DEEP RESEARCH · CHEMTROS

Chemtros: Where Materials Localization Meets the Advanced-Industry Supercycle

A review of the precision-chemistry platform spanning EUV PAG, hafnium precursors, electrolyte additives, PVDF, CCU, and ionomers

0. Bottom line first

My core read is that Chemtros is not just a commodity chemicals name. It is a custom synthesis platform extending into semiconductors, secondary batteries, and clean-energy materials. The KRW 35 billion BW financing and Jincheon Plant 3 were burdensome investments, but the December 2025 EUV-material mass-production news and the expected 2H26 hafnium precursor patent cliff could mark the shift into harvest mode.

Official fact: The source analyzes Chemtros through three pillars: semiconductor materials, secondary-battery materials, and clean-energy/hydrogen materials.

Interpretation: The moat is not bulk chemistry. It is the ability to design molecules for customer-specific properties and turn those recipes into manufacturable processes.

1. Industry backdrop

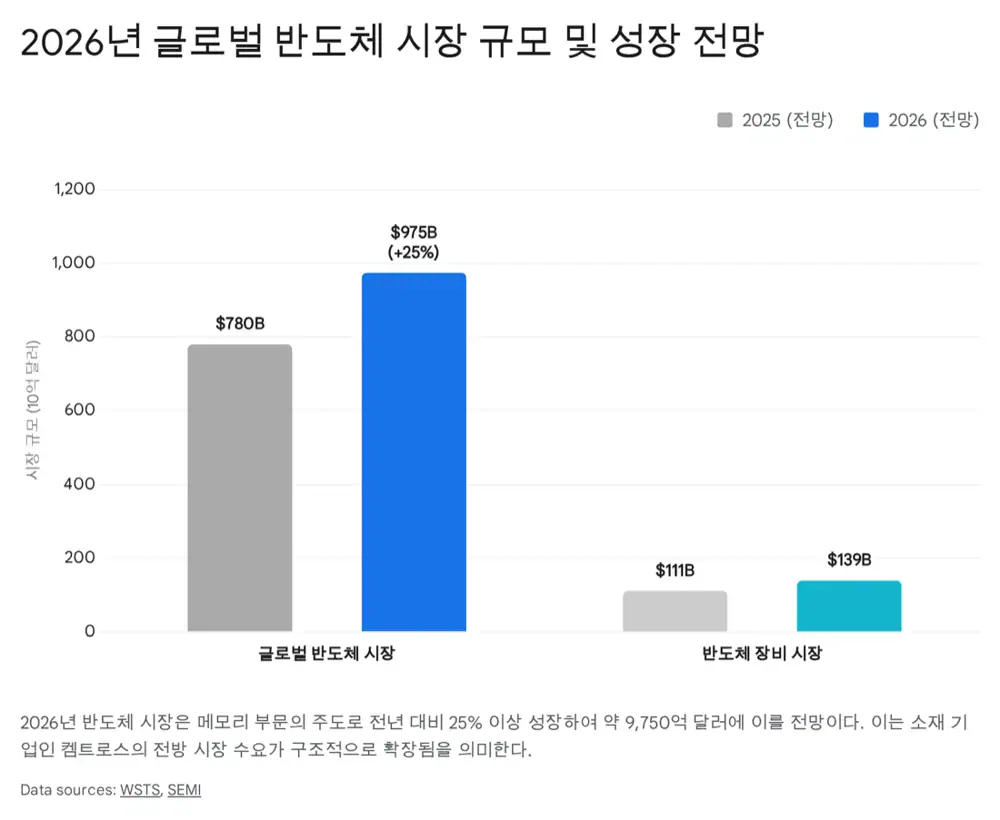

Official fact: The post cites a 2026 global semiconductor market outlook of more than 25% growth to nearly USD 975 billion, roughly KRW 1,300 trillion, with memory expected to grow in the 30% range.

AI data-center expansion drives HBM, DDR5, and AI accelerator demand. As processes move below 7nm and toward 2nm, EUV layer counts rise and specialty process chemicals become more important.

Official fact: The source presents the electrolyte market growing from USD 14.0 billion in 2025 to USD 15.86 billion in 2026.

Interpretation: Battery additives benefit from the need for higher energy density, faster charging, and stronger fire safety. Chemtros’ B2B additive model is directly tied to downstream production volume.

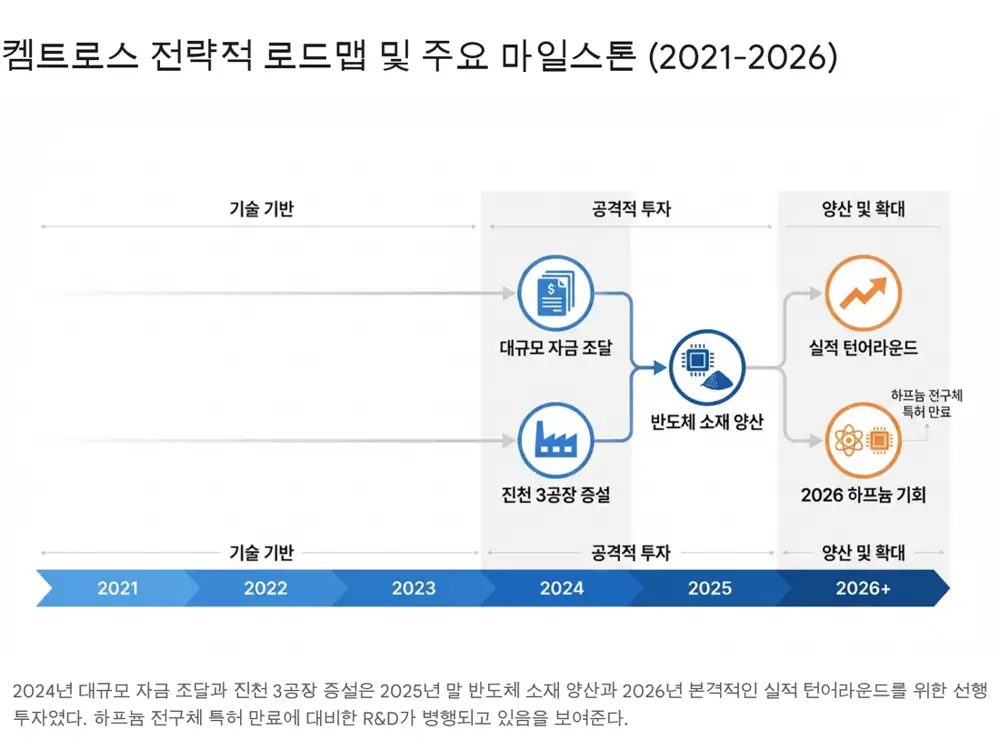

2. Investment-to-harvest timeline

| Period | Key development | Meaning |

|---|---|---|

| 2021-2023 | R&D for EUV photoresist materials and battery additives, plus national projects | Technology accumulation |

| 2024-2025 | KRW 35 billion BW in July 2024 and Jincheon Plant 3 completed in 1H25 | Aggressive investment |

| 2026 | Higher Plant 3 utilization and December 2025 semiconductor-material production news | Harvest phase begins |

3. Semiconductor materials

EUV PAG generates acid under 13.5nm EUV exposure and helps form photoresist patterns. The post interprets the December 8, 2025 production news as a signal of PAG localization.

Interpretation: Local PAG supply can reduce dependence on Japanese suppliers such as JSR, TOK, and Shin-Etsu and give domestic photoresist makers and chip customers a more stable supply chain.

Hafnium precursors are tied to DRAM scaling and High-K dielectrics. The source frames the expected 2H26 expiration of key Versum/Merck-related patents as an opening for Korean materials suppliers, while citing a domestic market estimate above KRW 300 billion.

PAG localization

A high-difficulty synthesis area requiring efficient acid generation and diffusion control.

Hafnium precursors

A next-growth candidate tied to High-K demand and patent-expiration timing.

Jincheon Plant 3

The newest capacity must prove production quality, yield, and customer qualification.

4. Battery and clean-energy materials

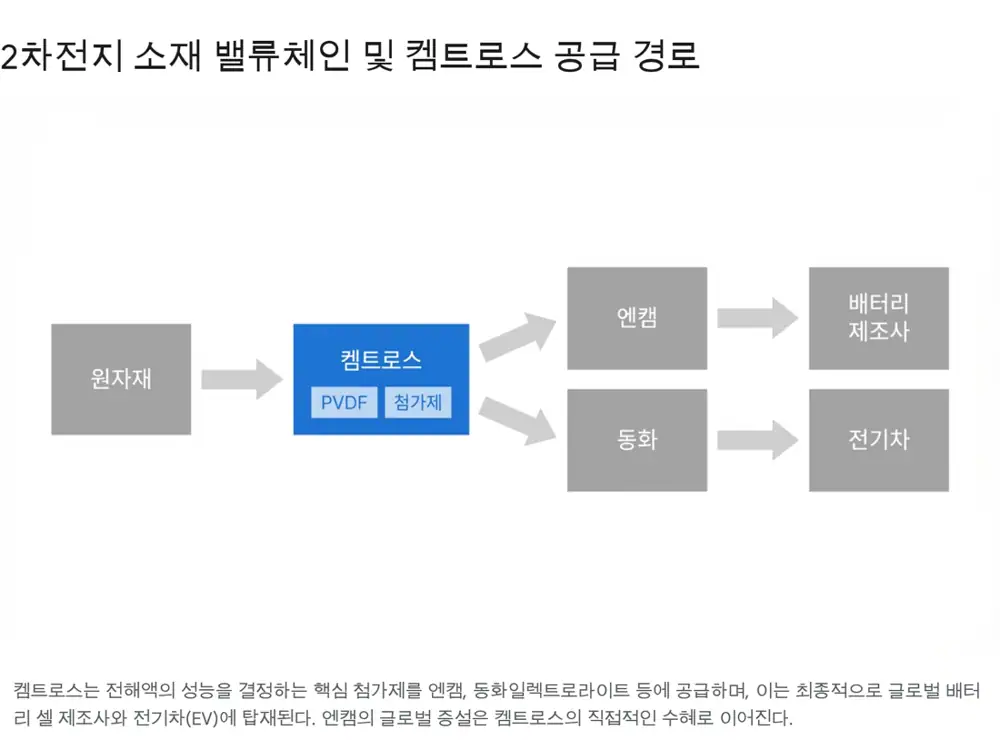

The battery-materials business supplies key additives to electrolyte makers such as Enchem and Dongwha Electrolyte. VEC and PS help form the SEI layer and affect battery life and stability.

PVDF is a fluoropolymer used as a cathode binder and separator coating. The post frames localization as a cost-reduction alternative to materials historically dominated by Solvay and Arkema.

Long-term options include perfluorosulfonic-acid ionomers for fuel cells and electrolysis, plus CCU technology that converts captured CO2 into high-value chemicals such as ethylene carbonate.

5. Risks and checks

- Raw materials: feedstock costs are exposed to oil, lithium, and other macro variables.

- Competition: hafnium precursor opening also means competition with LK Chem, SK Trichem, Lake Materials, and others.

- Overhang: the KRW 35 billion BW can create share-supply pressure.

- Execution: utilization, yield, and customer qualification at Jincheon Plant 3 matter most for 2026 numbers.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170323862

- Source 2: https://news.skhynix.co.kr/2026-market-outlook/

- Source 3: https://contents.premium.naver.com/joosikstudy/atmproject/contents/260127103600961vy

- Source 4: https://www.fetv.co.kr/news/article.html?no=211567

- Source 5: https://www.fortunebusinessinsights.com/ko/industry-reports/battery-electrolyte-market-100986

- Source 6: https://www.mk.co.kr/news/stock/9643990

- Source 7: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240730000187&docno=&viewerhost=&

- Source 8: http://chemtros.com/contact-us/notice/?pageid=4&uid=24&mod=document

- Source 9: http://www.newstnt.com/news/articleView.html?idxno=563913

- Source 10: https://www.chemlocus.co.kr/news/view/125805?url=L25ld3MvZGFpbHkvMjUvMTI/Y2F0ZWdvcnk9MDMwMw==

- Source 11: https://www.thelec.kr/news/articleView.html?idxno=29848

- Source 12: https://www.thelec.kr/news/articleView.html?idxno=32730

- Source 13: https://www.thelec.kr/news/articleView.html?idxno=19289

- Source 14: https://ssl.pstatic.net/imgstock/upload/research/company/1617926673594.pdf

- Source 15: https://batterydive.com/901547