Net income of KRW 1.23 billion versus operating profit of KRW 180 million should be read alongside export exposure, FX tailwinds, and potential derivative valuation gains related to CBs and EBs.

3. Company T and customer diversification

Official fact: Based on the KRW 59.4 billion supply contract disclosed in July 2025 and related press reports, the source interprets Company T as likely a top-tier U.S. power-semiconductor IDM or a leading EV company. The contract is described as running from July 2025 to December 2027 through quarterly confirmed purchase orders.

Interpretation: Because Company T is not disclosed by name, its identity should not be treated as confirmed fact. But if the source is right that Kostecsys passed strict mass-production validation for high-efficiency AI data-center power modules and EV SiC inverter modules, then the company's spacer and packaging technologies have cleared part of a global reliability bar.

Reliability test

Thermal management determines performance and lifetime in data centers and EVs, so supplier qualification is demanding.

Through Dec. 2027

A quarterly confirmed PO structure would provide higher visibility than an MOU.

NXP, MACOM, Dynax

Existing RF semiconductor customers and potential Hyundai-related collaboration are diversification points.

4. End markets: AI data centers, xEVs, and RF

Kostecsys draws attention because AI data centers and electric vehicles both chase high power and high efficiency, which inevitably makes heat dissipation a critical bottleneck.

| End market | Problem | Kostecsys role |

|---|---|---|

| AI data centers | GPU racks and PSUs are becoming denser, pushing air cooling toward its limits. The source expects the global data-center market to grow more than 15% annually through 2026 on AI inference demand and notes that roughly 40% of power consumption is used for cooling. | Low-CTE, high-thermal-conductivity spacers reduce thermal shock between chip and substrate. Block bonding lowers resistance versus wire bonding and expands the heat-dissipation area. |

| Next-generation mobility | As EVs move from 400V to 800V systems, SiC power-semiconductor adoption rises, and CTE mismatch becomes a reliability issue. | The source says KCMC offers a CTE close to SiC while providing copper-like thermal conductivity. As power modules move toward double-sided cooling, spacer demand can rise from one per module to dozens. |

| 5G/6G and defense | 5G Advanced, early 6G commercialization, aerospace, and defense radar can increase heat-control needs for high-power GaN devices. | Legacy RF package capability can extend into high-power GaN communication and defense packages. |

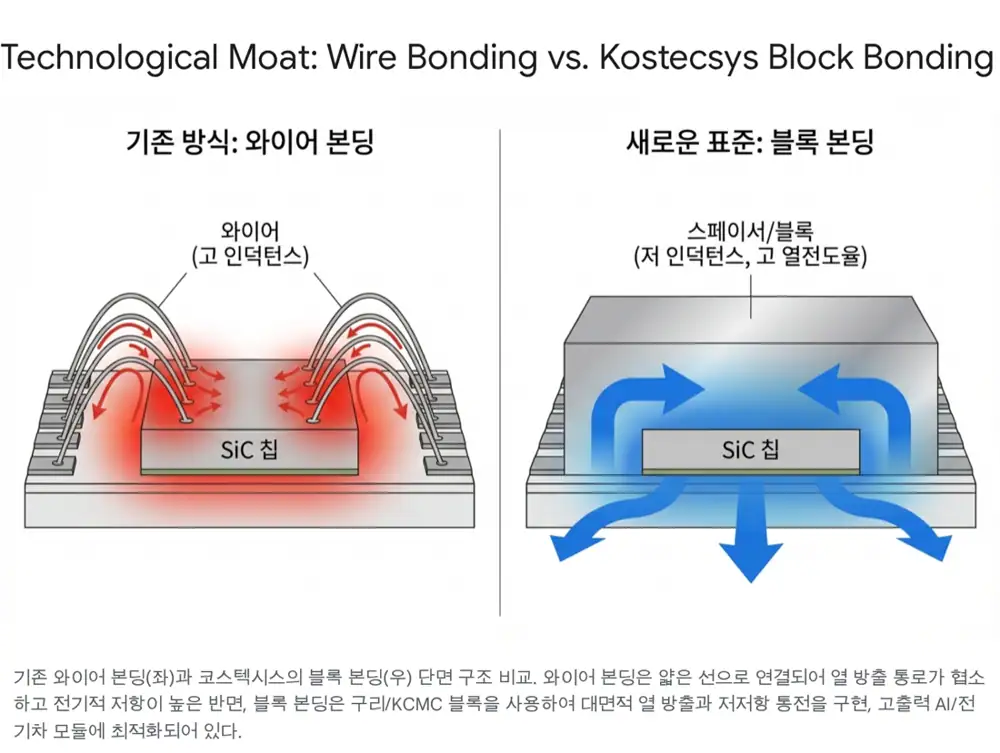

5. Technology moat: from materials to packaging

The reason Kostecsys is described as more than a component processor is vertical integration and block bonding. The source says that while most competitors import expensive materials from Japan or Germany and mainly process them, Kostecsys internalizes KCMC blending, molding, sintering, precision machining, plating, and brazing.

- Cost competitiveness: Lower dependence on external materials can protect margins against price pressure from global customers.

- Customization: Adjusting material ratios to meet customer-required CTE and thermal conductivity can shorten development cycles and deepen technical ties.

- Block bonding: Replacing wire bonding with metal-block direct connections can reduce parasitic inductance, electrical resistance, and thermal bottlenecks.

6. 2026-2028 roadmap and policy support

The Korean government is strengthening semiconductor support from 2026. The Semiconductor Special Act passed by the National Assembly on January 29, 2026 and the Materials, Parts, and Equipment 2.0 strategy create a favorable environment for technology-independent suppliers. The source says designation of next-generation power semiconductors as national strategic technology can lift R&D tax credits for SMEs and mid-sized firms up to 50%, while a special account may open infrastructure and equipment subsidy possibilities.

For 2026, the source cites full-year reflection of Company T volume, 100% utilization of the third plant, and possible government projects tied to the KRW 35.5 trillion 2026 R&D budget. For 2027, it expects supply to customers under qualification, including European S and domestic H, and capacity expansion to around KRW 100 billion. For 2028, as the AI data-center market matures, the source expects higher revenue contribution from laser-diode packages and telecom GaN packages.

7. Risks and my view

- Overhang: KRW 6.3 billion of exchangeable bonds issued in July 2025 could become share supply if the stock price rises.

- End-market volatility: A prolonged EV demand slowdown could lead to adjustments in Company T's automotive orders, though AI data-center demand may provide an offset.

- Customer concentration: The KRW 59.4 billion long-term contract is a major catalyst, but because the customer is undisclosed, order pace and revenue timing must be checked quarter by quarter.

- Policy over-expectation: The Semiconductor Special Act and materials policy are supportive, but they do not automatically guarantee company-level earnings.

My conclusion is broadly aggressive like the source, but the practical way to underwrite the thesis is to separately check the official 4Q25 result, 1H26 Company T shipment expansion, third-plant utilization, new-customer qualification outcomes, and EB overhang management.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224172211089

- Data Tooza: KRW 59.4B power-semiconductor spacer order: https://www.datatooza.com/article/20251223100223306952ef3ec9dc_80

- Metro Seoul: Share move after KRW 59.4B order: https://www.metroseoul.co.kr/article/20250716500179

- Yonhap: Semiconductor Special Act passed: https://www.yna.co.kr/view/AKR20260129165451003

- Korea Policy Briefing: Semiconductor competitiveness support act: https://www.korea.kr/briefing/pressReleaseView.do?newsId=156742072

- Korea Financial News: First high-heat-dissipation spacer mass-production order: https://www.fntimes.com/html/view.php?ud=2023072218031918569249a1ae63_18

- TechWorld: 2026 semiconductor 2nm era: https://www.epnc.co.kr/news/articleView.html?idxno=328115

- Yonhap: CES 2026 power and cooling competition: https://www.yna.co.kr/view/AKR20260108020000003

- TechWorld: AI and SiC market outlook: https://www.epnc.co.kr/news/articleView.html?idxno=327727

- iNews24: Next-generation power semiconductors market share outlook: https://www.inews24.com/view/1918853

- Pointe: 2026 materials/parts/equipment cooperation model: https://www.pointe.co.kr/news/articleView.html?idxno=70455

- ETNews: Materials/parts/equipment strategy revision: https://www.etnews.com/20260201000095

- Chosun Biz: R&D tax credit for next-generation power semiconductors: https://biz.chosun.com/policy/policy_sub/2026/01/09/OZV6VCV7LFG4JLYZ2ICVTDDCVQ/

- NBN Media: KOSDAQ CB/BW overhang risk: https://www.nbntv.kr/news/articleView.html?idxno=338878