DEEP RESEARCH · AJINEXTEK

Ajinextek: Structural Turnaround and a Physical AI Motion-Control Platform

Analyzing ASIC-based motion control, Samsung robot cooperation, and the 2026 semiconductor-equipment cycle

0. Bottom line first

Ajinextek’s 2025 turnaround looks structural, not just cyclical: production-base consolidation, SCM improvement, and higher-margin Physical AI controllers all contributed. The key is whether its rare domestic motion-control ASIC design capability becomes more valuable in semiconductor equipment and robot automation.

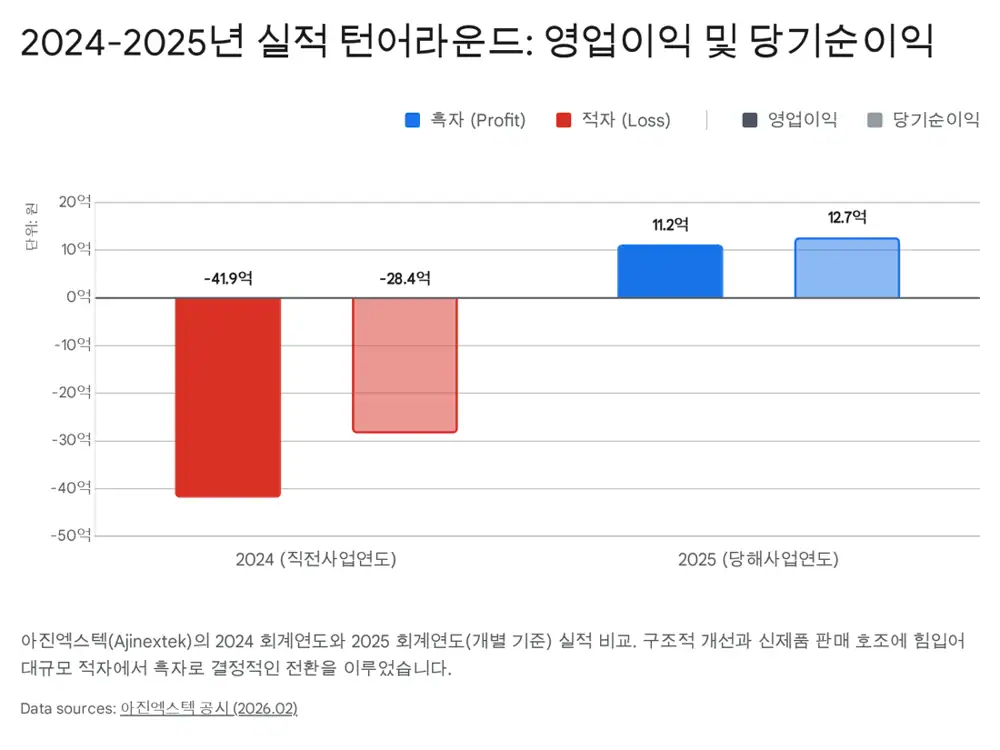

Official fact: The source says Ajinextek was founded on December 29, 1997 and has the ability to design and manufacture dedicated motor-control chips in-house. 2025 revenue was KRW 25.72 billion and operating profit was KRW 1.123 billion, turning profitable.

Interpretation: Revenue growth was only 2.2%, but operating profit improved by more than KRW 5.3 billion. This is a case where cost structure and product mix changed earnings more than sales growth did.

1. Identity: From Controller Localization to Physical AI

Ajinextek is a fabless component/materials company that grew around localization of controllers in Korea’s automation market, which had relied heavily on imported technology. Unlike firms that import general-purpose chips and assemble modules, it implements control algorithms at the silicon-chip level to secure real-time performance regardless of operating-system load.

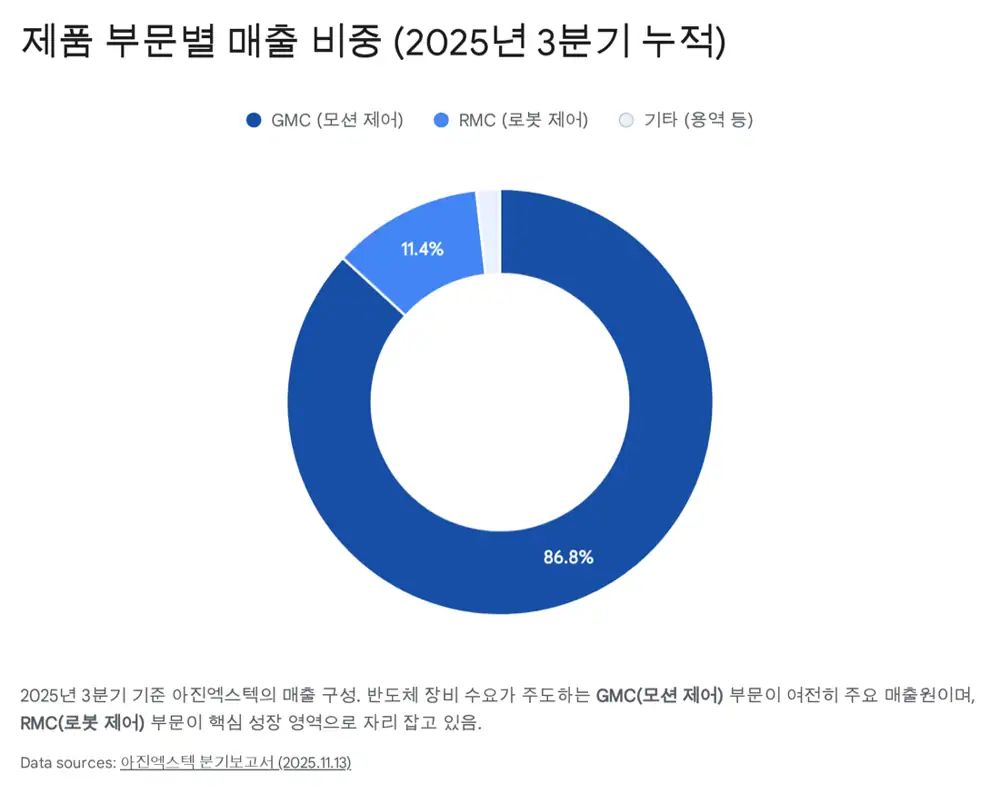

The business is split into General Motion Control and Robot Motion Control. The source says GMC accounted for about 86.8% of cumulative 3Q 2025 revenue and acts as the cash cow, while RMC accounted for about 11.4% but is the fastest-growing future driver.

2. 2025 Results: Small Sales Growth, Large Profit Improvement

| Item | 2025 | 2024 | Change |

|---|---|---|---|

| Revenue | KRW 25,720m | KRW 25,168m | +KRW 552m, +2.2% |

| Operating profit | KRW 1,123m | -KRW 4,189m | +KRW 5,312m, turnaround |

| Pre-tax continuing income | KRW 1,274m | -KRW 3,036m | +KRW 4,310m, turnaround |

| Net income | KRW 1,274m | -KRW 2,842m | +KRW 4,116m, turnaround |

The source cites Gumi production-site consolidation, SCM advancement, more realistic inventory valuation, and contribution from high-margin new products as the turnaround drivers. Comparing 3Q cumulative revenue of about KRW 16.7 billion and operating loss of about KRW 760 million with full-year revenue of KRW 25.7 billion and operating profit of KRW 1.12 billion implies Q4 alone delivered roughly KRW 9.0 billion of revenue and KRW 1.9 billion of operating profit.

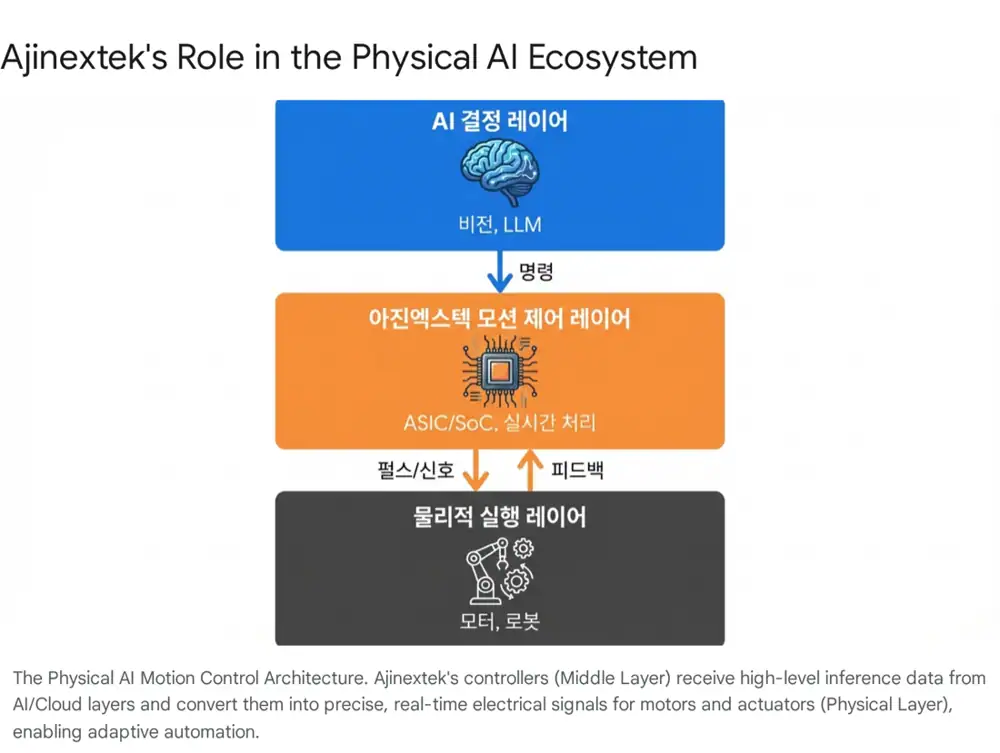

3. Physical AI Controllers and New Products

Physical AI turns AI decisions into movement in the physical world. A robot arm picking an object or an autonomous robot avoiding obstacles needs low-latency, precise motor control. Ajinextek’s controller plays the central-nervous-system role in that process.

2U · 4U · W1

The source says they can control up to 8 axes at a 125-microsecond cycle and synchronize up to 128 axes within 1 millisecond.

Standalone controller

Supports up to 32 axes, 16 by default, with 500-microsecond precision control and standalone operation without a PC.

PCIe slots

Can mount AI accelerators or vision cards, supporting smart factories and robot-cell control.

4. Samsung Partnership and Robot Expansion

The source says Ajinextek began supplying robot electrical boxes to Samsung Electronics in January 2021 and started supplying SCARA robot sets in Q2 2024. This means recognition not only as a controller supplier but also as a supplier of complete systems including body and drive components.

Official fact: The source explicitly says Ajinextek has not officially disclosed mass-production controller supply for Bot Fit, formerly GEMS-Hip.

Interpretation: Given its Samsung robot-controller history and compact, low-power motion-chip technology, it can be discussed as a possible wearable-robot supply-chain candidate, but that should remain a possibility rather than a confirmed fact.

5. 2026 Market Environment and Risks

Citing SEMI, the source says the global semiconductor equipment market is expected to reach a record $139 billion in 2026 and $156 billion in 2027 on AI semiconductor demand such as HBM and GPUs. If orders increase at Korean equipment makers such as SEMES and Wonik IPS, demand for Ajinextek motion controllers could expand.

- Policy support: Provisional anti-dumping duties on Chinese and Japanese industrial robots and robot-localization policy are favorable for domestic controller makers.

- End-market dependence: More than half of revenue depends on semiconductor and smartphone equipment, so delays in Samsung or SK hynix capex can increase volatility.

- Input costs: Higher wafer and electronic-component prices can pressure costs, although the 2025 SCM improvements raise resilience.

The main investment points are structural turnaround, rare domestic motion-control chip design capability, expanded Samsung SCARA robot supply, Physical AI products, and 2026 semiconductor equipment investment growth.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170375339

- Robot News: Ajinextek begins supplying SCARA robot sets to Samsung

- Robot News: Ajinextek achieves 2025 turnaround

- HelloT: Four new motion-controller products announced

- Industry News: Begins industrial-robot supply to Samsung

- Robot News: Industrial robot supply to Samsung expands from Q1

- Asia Economy: Feature stock on Samsung robot-parts supply

- SEMI: Equipment sales projected to reach $156bn in 2027

- SEMI: Equipment sales forecast to reach $139bn in 2026

- SEMI Korea: 2026-2028 global 300mm fab equipment investment outlook

- AJU PRESS: Korean robotics sector battles Chinese and Japanese competition