DEEP RESEARCH · YOUNG HWA TECH/HYDROGEN COMMERCIAL VEHICLE POWER CONTROL

Young Hwa Tech: Hydrogen-Vehicle High-Voltage Conversion and Control Order

How PCDU/HFDC technology and a KRW 198.6 billion Hyundai contract could drive structural re-rating

0. Bottom line first

Young Hwa Tech's February 2026 Hyundai Motor order is not just another parts contract. It is a long-term supply agreement worth about KRW 198.6 billion, equal to 209.4% of 2024 consolidated revenue, and I see it as the moment the company is redefined from a junction-box supplier into a hydrogen commercial-vehicle power conversion and control systems supplier.

The key products are PCDU and HFDC. Fuel-cell vehicles use both a fuel-cell stack and a high-voltage battery, making the power path far more complex than in conventional vehicles. Young Hwa Tech has combined 20 years of vehicle power-control experience with 10 years of high-voltage component R&D to secure core power electronics for Hyundai's next-generation hydrogen commercial vehicle platform.

1. Company overview and technical moat

Official fact: Young Hwa Tech was founded in August 2000 and built its position in automotive electronics, especially junction boxes. The source argues that, as of 2026, the company should be viewed not as an internal-combustion power-distribution supplier but as a Tier-1 supplier of high-voltage power conversion and control systems for EVs and FCEVs.

A junction box is a node in the vehicle electronics nervous system, relaying thousands of wires and signals. Young Hwa Tech won GM Supplier of the Year and a Platinum quality rating in this area, and that reliability became a reference for entering the higher-difficulty eco-friendly vehicle power-electronics market.

| Item | Source figure/detail | Interpretation |

|---|---|---|

| Employees | 179 | Small-to-mid automotive parts company scale |

| R&D staff | 68 people, about 38% | Engineering-centered organization rather than pure manufacturing |

| Compared with typical suppliers | Contrasts with 10% to 20% R&D staffing levels | Evidence of a rising technology barrier |

2. PCDU and HFDC: the core of the contract

Official fact: The core products in the Hyundai Motor supply agreement are PCDU, or Power Control Distribution Unit, and HFDC, or High-Voltage DC-DC Converter. The source describes them as among the most technically difficult components in fuel-cell vehicle drive systems.

Voltage stabilization

A fuel-cell stack's output voltage fluctuates with load. The HFDC boosts it to the stable high voltage required by the motor inverter, for example around 800V.

Millisecond control

It must monitor hydrogen/oxygen reaction speed, required vehicle output, and battery SOC in real time to control conversion efficiency.

Efficiency, thermal, EMC

The source says Young Hwa Tech's HFDC achieves over 95% efficiency and integrates high-voltage switching thermal design and electromagnetic shielding.

The PCDU is the traffic tower of internal FCEV power flow. During acceleration it sends power from both stack and battery to the motor; at steady speed it drives the motor with stack power and charges the battery with surplus power; during deceleration it recovers regenerative braking energy into the battery.

Interpretation: Payload and packaging efficiency directly affect truck and bus economics. Young Hwa Tech's ability to integrate high-voltage connectors, relays, fuses, and sensors into a single package can lower customer total cost of ownership.

3. Technology accumulation timeline

- 2000-2009: Built the base in circuit design and packaging through localization of junction boxes and development of PCB-type junction boxes.

- 2010-2015: Internalized global quality systems through GM global program awards and Supplier of the Year recognition; established a U.S. entity to deepen North American market understanding.

- 2015-2020: Started full-scale high-voltage parts R&D after being selected to lead a national project for integrated EV power-electronics modules. It won GM global EV platform parts, CCC IEC, in 2019 and became a Hyundai electrification Tier-1 supplier in 2020.

- 2021-present: Expanded production capability for hydrogen and electric commercial vehicles through Hyundai hydrogen electric truck high-voltage parts development and mass production, plus a Mexico plant.

4. End market: commercial hydrogen vehicles open first

Passenger FCEVs have been held back by charging infrastructure and competition from BEVs, but commercial vehicles are different. Large battery-electric trucks can require several tons of batteries and lose payload efficiency, while hydrogen vehicles can improve uptime through higher energy density and 15-to-20-minute refueling.

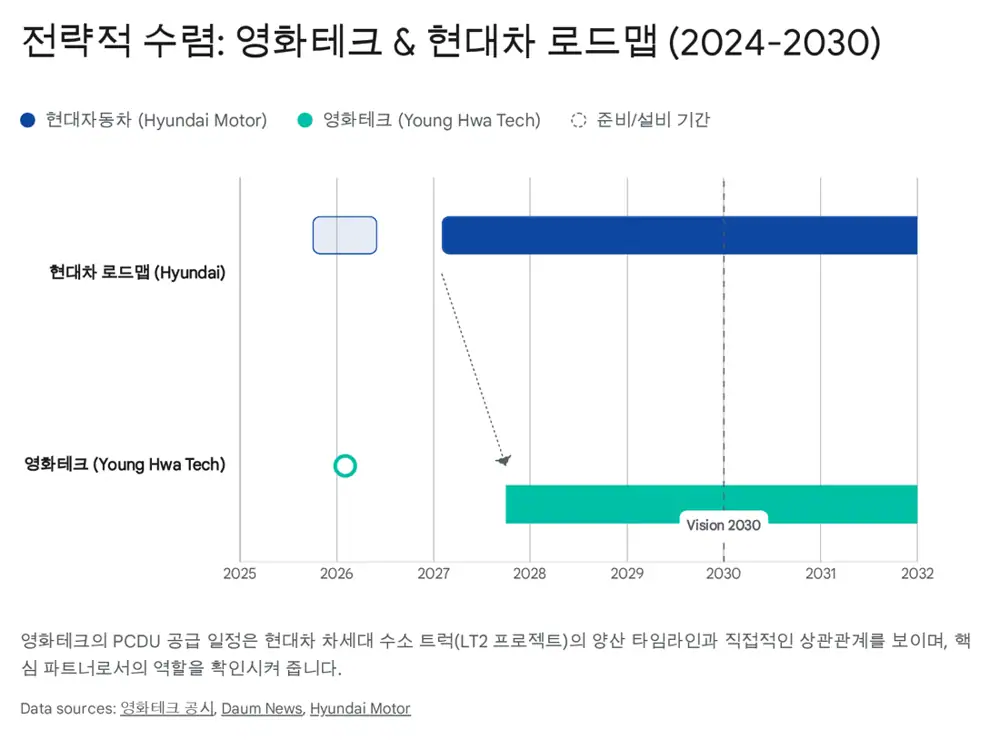

Official fact: Hyundai Motor has mass-produced the XCIENT hydrogen heavy truck and exported it to markets such as Switzerland and the U.S. The source says the real expansion should begin with the next-generation model, project name LT2. Hyundai's Jeonju plant is described as converting existing truck lines into eco-friendly vehicle lines from the second half of 2026 through the first half of 2027.

The supply start date of October 2027 matches Hyundai's next-generation hydrogen truck production timing. I read that as a sign that Young Hwa Tech is involved deeply in the initial platform design, not merely supplying a later add-on component.

- Korea: The government provides purchase subsidies of up to KRW 300 million per hydrogen bus and is pursuing replacement of aging city and intercity buses with hydrogen vehicles by 2030.

- United States: The IRA provides up to USD 40,000 in tax credits for commercial clean vehicles and subsidizes clean hydrogen production to reduce fuel prices. Hyundai's Georgia plant, HMGMA, and logistics projects such as NorCAL ZERO can create demand.

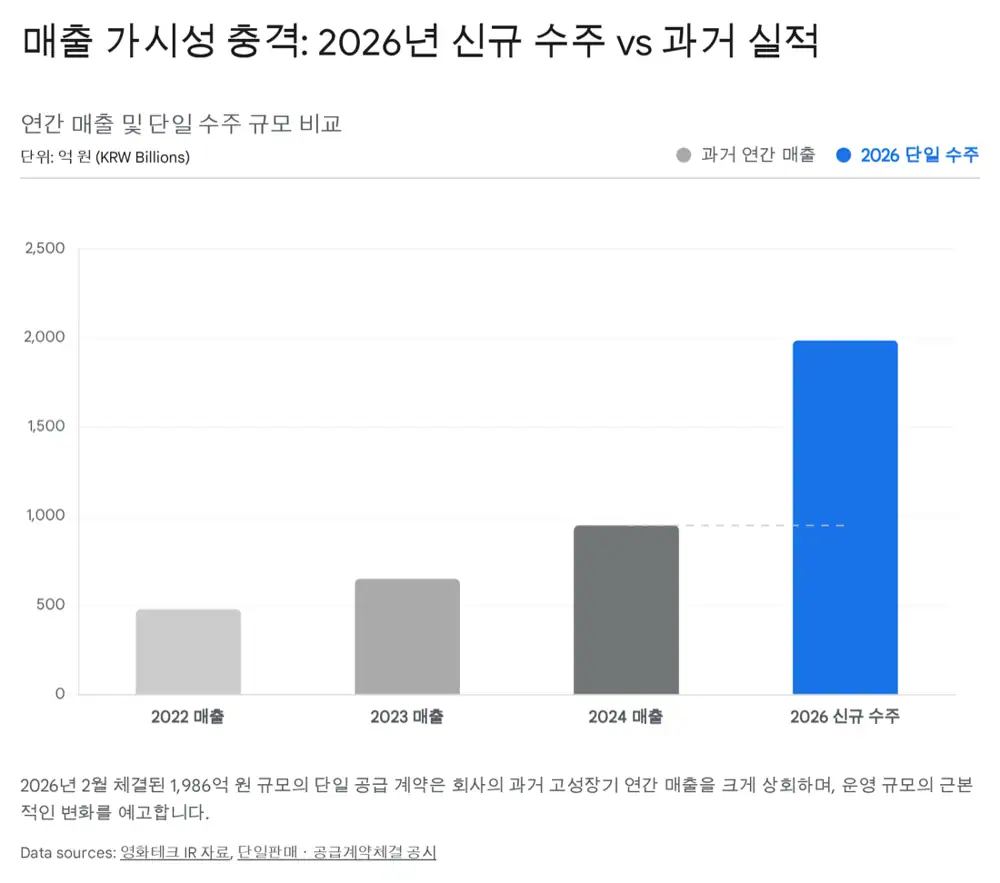

5. Revenue meaning of the KRW 198.6 billion contract

| Item | Detail |

|---|---|

| Contract value | KRW 198,563,967,056, about KRW 198.6bn |

| Counterparty | Hyundai Motor Company |

| As percentage of 2024 revenue | 209.4%, based on KRW 94.8bn consolidated revenue in 2024 |

| Contract period | February 2, 2026 to December 31, 2033 |

| Supply start | October 2027, first planned mass-production supply |

| Annual average effect | About KRW 33.0bn, roughly 35% of 2024 revenue |

Interpretation: Revenue contribution in 2026 and the first half of 2027 may be limited. Meaningful recognition is likely to begin in 2028 and continue through 2033 as stable cash flow.

Operating leverage matters. Young Hwa Tech has already made proactive CAPEX, including Asan plant expansion, the Giheung research center, and Mexico plant construction. If more than KRW 30.0 billion in annual incremental revenue is added from 2028 with fixed costs already reflected, a meaningful portion after variable costs could flow into operating profit. The source says operating margin, about 7.7% in 2023 and 16.2% in 2024, could settle at mid-teens or above after 2028 as volumes rise.

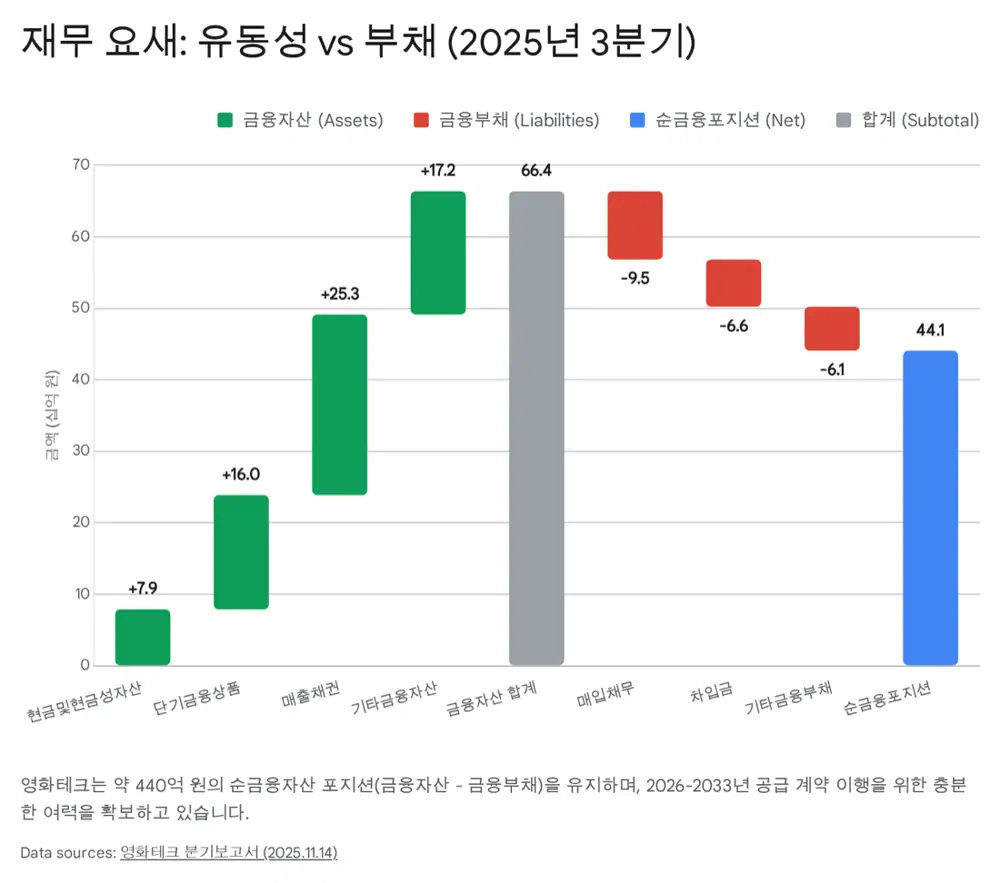

6. Balance sheet and capital allocation

| Category | End-3Q25 source figure | Meaning |

|---|---|---|

| Cash and equivalents | KRW 7.9bn | Short-term liquidity |

| Short-term financial products | KRW 16.0bn | Cash-like defense |

| Total liquidity | About KRW 23.9bn | Self-funding capacity |

| Total financial liabilities | KRW 22.3bn | Amortized-cost basis |

| Interest-bearing debt | KRW 4.5bn short-term borrowings and KRW 2.1bn long-term borrowings, about KRW 6.6bn total | Net-cash structure because cash-like assets exceed borrowings |

| Convertible bonds/derivatives | KRW 9.3bn convertible bond and KRW 1.9bn derivative liability at end-2024 disappeared by end-3Q25 | Overhang concern reduced |

Net cash is a competitive advantage in a high-rate environment. When peers cut investment because of interest expense, Young Hwa Tech can continue R&D and equipment investment with internal funds. The source also cites KRW 25.2 billion in receivables and KRW 8.2 billion in inventory; rising inventory can be a leading indicator of raw-material preparation ahead of mass production in the second half of 2027.

The company also owns 5.86% of autonomous-driving solution company SpringCloud, but its book value is carried at zero, reflecting conservative accounting. If the autonomous-driving market opens, this can act like a hidden call option.

7. Shareholders and re-rating logic

Official fact: CEO Eom Jun-hyung is the controlling shareholder with 44.12%, or 4,716,860 shares. Including related parties such as spouse Ahn Mi-kyung and children Eom Yoon-jin and Eom Hyun-jung, insider ownership exceeds 50%. Korea Terminal Industry is the second-largest shareholder with 9.26%, or 990,000 shares.

Interpretation: High insider ownership aligns management's long-term growth incentives with shareholders. Korea Terminal Industry's strategic stake is also a signal that Young Hwa Tech's technology is recognized by the automotive connector and module industry.

The source says Young Hwa Tech had been valued like a traditional internal-combustion parts maker at 5x to 8x P/E, but the KRW 198.6 billion hydrogen commercial-vehicle parts order creates a basis for re-rating as an eco-friendly energy mobility solutions company. It also compares with power electronics and secondary-battery equipment/parts peers that often receive 15x to 25x P/E multiples.

Technical moat

High-voltage hydrogen-vehicle parts have high entry barriers and require mass-production references.

Quality of earnings

The mix can improve toward higher-margin products that include technology value, not simple processing.

Visibility to 2033

Confirmed backlog provides long-term revenue stability.

Market opening speed

The pace of hydrogen-vehicle adoption, refueling infrastructure, hydrogen prices, and Hyundai dependence must be monitored.

8. Final take

Young Hwa Tech has validated a decade of hydrogen power-conversion investment through a long-term Hyundai order. My key checkpoints are October 2027 mass-production readiness, annual revenue recognition of about KRW 30.0 billion from 2028 onward, additional GM and global OEM orders through the Mexico plant, and the pace of hydrogen commercial-vehicle infrastructure buildout.

With a strong balance sheet, high R&D ratio, and confirmed backlog, Young Hwa Tech can be re-rated from a simple automotive parts stock into a hydrogen economy infrastructure company. However, delays in hydrogen-vehicle adoption or rising single-customer dependence would pressure both supply schedules and valuation.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170467664