DEEP RESEARCH · HWASEUNG CORPORATION

Hwaseung Corporation: A KRW 37 Billion Tech Center and the Shift to Green Materials

How a CMB-centered operating holding company is moving toward TPE, clean processes, and EV thermal-management materials

0. Bottom line first

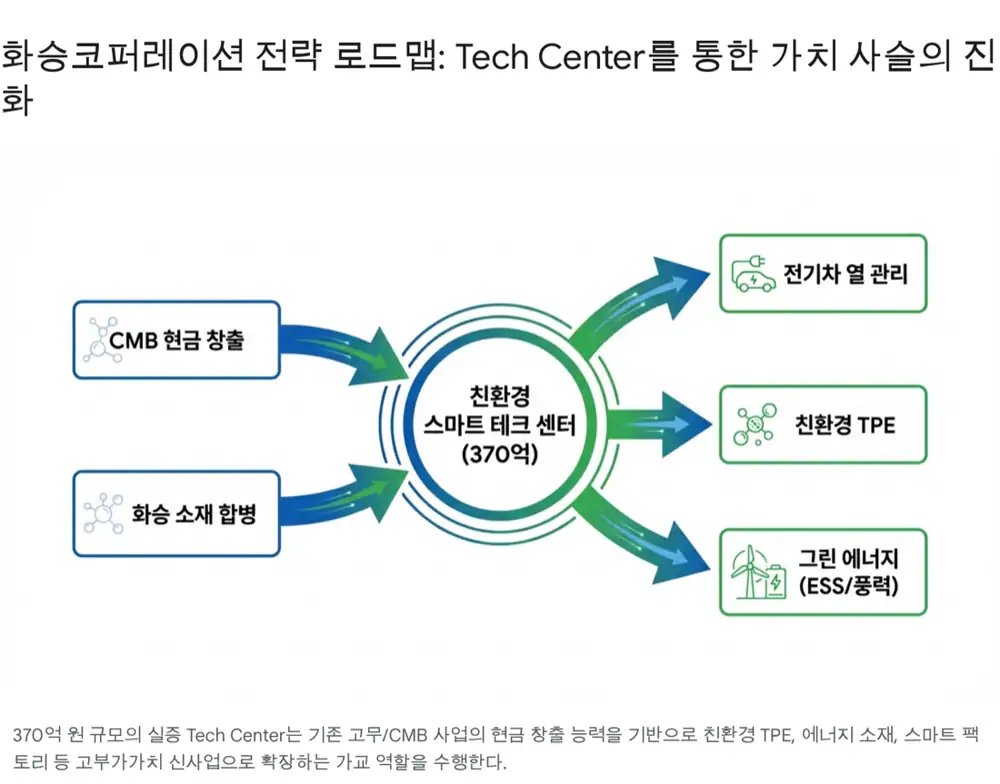

Hwaseung Corporation’s KRW 37 billion empirical Tech Center is not just a lab expansion. It is a strategic site combining green process validation, ICT manufacturing, and mass-production checks for TPE and EV materials. The key question is whether this can reduce the holding-company discount and earn a materials-company premium.

Official fact: The source says Hwaseung strengthened its operating-holding-company profile after the 2021 spin-off and established that identity after absorbing Hwaseung Materials in 2023.

Interpretation: The Tech Center is the physical expression of merger synergy, moving the business from stable but lower-growth CMB toward TPE, bio materials, ESS, offshore wind, and EV thermal-management materials.

1. What the Tech Center is meant to do

The source frames dust adsorption and filtration, waste-oil and waste-heat recycling, and solar-linked energy models as core environmental functions.

It also describes a smart-factory role: AI and IoT sensors collect data across raw-material input, mixing, and processing, then test intelligent compounding systems across variables such as temperature, pressure, and time.

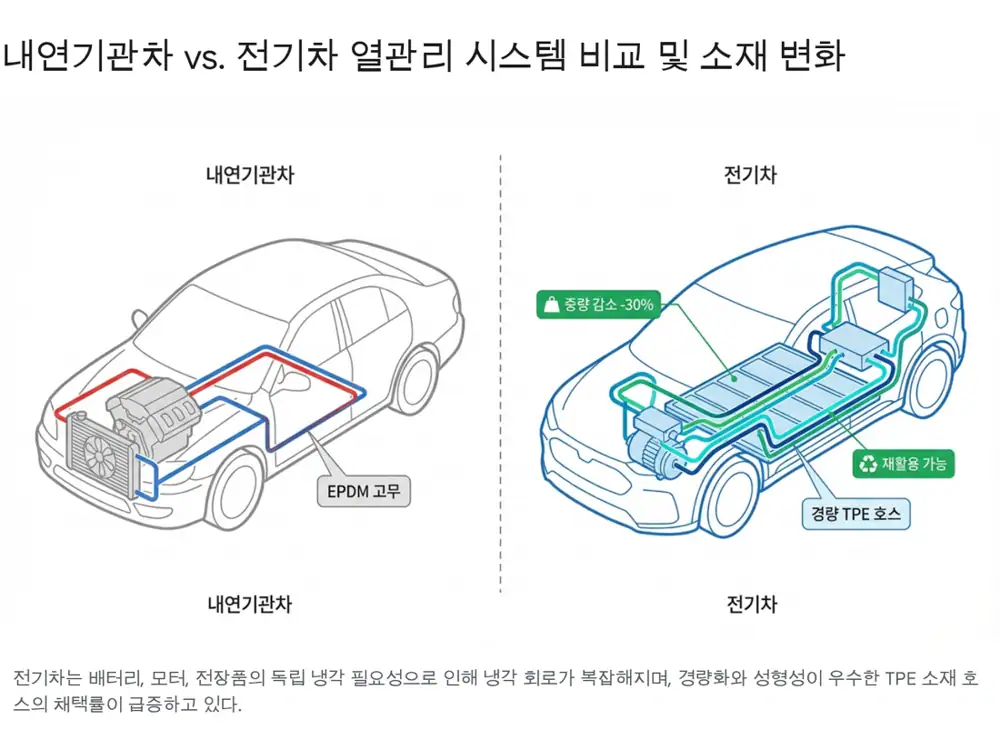

2. Material transition: TPE and lightweighting

Official fact: The post says Hwaseung is No. 1 in Korea’s TPE market and connects TPE, which can reduce weight by more than 30% versus conventional rubber, to EV driving-range improvement.

Rubber plus plastic

Elasticity and processability support lightweighting and recycling trends.

Thermal hoses

Complex thermal-management systems in EVs and hybrids create higher-value materials demand.

Clean Factory

The source frames this as a way to meet stricter global OEM supply-chain standards.

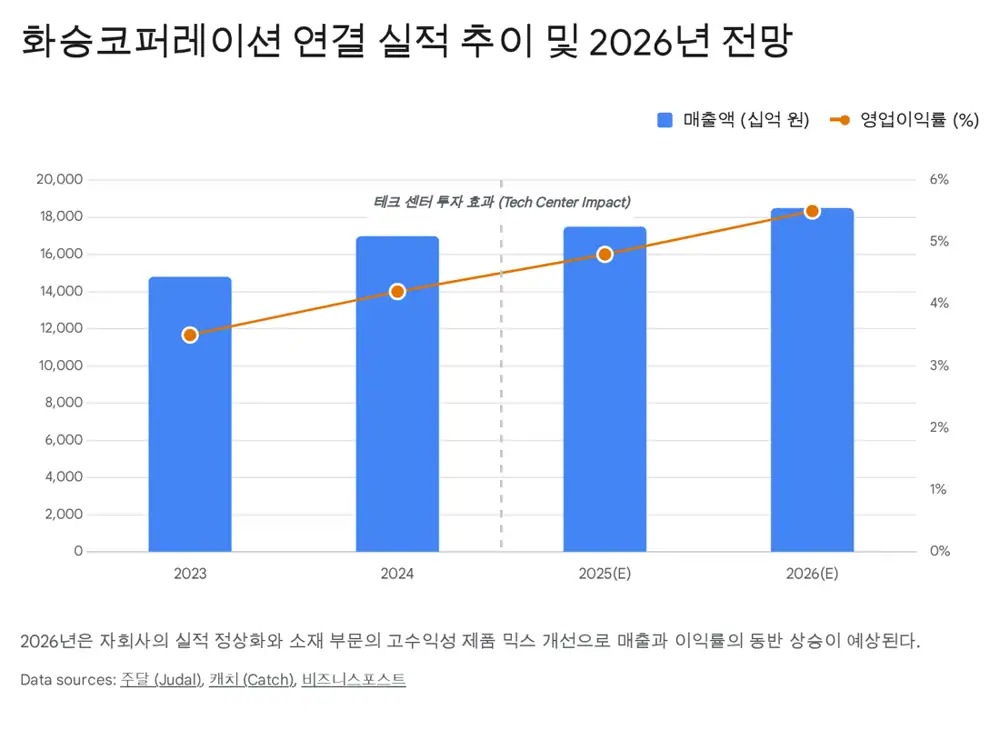

3. Subsidiaries and consolidated earnings

The source points to Hwaseung R&A expanding from Hyundai Motor Group toward emerging EV makers such as BYTON and VinFast, while Hwaseung Enterprise may recover as Adidas inventory adjustment ends and the 2026 World Cup approaches.

| Item | Source assumption | Check |

|---|---|---|

| 2026 revenue | 8-10% growth vs. 2025 estimate, around KRW 1.85 trillion | EV parts, Adidas utilization, TPE mix |

| Operating profit | Mid-5% OPM, around KRW 100 billion | Mix improvement and smart-factory gains |

| Valuation | P/B around 0.4-0.5x | Tech Center results and shareholder returns |

4. SOTP valuation frame

The source’s SOTP uses KRW 40 billion of 2026E EBITDA for the core materials/industrial-rubber business, a 6.0x EV/EBITDA multiple, about KRW 240 billion of value, KRW 22 billion for the Hwaseung R&A stake, KRW 150 billion from Hwaseung Enterprise, at least KRW 100 billion of unlisted subsidiaries and real estate, and KRW 150 billion of net debt, producing NAV of about KRW 365 billion.

Interpretation: The real issue is whether the center leads to new orders, green certifications, and a higher-margin materials mix, not the multiple itself.

5. Risks

- Raw materials: synthetic rubber and TPE feedstocks are oil-sensitive.

- EV chasm: prolonged EV demand softness could delay EV hose and materials growth.

- Governance: complex group structure and related-party transactions can sustain a Korea discount.

- Shareholder returns: buybacks, cancellations, and dividends matter for resolving low P/B valuation.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224170322136

- Source 2: https://www.hwaseunggroup.com/waybbs/way_bbs.php?bo_table=press&wr_id=95&page=0

- Source 3: https://www.todayenergy.kr/news/articleView.html?idxno=259810

- Source 4: https://www.yna.co.kr/view/AKR20230425032400051

- Source 5: https://m.etnews.com/20220214000149?obj=Tzo4OiJzdGRDbGFzcyI6Mjp7czo3OiJyZWZlcmVyIjtOO3M6NzoiZm9yd2FyZCI7czoxMzoid2ViIHRvIG1vYmlsZSI7fQ%3D%3D

- Source 6: https://www.hsrna.com/hscmb/index.php?pCode=notice&mode=fdn&idx=216244&num=1

- Source 7: https://www.chemlocus.co.kr/news/view/131438

- Source 8: https://www.hsrna.com/hsrna/index.php?pCode=MN000174&mode=view&idx=2648

- Source 9: https://hsrna.com/hsrna/index.php?pCode=pressrelease_02&mode=view&idx=2870

- Source 10: https://www.hsrna.com/hsrna/index.php?pCode=pressrelease_01&mode=view&idx=2633

- Source 11: https://static.roa.ai/research/company/20250306_company_352741000.pdf

- Source 12: https://www.etoday.co.kr/news/view/2512090

- Source 13: https://seo.goover.ai/report/202511/go-public-report-ko-0f75f355-2107-4ce3-af31-072c0fda93db-0-0.html

- Source 14: https://www.judal.co.kr/?view=stockAI&shareToken=1qegokGVjXHHBvfe

- Source 15: https://www.hsrna.com/hsrnaen/index.php?pCode=group

- Source 16: https://www.hsrna.com/hsrna/index.php?pCode=MN000175&mode=view&idx=2780

- Source 17: https://plus.hankyung.com/apps/newsinside.view?aid=202212107251Y&category=&sns=y

- Source 18: https://www.yna.co.kr/view/AKR20221209056600051

- Source 19: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250321001771&docno=&viewerhost=&

- Source 20: https://hsrna.com/hsrna/index.php?pCode=pressrelease_01&mode=view&idx=2679

- Source 21: https://www.asiatoday.co.kr/kn/view.php?key=20231101010000743

- Source 22: https://seo.goover.ai/report/202508/go-public-report-ko-cbbc7bb3-e6f0-4c86-8f4e-68e01fb26e83-0-0.html

- Source 23: https://www.360researchreports.com/market-reports/automotive-coolant-hose-market-214478

- Source 24: https://www.hwaseunggroup.com/eng/sub02/sub01.php

- Source 25: https://www.hwaseunggroup.com/waybbs/way_bbs.php?bo_table=press&wr_id=38&page=4

- Source 26: https://www.businesspost.co.kr/BP?command=article_view&num=356637

- Source 27: https://www.kookje.co.kr/news2011/asp/newsbody.asp?code=0200&key=20170726.22013005096

- Source 28: https://www.youtube.com/shorts/Y7q-tCxGp1o

- Source 29: https://www.hwaseunggroup.com/waybbs/way_bbs.php?bo_table=press&wr_id=20&page=7

- Source 30: https://www.judal.co.kr/?view=stockAI&shareToken=HkFRCEP9cxw3d3gY

- Source 31: https://www.judal.co.kr/?view=stockAI&shareToken=7VkLUroyooH8EVDQ

- Source 32: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240531000468&docno=&viewerhost=&