DEEP RESEARCH · SGC E&C/CONSTRUCTION & CHEMICAL PLANTS

SGC E&C Company Analysis and 2026 Outlook

A review of post-2025 big-bath cleanup, overseas chemical plant orders, and valuation re-rating potential

0. Bottom line first

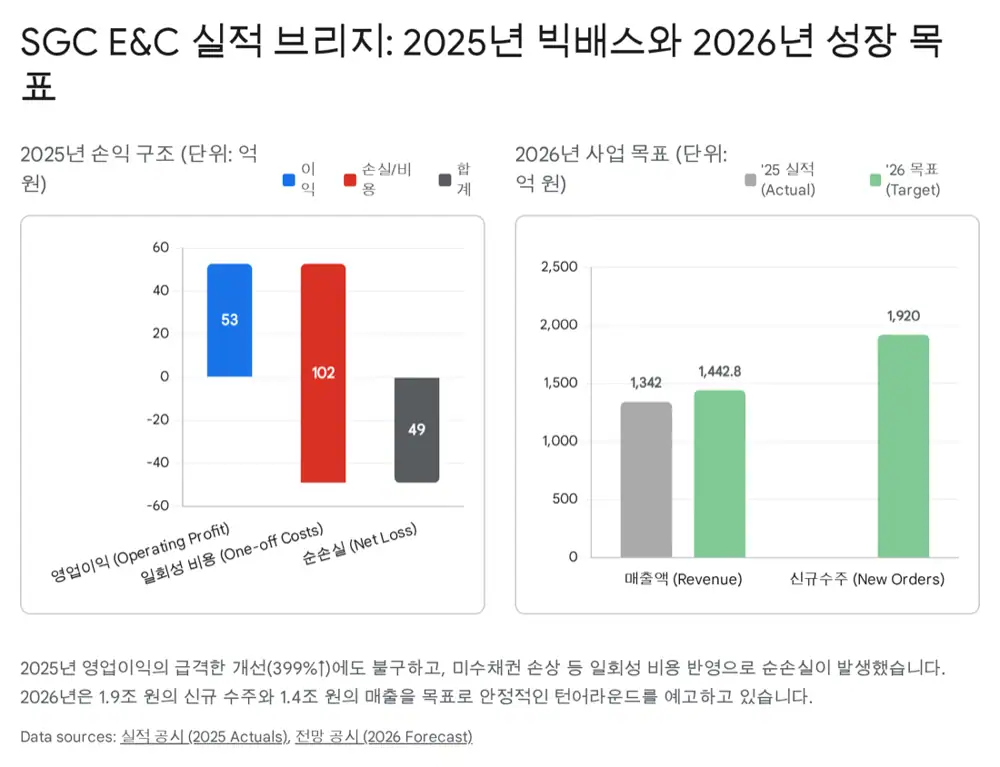

The key point I see in SGC E&C is not the 2025 net loss itself, but the cleanup embedded in it. Core operations recovered to KRW 1.342 trillion in revenue and KRW 52.7 billion in operating profit, but the company recognized a KRW 65.3 billion to KRW 65.4 billion net loss because of one-off non-operating costs such as receivables impairment. I read this as bottoming work ahead of a 2026 turnaround.

The company guided for KRW 1.92 trillion in new orders, KRW 1.4428 trillion in revenue, and KRW 50.9 billion in operating profit for 2026. I view these numbers not as simple top-line ambition, but as a backlog rebuild plan that depends on Saudi and Malaysian chemical plants, OCI/SGC captive demand, and reduced exposure to domestic housing risk.

1. Roots and business structure

Official fact: The source traces SGC E&C's engineering capability to OCI's former technical department, originally established in 1967. Youngchang Construction was founded in 1982, but the company's engineering identity was cemented in 1997 when it acquired OCI's technical department. It became E-Tech Construction in 2005, was reorganized with the SGC Group in 2020, and changed its name from SGC E-Tech Construction to SGC E&C in March 2024.

The company is closer to a chemical-process EPC firm than a general civil and building contractor. It is a KOSDAQ-listed company applying K-IFRS since 2011, headquartered at 246 Yangjae-daero, Seocho-gu, Seoul, and run by co-CEOs Lee Woo-sung and Lee Chang-mo.

Plant EPC

Petrochemical, fine chemical, semiconductor/LCD, and power facility EPC are the core. Process experience in polysilicon, carbon black, soda ash, and other OCI-group chemicals acts as a technical moat.

Construction and housing

The company handles civil/building works and owns the residential brand THE LIV. It grew in mixed-use, officetel, and knowledge-industry-center niches, but domestic real-estate PF risk is now the key issue.

Logistics and others

Warehouse operation/leasing, bonded warehousing, and cold-chain expansion through Westside Logistics diversify the portfolio and add recurring income.

Official fact: SGC E&C belongs to the OCI business group under Korean fair-trade rules. As of September 30, 2025, the largest shareholder was SGC Energy with about 56.79%.

Interpretation: O&M, new CAPEX, the Malaysian OCIM polysilicon expansion, and domestic biomass conversion projects from SGC Energy and OCI affiliates provide captive demand. OCI Group credibility can also help with performance guarantees and financing for overseas projects.

2. 2025 results: growth and loss in the same year

| Item | 2024 | 2025 preliminary | Change | My read |

|---|---|---|---|---|

| Revenue | KRW 1.2056tn | KRW 1.342tn | +11.3% | Top-line recovery from Saudi and Malaysian plant progress |

| Operating profit | KRW 10.6bn | KRW 52.7bn | +399.7% | Core earnings recovered through cost-rate improvement and SG&A control |

| Net profit/loss | -KRW 49.0bn | -KRW 65.3bn to -65.4bn | Loss widened about 33.3% | One-off non-operating costs, including impairment of receivables |

Official fact: On February 3, 2026, the company disclosed preliminary 2025 results showing revenue growth, operating-profit recovery, and a wider net loss. The source attributes the wider net loss to large one-off non-operating expenses including receivables impairment.

Interpretation: I read this as a big bath. By recognizing mostly non-cash accounting costs in 2025, the company appears to be clearing doubtful receivables and potentially impaired assets in order to reduce earnings drag after 2026.

3. 2026 guidance and order strategy

| Category | 2025 result | 2026 target | Meaning |

|---|---|---|---|

| New orders | - | KRW 1.92tn | Backlog rebuild target, about 143% of 2025 revenue |

| Revenue | KRW 1.342tn | KRW 1.4428tn | YoY growth of +7.5% |

| Operating profit | KRW 52.7bn | KRW 50.9bn | Profit-focused internal discipline rather than pure scale |

The new-order target is much larger than the revenue target. The company appears to be treating 2026 as the first year of rebuilding backlog for the next two to three years, which assumes major performance in overseas plant projects rather than domestic housing.

Keeping the operating-profit target near 2025's KRW 52.7 billion, at KRW 50.9 billion, suggests selective bidding and margin control rather than aggressive low-margin growth. I see that conservatism as an important post-big-bath signal.

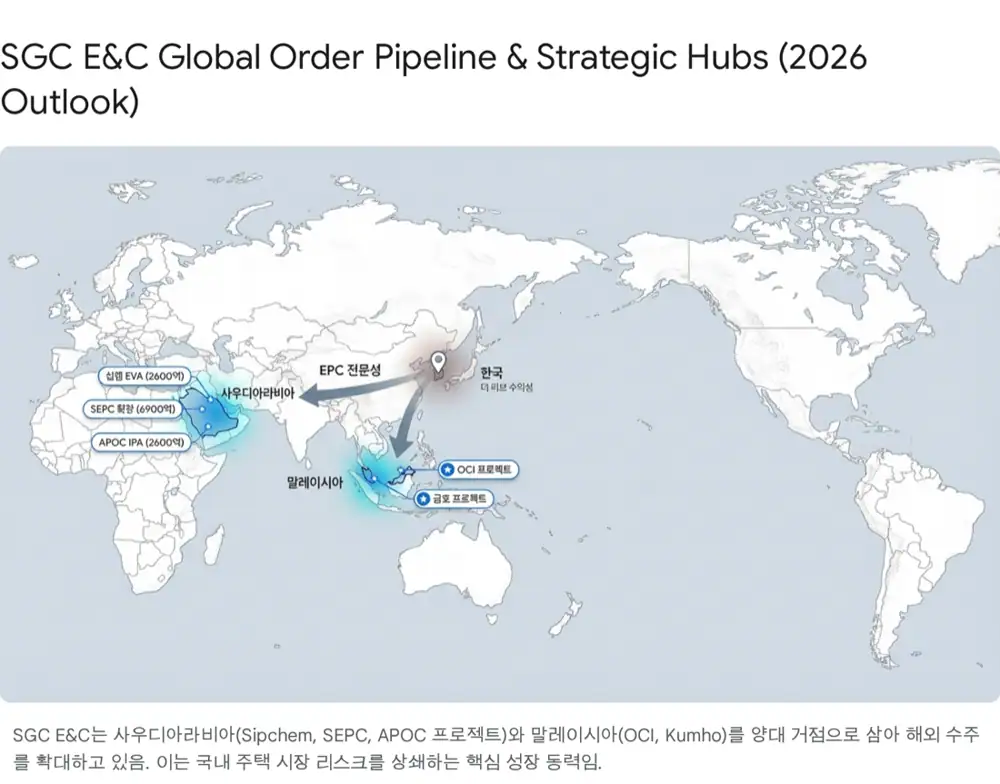

4. Competitive advantage and end markets

SGC E&C's strongest moat is its understanding of chemical processes. While general contractors are strongest in structures, SGC E&C differentiates itself through EPC capability that includes process engineering and commissioning.

- It has experience in specialized chemical facilities such as ethylene vinyl acetate (EVA), isopropyl alcohol (IPA), and polysilicon. Polysilicon plants in particular require demanding high-purity controls.

- Four consecutive projects with Saudi Sipchem are a strong global reference and can raise future bidding success rates.

- Saudi Arabia is expanding investments to turn crude oil into higher-value chemical products through Vision 2030 and oil-to-chemicals strategy. The source says the Middle East petrochemical market could grow at a 6.7% CAGR from 2025 to 2033 to reach USD 29.4 billion.

- The SEPC ethylene cracker expansion is expected to begin production in the first half of 2026, and the Sipchem EVA plant expansion is expected to be completed in 2027.

Domestic construction, by contrast, remains difficult through 2026. PF restructuring from high interest rates and higher construction costs, unsold regional housing, and housing-market polarization can pressure cash flow. Some research expects construction investment to bottom and grow 2.6% in 2026, but near-term profitability improvement in domestic construction will likely be difficult.

5. Risks: business suspension lawsuit and balance-sheet burden

Official fact: The biggest valuation discount comes from the eight-month business suspension administrative order related to the 2023 Anseong logistics warehouse collapse. The company obtained a stay of execution, so current operations are not affected, and the main cancellation lawsuit is ongoing.

Win or reduced penalty

Removing uncertainty could become a strong catalyst for both orders and the stock.

Loss and final penalty

A confirmed suspension could block public-project bidding and new orders for eight months, potentially creating revenue gaps, credit-rating pressure, and cross-default risk.

Financial health

The source cites a debt ratio of about 252% at end-3Q25. Initial working capital for large overseas projects and high interest costs remain variables.

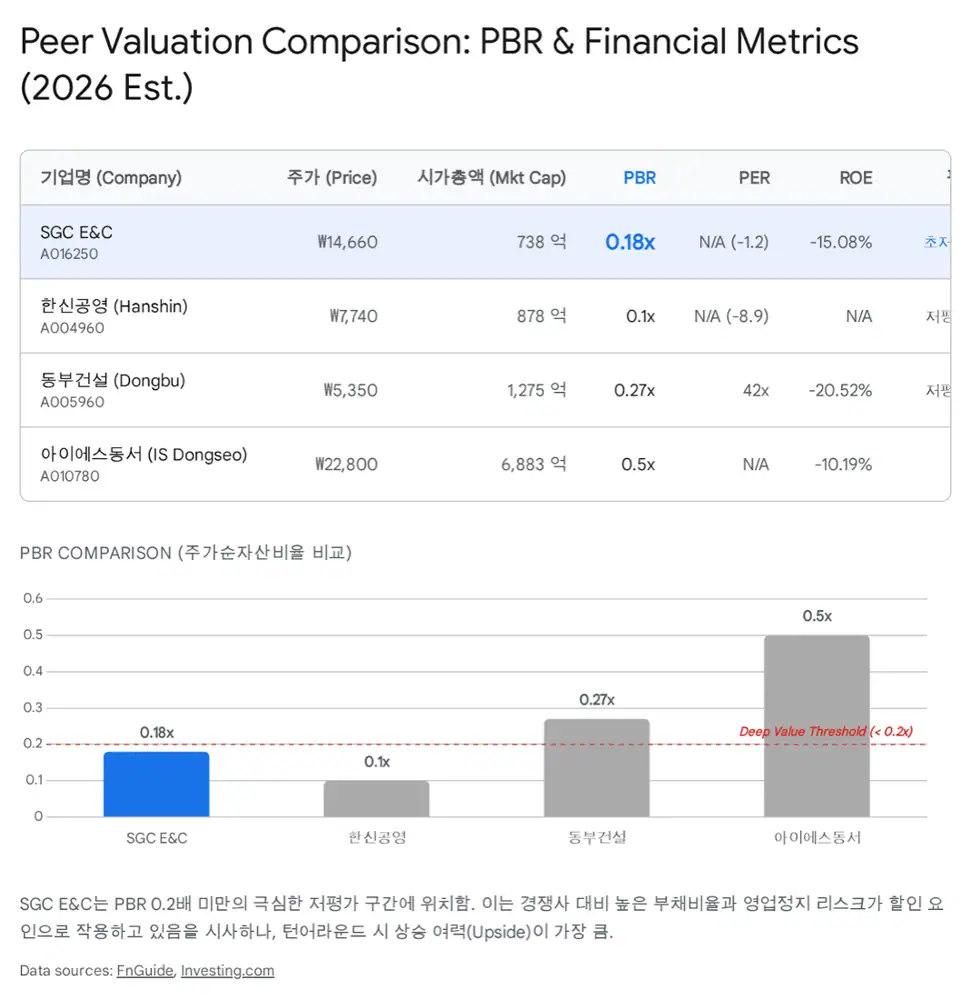

6. Valuation and strategy

The source says the stock trades below 0.2x PBR, far below net asset value. It also compares the company with IS Dongseo at 0.5x PBR and Dongbu Construction at 0.27x PBR.

Interpretation: Low PBR is both an opportunity and a warning that the market is weighing the suspension lawsuit, 2025 earnings shock, and weak construction-sector sentiment more heavily than the turnaround case. The source mentions a first target near KRW 25,000, or 0.3x to 0.4x PBR, but that depends on successful earnings recovery and industry improvement.

Bull Case

- Potential bad assets were proactively cleaned up through the 2025 big bath.

- Overseas plant backlog, including Saudi projects, could convert into revenue and profit from 2026.

- The valuation is near the floor at roughly 0.2x PBR.

- OCI and SGC group captive demand provides support.

Bear Case

- Losing the business-suspension administrative lawsuit could damage fundamentals.

- Further deterioration in domestic housing could turn PF contingent liabilities into real risk.

7. Final take

SGC E&C is preparing for a new 2026 cycle after the pain of 2025. I see 2026 as the year to test whether the market can reclassify the company from a mid-sized domestic contractor into a chemical plant engineering company with global competitiveness.

The three key checkpoints are: first, progress against the KRW 1.92 trillion new-order target; second, stability of profits after 1Q26; and third, the status of the main business-suspension lawsuit. If all three improve together, the discount below 0.2x PBR can be re-evaluated.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170325613

- Quarterly report (2025.11.14), fair disclosure on consolidated operating outlook (2026.02), disclosure on revenue/profit structure change of 30% or more (2026.02), FnGuide and securities reports, overseas plant and petrochemical industry outlooks, domestic construction and real-estate market outlooks

- Saudi Arabia's flagship mega-projects signal industrial transformation era: https://ognnews.com/Article/48042/Saudi_Arabia%E2%80%99s_flagship_mega-projects_signal_industrial_transformation_era

- SGC E&C Secures $366 Million Contract for Saudi Arabia Chemical Plant - ChemAnalyst: https://www.chemanalyst.com/NewsAndDeals/NewsDetails/sgc-e-c-secures-366-million-contract-for-saudi-arabia-chemical-plant-29973

- '안성 물류창고 추락사고' SGC이테크건설 8개월 영업정지 - 연합뉴스: https://www.yna.co.kr/view/AKR20231005079200004

- Asia 2026: 6 questions for Korea's recovery | articles - ING Think: https://think.ing.com/articles/korea-outlook-2026-6-questions-for-korea-in-2026/

- South Korea's Construction Investment Plummets 9.9%: https://www.chosun.com/english/market-money-en/2026/01/23/FXLJAHVHLRDLFOMTJ7NUTZ5EVI/

- SGC E&C(A016250) 경쟁사비교 - Company Guide: https://comp.fnguide.com/SVO2/asp/SVD_Comparison.asp?pGB=1&gicode=A016250&cID=&MenuYn=Y&ReportGB=&NewMenuID=106&stkGb=701

- SGC E&C Completes Malaysia Project Using Plant Modularization - The financial news: https://en.fnnews.com/news/202512171332122840

- Revenue For SGC Energy Co Ltd (A005090) - Finbox: https://finbox.com/KOSE:A005090/explorer/total_rev/

- SGC E&C 해외 수주 단숨에 1조 원 돌파 - 소비자가 만드는 신문: https://www.consumernews.co.kr/news/articleView.html?idxno=721650

- SGC E&C (KOSDAQ:016250) Revenue - Stock Analysis: https://stockanalysis.com/quote/kosdaq/016250/revenue/

- SGC E&C secures $189 mn petrochem facility project in Saudi Arabia - KED Global: https://www.kedglobal.com/construction/newsView/ked202408080009

- SGC lands $191mln EPC contract for Advanced petchem plant - ZAWYA: https://www.zawya.com/en/business/energy/sgc-lands-191mln-epc-contract-for-advanced-petchem-plant-p2gcbzt3

- Middle East Petrochemicals Market | Industry Report, 2033 - Grand View Research: https://www.grandviewresearch.com/industry-analysis/middle-east-petrochemicals-market-report

- ARCC signs contract with SGC Arabia for SEPC ethylene cracker plant expansion - Hydrocarbon Processing: https://www.hydrocarbonprocessing.com/news/2024/02/arcc-signs-contract-with-sgc-arabia-for-sepc-ethylene-cracker-plant-expansion-in-saudi-arabia/

- EPC Contractor Sealed for Major Plant Expansion in Saudi Arabia - Gulf Fire: https://gulffire.com/epc-contractor-sealed-for-major-plant-expansion-in-saudi-arabia/

- Korea's Economic Outlook for 2026 and Its Policy Implications: https://www.kif.re.kr/kif4/publication/viewer?mid=220&cno=357139&ism=1&fcd=2025013986TK&ft=0&email=[$email]

- SGC E&C 투자분석 2025. 11. 30 - 주달: https://www.judal.co.kr/?view=stockAI&shareToken=GUOzhofRoPM2UZVv

- SGC E&C Co Ltd Compare against Competitors - Investing.com NG: https://ng.investing.com/pro/KOSDAQ:A016250/compare/KOSDAQ:A037350,KOSE:A005960,KOSDAQ:A045100,KOSE:A028100,KOSDAQ:A011560,KOSE:A004960

- SGC E&C Co Ltd Compare against Competitors - Investing.com: https://www.investing.com/pro/KOSDAQ:A016250/compare/KOSDAQ:A037350,KOSDAQ:A045100,KOSE:A005960,KOSE:A053690,KOSE:A126720,KOSDAQ:A011560

- SGC E&C(A016250) 경쟁사비교 - Company Guide: https://comp.fnguide.com/SVO2/asp/SVD_Comparison.asp?pGB=1&gicode=A016250&cID=30&MenuYn=Y&ReportGB=&NewMenuID=106&stkGb=701

- 2026년 건설업 전략 전환 외형 확장 멈추고 리스크 관리로 - 프라임경제: https://m.newsprime.co.kr/section_view.html?no=718992&menu=1