DEEP RESEARCH · Ubiquoss Holdings

Ubiquoss Holdings: Where value-up meets the Hyper-AI network

A review of 2025 preliminary results, the 2026-2028 shareholder-return policy, and potential K-Network 2030 benefits.

0. Bottom line first

Ubiquoss Holdings sits at the intersection of two major Korean equity themes in early 2026: corporate value-up and Hyper-AI network infrastructure. 2025 operating profit growth of 113.3% and the 2026-2028 shareholder-return policy can support a case for narrowing the holding-company discount.

Profit level-up

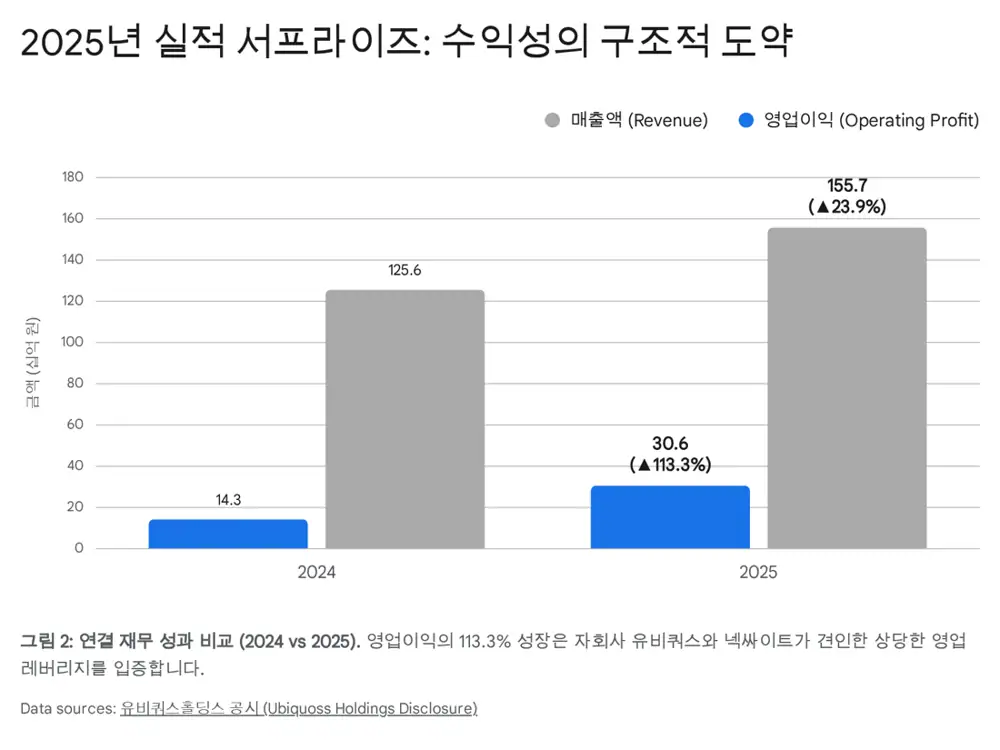

2025 consolidated revenue was KRW 155.6623 billion and operating profit was KRW 30.60543 billion, up 23.9% and 113.3%, respectively.

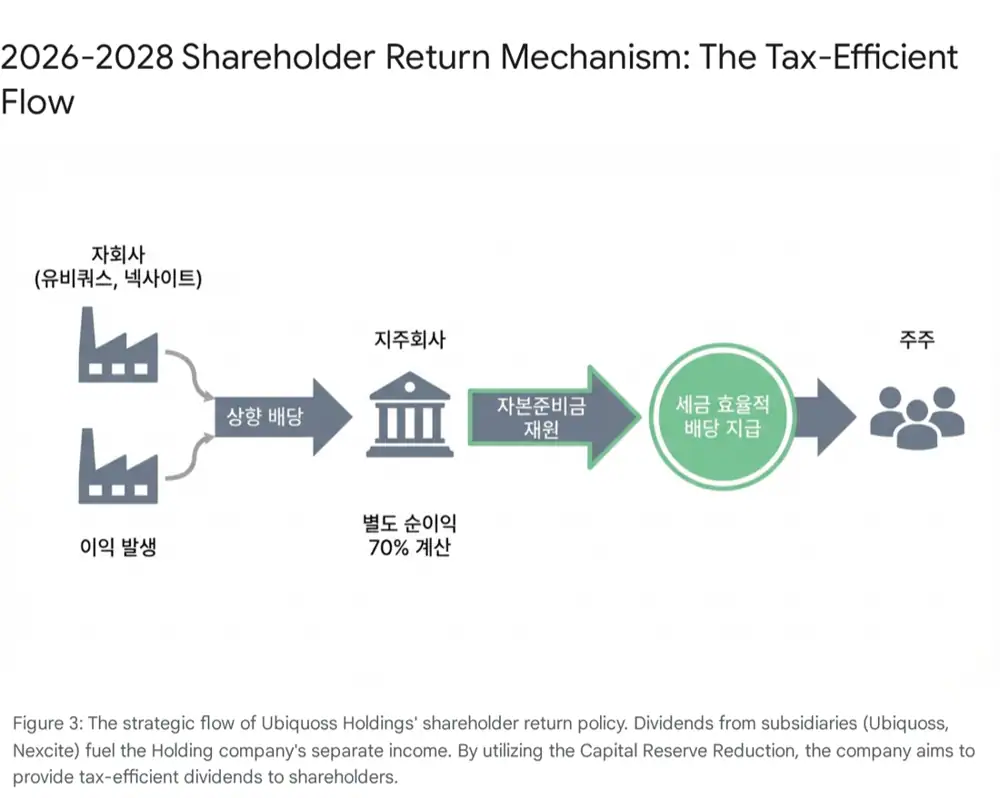

70% of separate net income

The company presented a dividend policy equal to 70% of adjusted separate-basis net income for fiscal years 2026-2028.

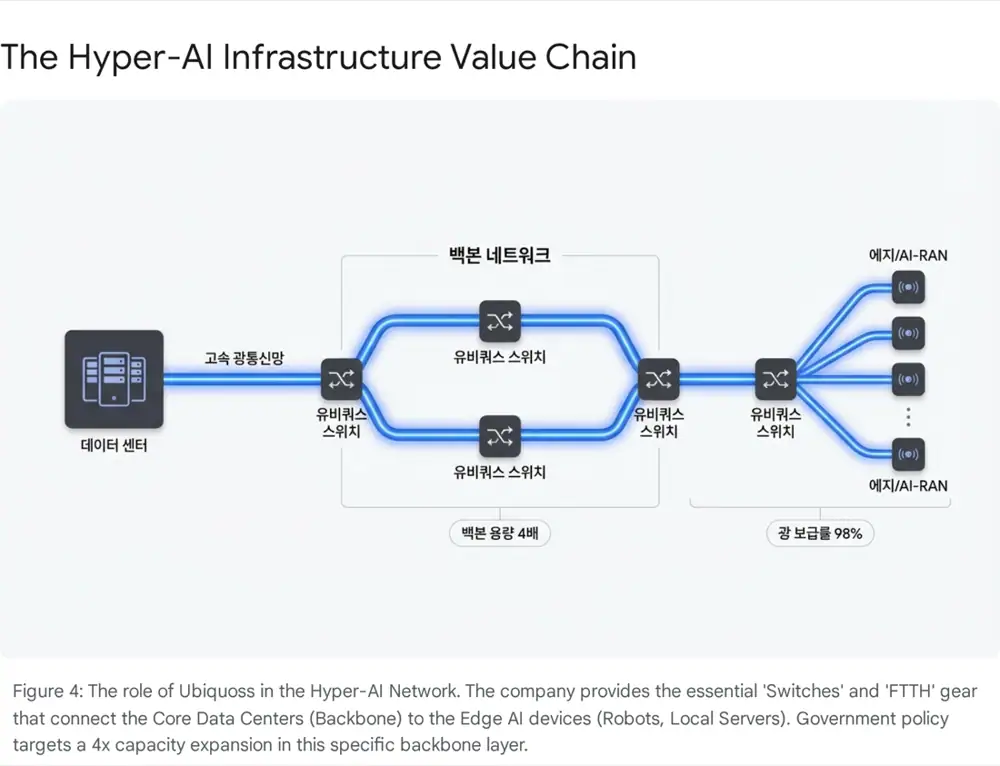

AI network

Backbone capacity of more than four times, 98% optical-fiber coverage, 6G, and AI-RAN strategies can stimulate wired-equipment demand.

Official fact: On February 3, 2026, the company disclosed 2025 preliminary results and a 2026-2028 medium-term shareholder-return policy. The original post reads these as evidence of a structural re-rating phase.

Interpretation: I read Ubiquoss Holdings as more than a simple telecom-equipment holding company: it is an indirect AI-infrastructure beneficiary with a net-cash-like balance sheet and a defined dividend policy.

1. Corporate Structure and Governance: A practical control tower

Ubiquoss Holdings became a pure holding-company structure in March 2017 through a spin-off and split-off that separated the operating company Ubiquoss. In April 2021, it was removed from legal holding-company regulation because it did not meet the KRW 500 billion asset threshold under the amended Fair Trade Act, but in practice it still serves as the group's strategic control tower.

Official fact: As of the end of 2025, CEO Lee Sang-geun owned about 50.10% of the company.

Interpretation: When a holding company's cash flow is a major source of liquidity for the controlling shareholder, the interests of the controlling and minority shareholders can align around high dividends. That helps reduce agency costs, one cause of the Korea discount.

| Pillar | Core asset | Original-post view |

|---|---|---|

| Network | Ubiquoss, KOSDAQ-listed | Core cash generator and growth engine |

| Industrial computing | Nexsite, 99% owned | Hidden alpha from AIoT and smart-factory expansion |

| Medical devices/biotech | Bylab | Long-term growth option |

| Finance/investment | Ubiquoss Investment and others | Antenna for new growth engines |

Nexsite's 99% ownership is especially important. Unlike listed Ubiquoss, where the ownership ratio is about 33-39%, Nexsite's growth can be reflected almost fully in consolidated earnings and separate-basis dividend resources. Ubiquoss, Nexsite, and Bylab also share a hardware-manufacturing base, which can support R&D and manufacturing efficiency.

2. 2025 Preliminary Results: Operating leverage confirmed

The 26th fiscal-year 2025 preliminary results disclosed on February 3, 2026 suggest a step-up in earnings power, because operating profit grew far faster than revenue.

| 2025 consolidated result | Amount | YoY |

|---|---|---|

| Revenue | KRW 155.6623 billion | +23.9% |

| Operating profit | KRW 30.60543 billion | +113.3% |

| Pre-tax continuing operating income | KRW 41.96378 billion | +94.0% |

| Net income | KRW 33.64539 billion | +57.1% |

Official fact: The company identified revenue increases at subsidiaries Ubiquoss and Nexsite as the main reason for the earnings change.

Interpretation: Operating-profit growth of 113.3% versus revenue growth of 23.9% shows operating leverage in a fixed-cost-heavy equipment-manufacturing business.

- Ubiquoss turnaround: After weak results caused by delayed telecom capex in 2024, performance recovered in 2025, helped by a higher share of high-margin FTTH products such as 10-gigabit internet equipment.

- Hidden Nexsite contribution: Demand for industrial computing boards raised Nexsite utilization, and because Nexsite is 99% owned, its earnings growth directly affects holding-company shareholder value.

Official fact: As of the end of 2025, total assets were KRW 417.1 billion, total liabilities were KRW 33.2 billion, and the debt-to-equity ratio was about 8.7%.

Interpretation: A near debt-free balance sheet reduces financing-cost risk in a high-rate environment and provides capacity for future M&A or shareholder returns.

3. 2026-2028 Shareholder Returns: The core value-up mechanism

On February 3, 2026, Ubiquoss Holdings disclosed a medium-term shareholder-return policy for fiscal years 2026-2028. The original post views this not simply as higher dividends but as a strategy considering capital efficiency and tax effects.

70% of adjusted separate net income

The basis is close to cash flow actually entering the holding company.

Steady dividends

Dividend-capable subsidiaries are expected to pay dividends every year, formalizing the flow from subsidiaries to the holding company and final shareholders.

All treasury shares

The company said it would cancel all treasury shares it already holds evenly over 2026 and 2027.

3.1 Dividend of 70% of separate net income

The company set the dividend resource at 70% of adjusted separate-basis net income. Separate net income is largely composed of subsidiary dividends, brand fees, rent, and other items close to cash flowing into the holding company.

Adjusting non-recurring gains and valuation gains on financial products, which do not bring cash in, can improve dividend predictability and stability. This reduces the risk that dividends swing sharply because of market prices or temporary accounting items.

3.2 Capital-reserve reduction and after-tax yield

Official fact: Ubiquoss Holdings resolved a capital-reserve reduction at an extraordinary shareholders' meeting on December 3, 2025. Under Korean commercial law, a company can reduce capital reserves exceeding 1.5 times capital stock, transfer them into retained earnings, and use them as dividend resources.

Interpretation: Under current Korean tax rules, dividends funded by capital-reserve reduction are often excluded from dividend-income taxation. Compared with the 15.4% withholding on ordinary cash dividends, the after-tax yield can appear more attractive than the headline pre-tax dividend yield.

3.3 Treasury-share cancellation

The company announced that it would cancel all treasury shares it already holds evenly over two years from 2026 through 2027. Treasury-share cancellation directly reduces the public share count and raises EPS and ROE.

Interpretation: The original post reads the cancellation, at a time when PBR is around a historical low of 0.7x, as a signal that the company sees the stock as undervalued.

4. Subsidiary Value and NAV: A case for discount narrowing

A holding company's value eventually converges toward the sum of its subsidiary values, or SOTP and NAV. Ubiquoss Holdings' core assets are Ubiquoss, Nexsite, and Bylab.

| Asset | Core detail | Value point |

|---|---|---|

| Ubiquoss (264450) | Switches, FTTH, domestic network equipment | 10G/100G switch demand from the Hyper-AI network strategy |

| Nexsite | Industrial computing boards and systems, 99% owned | Potential direct beneficiary of Physical AI and smart factories |

| Bylab | Medical-device development and manufacturing | Long-term healthcare-device option from aging demographics |

Because Nexsite is unlisted, its market value is not directly visible. The original post argues that, given its contribution to the sharp rise in 2025 consolidated operating profit, applying comparable-company PERs could make Nexsite's stake value a margin of safety explaining a meaningful portion of Ubiquoss Holdings' market capitalization.

Official fact: Nexsite established the Global Embedded Investment Association during 2025, expanding its business scope.

Interpretation: Korean holding companies commonly trade at 40-60% discounts to NAV because of double-counting concerns. Ubiquoss Holdings has room for a narrower discount because of its 70% payout policy, unlisted Nexsite value, and net-cash structure.

5. Macro Setting: Hyper AI and K-Network 2030

The investment case connects beyond company-specific issues to Korean infrastructure policy. In December 2025, the Ministry of Science and ICT announced the Hyper-AI Network strategy, centered on 6G commercialization by 2030, AI-RAN adoption, and expansion of wired backbone networks.

- Return of wired networks: The government said it would expand backbone capacity by more than four times by 2030 and raise optical-fiber coverage to 98%, potentially driving demand for high-capacity switches and FTTH equipment.

- 2026 as the first investment year: The source cites KRW 290 billion for network technology development and demonstrations in 2026, up KRW 45 billion year on year.

- Physical AI: Robots, autonomous driving, and smart factories require real-time processing and ultra-low-latency communication. The logic is that existing 1G-class networks are insufficient and 10G-or-higher equipment replacement is needed.

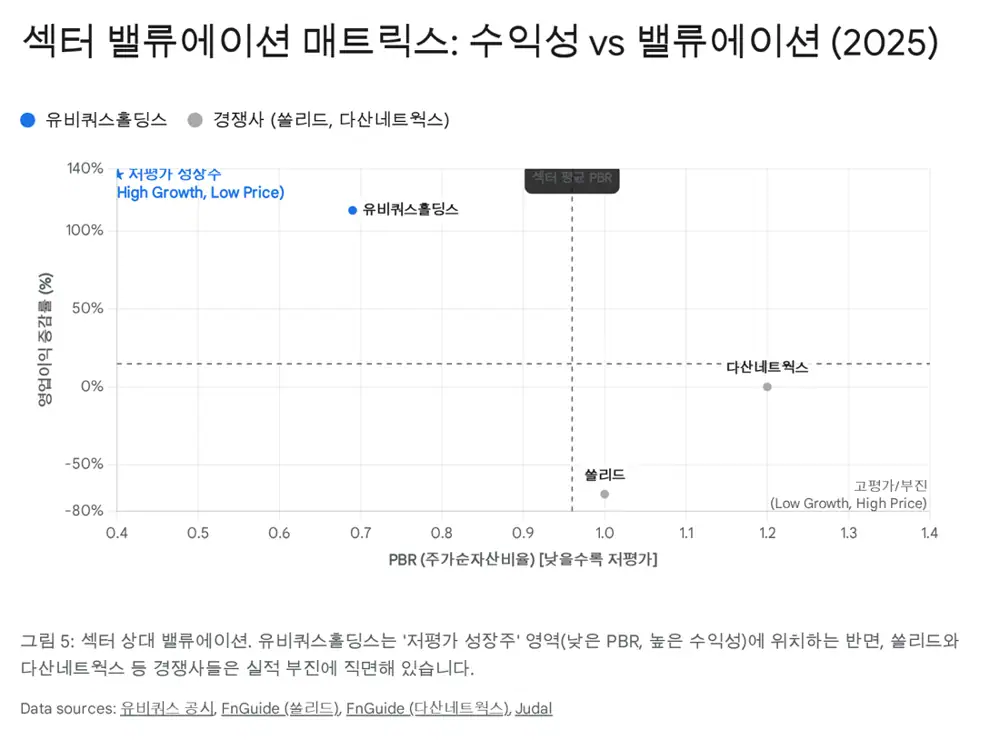

6. Peer Comparison and Investment Strategy

Compared with telecom-equipment peers, the original post argues that Ubiquoss Holdings stands out in financial stability and shareholder returns.

| Company | Original-post comparison point | Read-through |

|---|---|---|

| Dasan Networks | Accumulated deficits in recent years made dividends difficult, while building sales and other measures were used to improve the balance sheet | Financial risk from subsidiary guarantees and earnings volatility |

| Solid | 3Q 2025 cumulative operating profit fell 68.9% year on year | Impacted by delayed telecom investments |

| Ubiquoss Holdings | 2025 operating profit rose 113%, balance sheet is close to debt-free, PBR below 0.7x | Combination of profitability and shareholder returns |

6.1 Top Pick logic

- Policy-benefit clarity: The Hyper-AI Network strategy requires wired-network upgrades, which can lead to Ubiquoss equipment orders.

- Credibility of shareholder returns: A 70% payout ratio, treasury-share cancellation, and tax-efficient dividend strategy offer a structure beneficial to both controlling and minority shareholders.

- Earnings momentum: The original post judges that the 113% profit growth confirmed in 2025 may continue into 2026-2027 alongside Nexsite's structural growth.

- Valuation appeal: With PBR below 0.7x, net cash, and subsidiary stake value, the stock is framed as having downside rigidity and upside potential.

6.2 Time-horizon checkpoints

- Short term, 1-3 months: Whether dividend expectations and the earnings surprise are reflected around final 2025 results and the March shareholder-meeting season.

- Medium term, 6-12 months: Execution of the government network-investment budget, visibility of AI data-center equipment orders, and possible multiple expansion.

- Long term, 1-3 years: Execution of the 2026-2028 shareholder-return policy, resolution of chronic undervaluation, and possible recovery toward PBR 1x.

Interpretation: The original post presents Ubiquoss Holdings as a Top Pick in telecom equipment and holding-company sectors. I frame that not as an investment recommendation, but as a research view to track whether earnings leverage, shareholder returns, and policy benefits are confirmed together.

In conclusion, Ubiquoss Holdings is difficult to view as only a stagnant telecom-equipment holding company. It has exposure to the wired-infrastructure equipment ecosystem needed for the AI era and a more advanced shareholder-return policy. 2026 can be the first year in which this change is verified in numbers.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170468763

- Etoday CInsight: https://cinsight.etoday.co.kr/detail/00411385

- TradingView: https://kr.tradingview.com/news/hankyung:21209fc1165a7:0/

- 38 Communication: https://www.38.co.kr/html/news/?o=v&m=kosdaq&key=special&no=1891367&page=1

- DigitalToday: https://www.digitaltoday.co.kr/news/articleView.html?idxno=561238

- Korea Securities Daily: https://www.ksdaily.co.kr/news/articleView.html?idxno=104328

- Judal 2026.01.30: https://www.judal.co.kr/?view=stockAI&shareToken=leCnIaKb9Mg60Yks

- News1: https://www.news1.kr/it-science/general-it/6012067

- MoneyToday: https://www.mt.co.kr/tech/2025/12/18/2025121717525432933

- Dailysecu: https://www.dailysecu.com/news/articleView.html?idxno=203534

- KRX Dasan Networks annual report: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240321001479&docno=&viewerhost=&

- Judal 2025.11.27: https://www.judal.co.kr/?view=stockAI&shareToken=aE6CHKrUO77236OC