DEEP RESEARCH · SAMSUNG SDI ESS CONTRACT

Samsung SDI Supply Contract Analysis: Tesla ESS Value Chain and North America Pivot

A review of what the January 30, 2026 confidential supply disclosure implies for ESS, LFP, and Indiana line conversion.

0. Bottom line first

I read this disclosure as more than a battery supply order. It signals Samsung SDI’s strategic expansion into North American ESS and LFP supply chains. The official disclosure hides the counterparty and value, but the source treats its link to the November 2025 Tesla ESS rumor inquiry as the key clue.

Confidential until 2030

The counterparty, contract value, and period were kept confidential until January 1, 2030 for business-confidentiality reasons.

Prismatic LFP ESS

The source identifies the core product as prismatic LFP batteries for ESS, potentially using SBB 2.0 technology.

Indiana conversion

Part of StarPlus Energy’s EV battery line is interpreted as being converted to ESS LFP to protect utilization and capture IRA benefits.

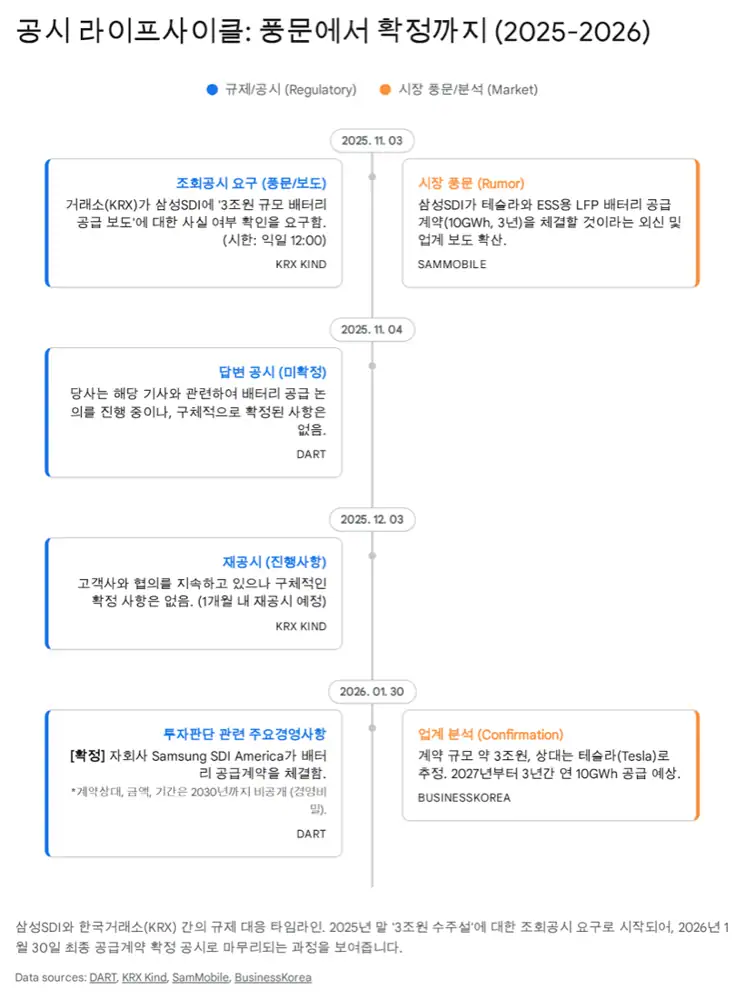

1. Disclosure framework: separating facts from inference

Official fact: According to the source, on January 30, 2026 Samsung SDI made a final disclosure that Samsung SDI America, Inc. had signed a large battery supply contract. The counterparty, value, and contract period are confidential until January 1, 2030.

Official fact: The disclosure is framed as the final response to the Korea Exchange’s November 3, 2025 inquiry on rumors or media reports. The key report at the time was that Samsung SDI was discussing an ESS battery supply contract with Tesla worth KRW 3 trillion.

Interpretation: Tesla as the customer is the source author’s inference, not an official disclosed fact. Still, the source sees the shift from “under discussion” to “contract signed” within the same inquiry chain as a strong clue.

2. Product and production site: LFP, SBB 2.0, and Indiana

The source sees prismatic LFP batteries for ESS as the core product. Samsung SDI has historically been strong in NCA ternary batteries, but ESS demand is moving toward LFP because price competitiveness and fire safety matter more.

- LFP transition: the source argues Tesla Megapack’s prismatic LFP design fits Samsung SDI’s prismatic form-factor capabilities.

- SBB 2.0: high-capacity LFP cells and direct-injection thermal-runaway prevention are presented as safety features for critical infrastructure such as data centers.

- Production site: because the disclosing entity is Samsung SDI America, the source points to the StarPlus Energy plant in New Carlisle, Indiana.

- Line conversion: EV demand weakness at Stellantis creates a reason to convert potential idle capacity into ESS LFP production.

Official fact: The source cites IRA advanced-manufacturing production credits of up to $45 per kWh. Its later financial estimate uses a $35-$45 per kWh range.

3. Value-chain partners: Capex and Opex beneficiaries

| Category | Company | Source role |

|---|---|---|

| Equipment | MOT | Core prismatic assembly equipment such as jelly-roll insertion, can insertion, and cap welding |

| Equipment | Wonik PNE | Formation-process equipment, high-performance cyclers, and inspection systems |

| Equipment | Hana Technology and Toptec | Potential logistics automation and tab-welding equipment for line retrofits |

| Parts | Shinheung SEC | Cap assemblies for prismatic-battery safety, with local production near Indiana |

| Parts | Sangsin EDP | Aluminum cans for prismatic batteries and high Samsung SDI can exposure |

| Materials | EcoPro BM, L&F, Kangwon Energy | LFP cathode localization, North American sourcing, and lithium-hydroxide-related processing |

Interpretation: Equipment suppliers are better viewed as 2026 line-conversion Capex beneficiaries, while parts and materials suppliers are more Opex-like recurring beneficiaries if full supply starts from 2027.

4. Financial impact: the ESS option missing from consensus

Official fact: The source summarizes brokerage estimates of contract value at about KRW 3 trillion to as much as KRW 5 trillion over three years. Annual revenue contribution is estimated at about KRW 1 trillion to KRW 1.5 trillion, or roughly 5-7% of Samsung SDI’s total revenue.

| Item | Source estimate | Investment angle |

|---|---|---|

| Contract value | About KRW 3-5 trillion over three years | ESS revenue visibility during EV slowdown |

| Annual revenue | About KRW 1-1.5 trillion | 5-7% of total revenue, but a quantum jump for ESS |

| AMPC | $35-$45 per kWh | Margin lift from U.S. local production |

| 10GWh assumption | KRW 450-500 billion annual tax credit | Potentially lifts companywide operating profit by more than 10-15% |

Interpretation: The key is not only revenue size. It is the combination of monetizing idle assets and capturing AMPC. If Indiana utilization is protected by ESS demand, fixed-cost absorption and tax credits can both lift margins.

5. Conclusion: turning a challenged EV asset into ESS infrastructure

The source treats the disclosure as a case in which Samsung SDI pivots capacity from a slowing EV market toward a fast-growing ESS market. The logic combines a likely top-tier customer, Indiana utilization protection, and a new LFP product portfolio.

Interpretation: I see this as an early test of whether Samsung SDI can be reclassified from a pure EV battery maker into an energy-storage infrastructure partner for the AI era. But because the core contract terms remain confidential, customer identity, pricing, and margins must remain estimates.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224167794583

- Source 2: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251203000441&docno=&viewerhost=&

- Source 3: https://kind.krx.co.kr/external/2025/11/03/000764/20251103001708/99812.htm

- Source 4: https://www.thehindu.com/sci-tech/technology/samsung-sdi-says-discussing-supplying-tesla-with-ess-batteries/article70238698.ece

- Source 5: https://biz.chosun.com/en/en-finance/2025/11/04/YNE4SWPYCZGKRAOI32MKH7OMHQ/

- Source 6: http://koreabizwire.com/samsung-sdi-secures-u-s-battery-contract-details-withheld/343311

- Source 7: https://www.sammobile.com/news/samsung-may-have-signed-deal-tesla-ess-batteries/

- Source 8: https://www.sammyfans.com/2026/01/31/samsung-may-have-just-won-tesla-battery-deal-in-the-us/amp/

- Source 9: https://www.businesskorea.co.kr/news/articleView.html?idxno=262165

- Source 10: https://www.samsungsdi.com/sdi-now/sdi-news/4642.html

- Source 11: https://electrek.co/guides/samsung-sdi/

- Source 12: https://electrification-solutions.com/samsung-sdi-gms-3-5b-us-battery-jv-investment-may-face-delay-again/

- Source 13: https://www.chosun.com/economy/industry-company/2026/01/31/LBTEB4NCVFBO7PELUD7WPAOXWE/

- Source 14: https://www.thelec.kr/news/articleView.html?idxno=51670

- Source 15: https://cleantechnica.com/2025/11/04/tesla-to-buy-2-billion-in-lfp-batteries-from-samsung-sdi-gm-project-slowed/

- Source 16: https://news.metal.com/newscontent/103740786/

- Source 17: https://en.sedaily.com/article?id=version_2K7I5XPIPH_20260130_181431

- Source 18: https://m.etnews.com/20260126000059?obj=Tzo4OiJzdGRDbGFzcyI6Mjp7czo3OiJyZWZlcmVyIjtOO3M6NzoiZm9yd2FyZCI7czoxMzoid2ViIHRvIG1vYmlsZSI7fQ%3D%3D

- Source 19: https://koreajoongangdaily.joins.com/news/2025-07-04/business/industry/For-Korea-Inc-Trumps-Big-Beautiful-Bill-is-a-lot-of-pain-some-gain/2345851

- Source 20: https://www.koreaherald.com/article/10541386

- Source 21: https://www.thelec.net/news/articleView.html?idxno=5550

- Source 22: https://www.thelec.kr/news/articleView.html?idxno=35623

- Source 23: https://www.thelec.kr/news/articleView.html?idxno=51235

- Source 24: https://www.thelec.kr/news/articleView.html?idxno=50050

- Source 25: https://www.financialpost.co.kr/news/articleView.html?idxno=240741

- Source 26: https://www.trendforce.com/news/2025/01/02/news-korean-battery-makers-lg-energy-solution-samsung-sdi-and-sk-on-reportedly-hit-by-lower-utilization/

- Source 27: https://www.koreatimes.co.kr/business/companies/20260105/struggling-battery-makers-bet-on-ess-ai-cost-cutting-to-power-2026-rebound

- Source 28: https://www.autodaily.co.kr/news/articleView.html?idxno=541229

- Source 29: https://www.businesspost.co.kr/BP?command=article_view&num=428678

- Source 30: https://www.economidaily.com/view/20260130151653416

- Source 31: https://thelec.net/news/articleView.html?idxno=5160

- Source 32: https://www.koreaherald.com/article/10608634