DEEP RESEARCH · Jinheung Enterprise (002780.KS)

Jinheung — KRW 158B HVDC plant win + a ‘big bath’ teeing up an asymmetric setup

Portfolio pivot from B2C housing into B2B group industrial capex, and the paradox of a 0.37× P/B

0. Bottom line first

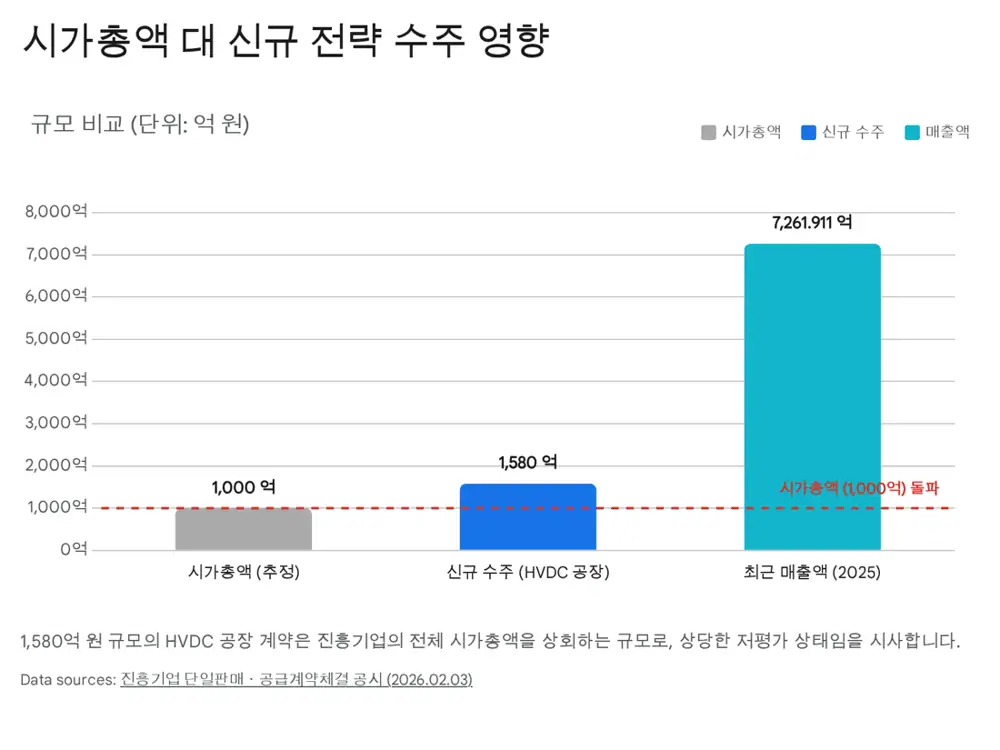

The Jan-26 disclosure of a KRW 158B HVDC plant construction contract with Hyosung Heavy equals 21.73% of prior-year revenue and is ~1.5× the whole market cap (KRW 101B). The simultaneous large 2026 loss (-KRW 23B operating, -KRW 28.3B net) is best read not as deterioration but as a ‘big bath’ ahead of meaningful group-capex revenue starting in 2027. Today’s P/B of 0.37× reflects ‘failing housing builder’ framing — re-categorised as ‘Hyosung group industrial-capex EPC’, even a return to 0.6–0.8× implies 60–80% upside.

1. Two realities — housing slump vs power-grid supercycle

Korea’s construction sector is split. One side: housing crushed by high rates and PF risk. Other side: industrial plant in a supercycle — AI data centers, renewables interconnect, ageing-grid replacement. Jinheung sits at the intersection.

2. The business — moat analysis

2.1 Mix (3Q25 revenue)

- Housing (Harrington Place): 61.2% — historic cash-cow, exposed to PF / unsold inventory.

- Civil engineering (SOC): 20.1% — government-backed, defensive.

- Plant / industrial: the strategic growth engine — building Hyosung group facilities.

2.2 Captive moat — Hyosung’s trickle-down

The captive relationship gives Jinheung ① credit enhancement via implicit parent support, and ② captive order flow when Hyosung Heavy expands capacity. The KRW 158B win is the first concrete demonstration.

3. The trigger event — global grid supercycle

3.1 Three drivers

- AI / data centers: Generative AI explodes hyperscale data-center buildout → demand for stable HV power.

- Renewables interconnect: Offshore wind etc. is far from cities — long-distance transmission requires HVDC.

- Ageing grids: NA/EU grids built 50–60 years ago hitting full replacement cycles.

3.2 Hyosung Heavy’s standing

Top-tier alongside Siemens, Hitachi Energy and GE. Large US/EU bookings put Hyosung into a capacity-short position. HVDC transformers/breakers are hard to manufacture, creating a global bottleneck.

3.3 The contract — specifics

| Item | Detail |

|---|---|

| Issuer | Hyosung Heavy Industries Co., Ltd. |

| Project | Ultra-high-voltage transformer (HVDC) plant construction |

| Location | 303 Gongdan-ro, Seongsan-gu, Changwon, Gyeongnam |

| Period | 2026-02-11 to 2027-06-30 (~16 months) |

| Value | KRW 158B (21.73% of prior-year revenue) |

The contract formalises Jinheung as Hyosung Heavy’s designated partner for capex execution — strong follow-on probability for the US Memphis expansion and other future plants.

4. The ‘big bath’ — anatomy of the 2026 loss

4.1 Numbers

- Revenue: KRW 576.3B (YoY -20.6%) — regional housing slump, delayed groundbreakings, weak presales.

- Operating: -KRW 23B (prior -KRW 4.7B → wider loss).

- Net: -KRW 28.3B (prior +KRW 2.1B → loss).

4.2 Why it reads as a big bath

The company labelled the loss “one-off site provisions reflecting the regional real-estate slump.” Classic playbook: front-load the ugly entries in the year before the new growth cycle (HVDC) hits — a clean book for 2027’s turnaround. Booking ‘bad news’ early stops legacy housing exposure from haunting 2027 results when HVDC revenue rolls in.

4.3 Balance-sheet check

| Item | Value |

|---|---|

| Total assets | KRW 563.1B |

| Total equity | KRW 268.2B |

| Total liabilities | KRW 275.3B |

| Debt ratio | ~110% |

Industry average is 200–300% — Jinheung’s balance sheet is strong enough to weather housing winter while pivoting to industrial EPC.

5. Impact — Q · P · C

5.1 Q (volume / revenue)

- ~KRW 9.8B/month → if 11 months of 2026 are worked, ~KRW 100B of new revenue is recognised, offsetting ~17% of the housing-segment decline.

- Group industrial capex share rises sharply → revenue volatility falls.

5.2 P (price / margin)

- Housing margin: raw-material inflation can’t fully pass into sale prices; unsold units add finance costs.

- Group capex projects: stable margins (OPM 3–5%), zero unsold-inventory risk, certain payment → high-quality operating income drops through to the bottom line.

5.3 C (cost)

- Large HVDC revenue absorbs fixed costs (overhead absorption) → company-wide OPM improves.

6. Valuation — P/B re-rating

- Equity: KRW 268.2B.

- Market cap: ~KRW 100.7B.

- P/B: ~0.37×.

The market values Jinheung as a ‘failing housing builder’ at 0.3×. Re-categorised as ‘Hyosung industrial EPC’, fair P/B should be 0.6–0.8×; power-infrastructure specialists trade 1.5×+. 0.37 → 0.6× alone delivers 60–80% upside.

6.2 Catalysts to close the gap

- Retail sells on the loss disclosure; institutions analyse the Hyosung capex cycle and accumulate.

- ‘Big bath’ release is usually the price bottom — bad news exposed, book cleaned up.

6.3 Risks

- Further losses: If the housing slump exceeds expectations, additional charges may follow.

- Raw-material spike: Steel inflation could compress margin (mitigated by likely escalation clauses in group contracts).

- Group risk: Hyosung Heavy financial deterioration could delay payment — currently mitigated by record-high industry conditions.

7. Conclusion — deep-value turnaround

KRW 158B HVDC win

Formalises designated-partner role in group capex.

2026 big bath

Sets up a clean 2027 turnaround.

P/B 0.37 → 0.6×

Reframing alone implies 60–80% upside.

Investment view: BUY — turnaround play. Buy the shock, sell the turnaround. Stop = Hyosung Heavy materially cancels or delays its capex plan.

8. Appendix — shareholders and ecosystem

- Top holder: Hyosung Heavy (48.19%) — not just equity but strategic alliance.

- Major holder: Woori Bank (~14.12%) — legacy creditor from past workout debt-for-equity. A potential M&A trigger if Hyosung buys it back or a third party acquires the block.

- Group ecosystem: Hyosung Heavy (HVDC + hydrogen filling stations), Hyosung TNC / Advanced Materials (spandex / carbon-fiber expansion), Hyosung Chemical (Vietnam etc.) — global expansion creates co-investment opportunities for Jinheung.

Sources

- Naver blog source: m.blog.naver.com/.../224170383695

- Jinheung Enterprise (002780) — DART disclosure (HVDC contract): dart.fss.or.kr

- Hyosung Heavy Industries — parent IR: hyosungheavyindustries.com

- HVDC overview (Wikipedia): en.wikipedia.org