DEEP RESEARCH · MEATBOX GLOBAL

Meatbox Global: Digitalizing Meat Distribution and the 2026 Tariff Catalyst

Reviewing 2025 preliminary results, finance/processing expansion, and zero-tariff U.S. beef

0. Bottom line first

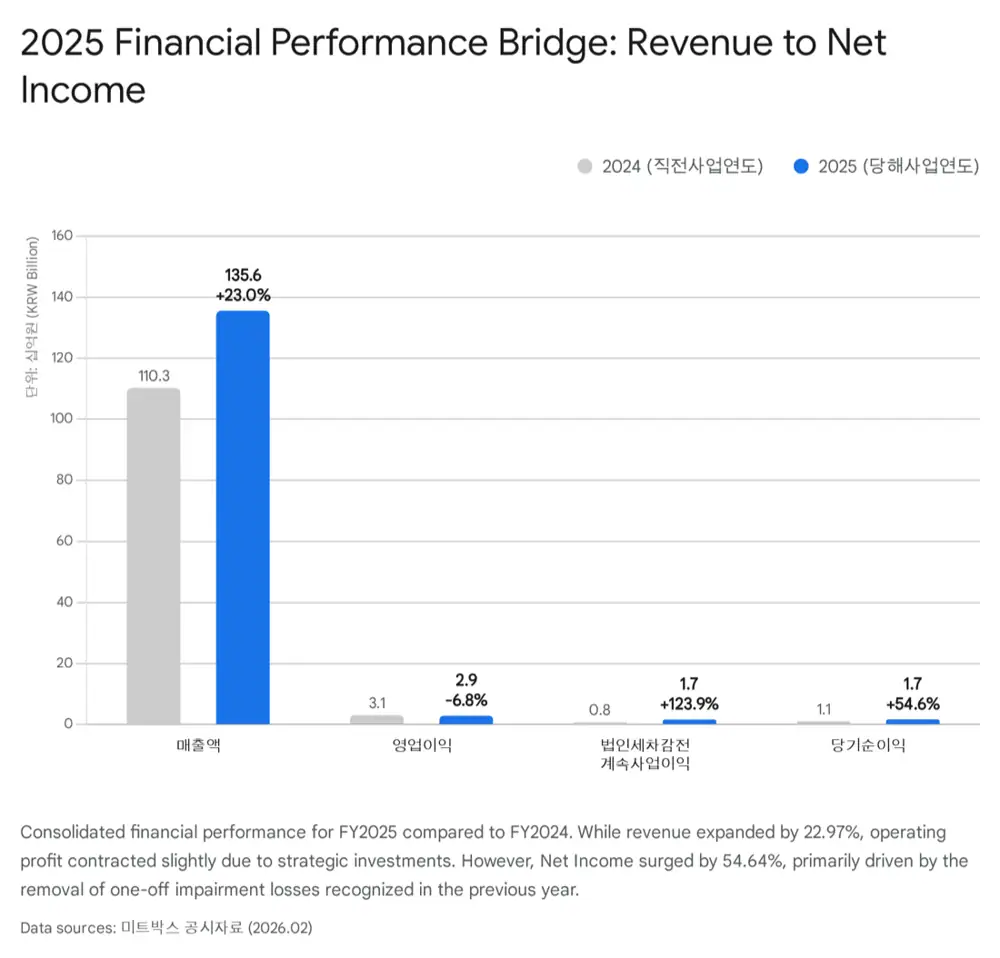

Meatbox Global is evolving from a B2B meat brokerage platform into distribution infrastructure combining data, logistics, finance, and processing. In 2025, revenue grew 22.97%, operating profit fell 6.83% due to new-business costs, and net profit rose 54.64% as the prior year’s one-off impairment disappeared.

Official fact: The source reports 2025 consolidated revenue of KRW 135.59397 billion, operating profit of KRW 2.90604 billion, and net profit of KRW 1.73639 billion. Revenue rose 22.97%, operating profit fell 6.83%, and net profit rose 54.64% year on year.

Interpretation: The operating-profit decline looks more like infrastructure investment than core deterioration: MeatMatch Finance, Meatgram, development/data hiring, and listing costs. The key question is whether this spending turns into GMV and margin in 2026.

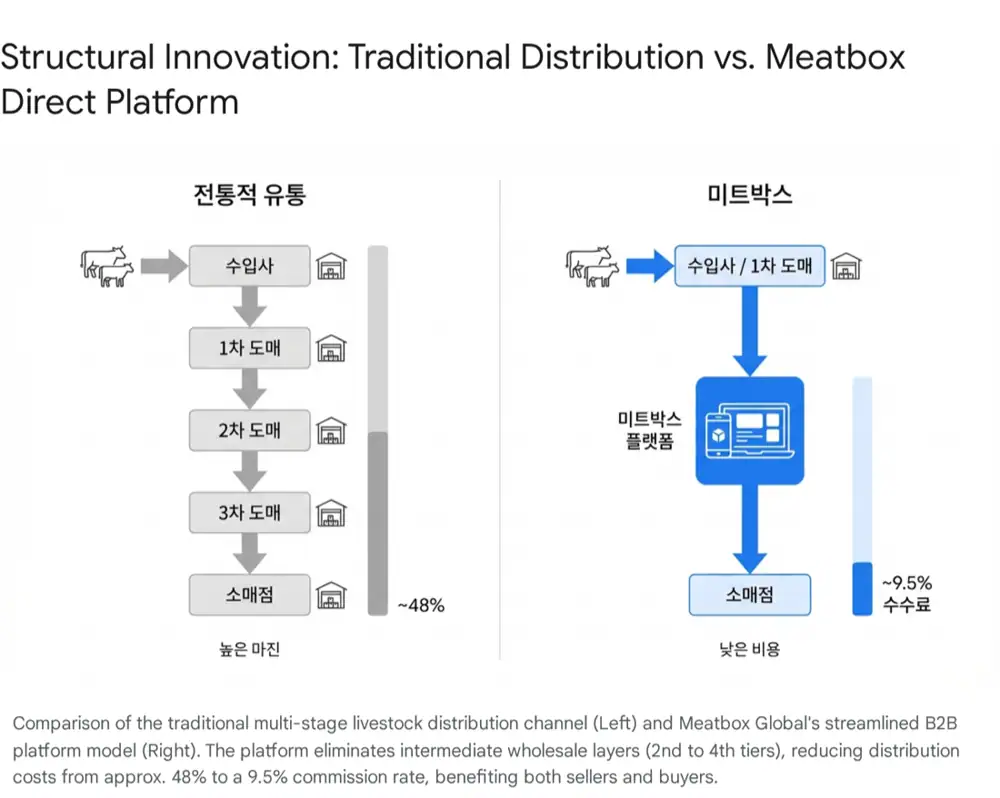

1. Business Model: A B2B Platform Reducing Information Gaps

Traditional meat distribution often runs through four or more intermediaries between producers/importers and restaurants/butchers. The source says distribution costs that averaged 48.0% can be reduced to about a 9.5% platform usage or brokerage fee. Sellers get broader channels and faster settlement; buyers get price transparency and lower costs.

Meatbox’s strength is more than 11 years of transaction data and pricing data across over 80,000 SKUs. Since meat prices change daily, price discovery itself becomes a lock-in function.

2. 2025 Results: Revenue Growth and Investment Costs

| Item | 2025 | YoY | Interpretation |

|---|---|---|---|

| Revenue | KRW 135.59397bn | +22.97% | GMV growth, direct-purchase/PB strength, Meatgram contribution |

| Operating profit | KRW 2.90604bn | -6.83% | Finance/processing subsidiaries, hiring, and listing costs |

| Pre-tax continuing income | KRW 1.68710bn | +123.94% | Prior-year one-off non-operating cost disappeared |

| Net profit | KRW 1.73639bn | +54.64% | Core profit flowed back into net income |

In 2024, an impairment loss of about KRW 2.3 billion on construction-in-progress assets at a subsidiary hurt net income. In 2025, that large non-recurring loss was absent. Revenue growth and net-profit recovery are positive, but operating-margin improvement remains the 2026 test.

3. New Growth Engines: Finance and Processing

MeatMatch Finance is data-based supply-chain finance. It uses real-time price data to value frozen-meat collateral and lends against inventory stored in the My Box logistics center. This supplies working capital to sellers, activates platform trading, and creates interest income plus seller lock-in.

Meatgram is a meat-processing company with HACCP-certified facilities. The April 2025 acquisition expands Meatbox from raw-meat brokerage into cutting, portioning, and packaging. Growth in single-person households and higher restaurant labor costs support demand for ready-to-cook cut and portioned products.

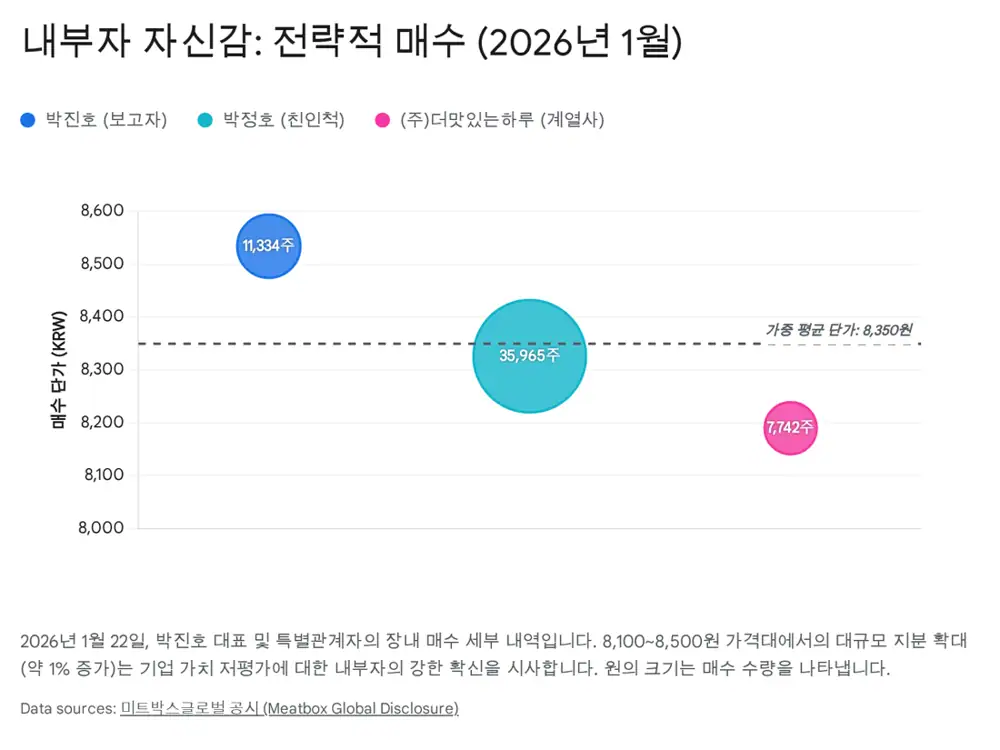

4. 2026 Catalysts: U.S. Beef Tariff Removal and Insider Buying

Official fact: The source says U.S. beef import tariffs fell from about 5.3% to 0% on January 1, 2026. It also says director Park Jin-ho and related parties bought 55,041 shares in the market, raising ownership from 5.02% to 6.00% according to the January 22, 2026 disclosure.

The source lists purchase prices of KRW 8,534 for Park Jin-ho, KRW 8,326 for auditor Park Jung-ho, and KRW 8,190 for affiliate The Delicious Day. It reads this as management viewing the KRW 8,200-8,500 share-price area as undervalued.

5.3% → 0%

Lower U.S. beef import costs can increase trading volume from B2B buyers.

Cargill and others

Direct partnerships with global suppliers can speed up pass-through of lower costs.

55,041 shares

Market purchases by related parties are presented as a signal of confidence in 2026 earnings.

5. Risks and Watchpoints

- U.S. supply chain: Drought and lower cattle herd numbers in the U.S. may raise beef prices and offset part of the tariff benefit.

- Finance execution risk: MeatMatch Finance carries credit risk, so collateral valuation, disposal capability, and risk systems need monitoring.

- Overhang: Post-IPO lockup releases by VCs and other financial investors could increase short-term share-price volatility.

The metrics I would watch are U.S. beef transaction volume in 1H 2026, profit contribution from MeatMatch and Meatgram, and how institutional overhang is absorbed.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170636015

- Google Drive: Meatbox company analysis request

- Meat Insight: Why U.S. beef prices rise despite 0% tariff

- Financial Post: Meatbox highlighted as U.S. beef tariff-removal beneficiary