DEEP RESEARCH · MAERSK / HAPAG-LLOYD

Maersk and Hapag-Lloyd: Two Shipping Strategies After Gemini Cooperation

Using 2025 results to compare an integrated logistics model with a premium liner model

0. Bottom line first

Gemini Cooperation is a shared operating platform, but the two companies’ strategies diverge sharply. Maersk wants to become a global integrator across the whole logistics chain; Hapag-Lloyd wants to monetize liner-shipping quality and terminal control through a Pure Play Plus model.

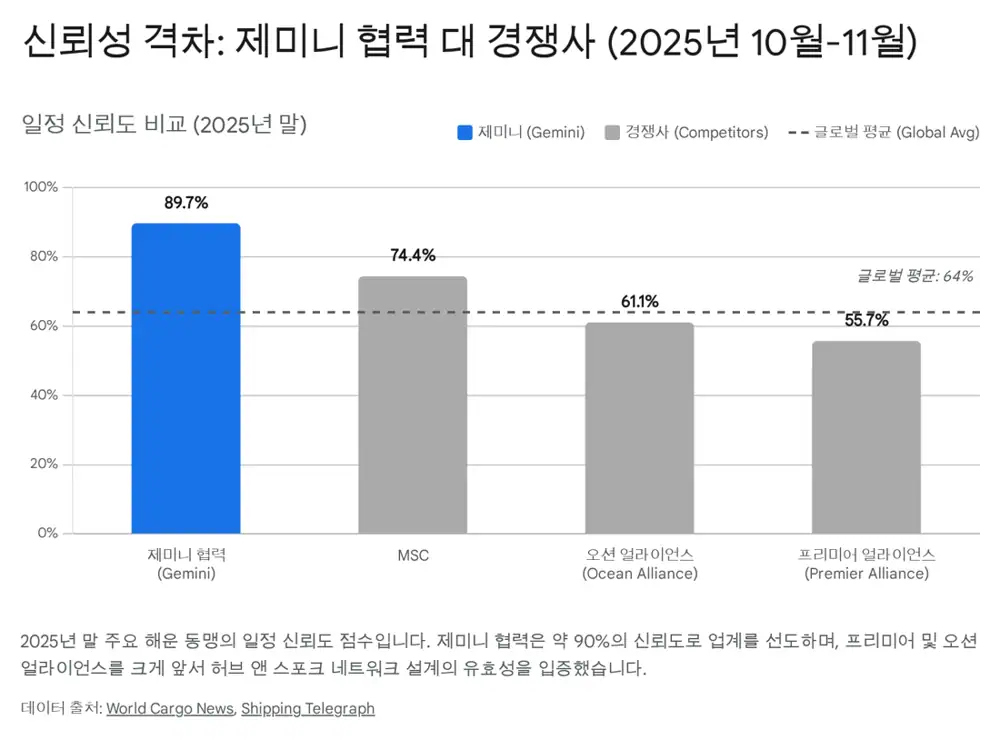

Official fact: The source says Gemini Cooperation launched on February 1, 2025 and recorded 89.7% schedule reliability across all arrivals in October-November 2025. It compares this with Ocean Alliance at 61.1%, Premier Alliance at 55.7%, and MSC at 74.4%.

Interpretation: In container shipping, reliability is not just an operating metric. It is a commercial weapon because it keeps shippers attached even when freight rates fall.

1. Strategy: Integrator vs. Premium Carrier

Maersk’s goal is to become the global integrator of container logistics. It wants to bundle ocean freight, inland transport, air cargo, customs, warehousing, and last-mile delivery into end-to-end solutions. The idea is to reduce ocean-freight volatility through stable logistics margins and customer lock-in.

Hapag-Lloyd follows Pure Play Plus under Strategy 2030. Instead of expanding too far into inland logistics, it focuses on liner-shipping reliability and service quality, then adds terminal infrastructure to protect that quality.

Global Integrator

Builds Logistics & Services to reduce profit volatility when ocean freight rates decline.

Pure Play Plus

Pursues service quality and rate premiums through core liner shipping and terminal control.

2. Gemini Cooperation Performance

Gemini uses a hub-and-spoke model: large mainliners call at a limited number of core hubs, and shuttle vessels distribute cargo to surrounding ports. The older direct-call model allowed one port delay to ripple across an entire service string; Gemini is designed to reduce that structural weakness.

Official fact: The source says Hapag-Lloyd expanded its service network from 113 to 130 services during 9M 2025, mainly through Gemini’s denser shuttle network. Both carriers reported that early cost savings from Gemini were already visible.

Interpretation: If hubs are built around owned or controlled terminals, the network can improve reliability while increasing terminal throughput. Network strategy and terminal strategy become one system.

3. 9M 2025 Results: Growth With Margin Pressure

| Item | Hapag-Lloyd | Maersk |

|---|---|---|

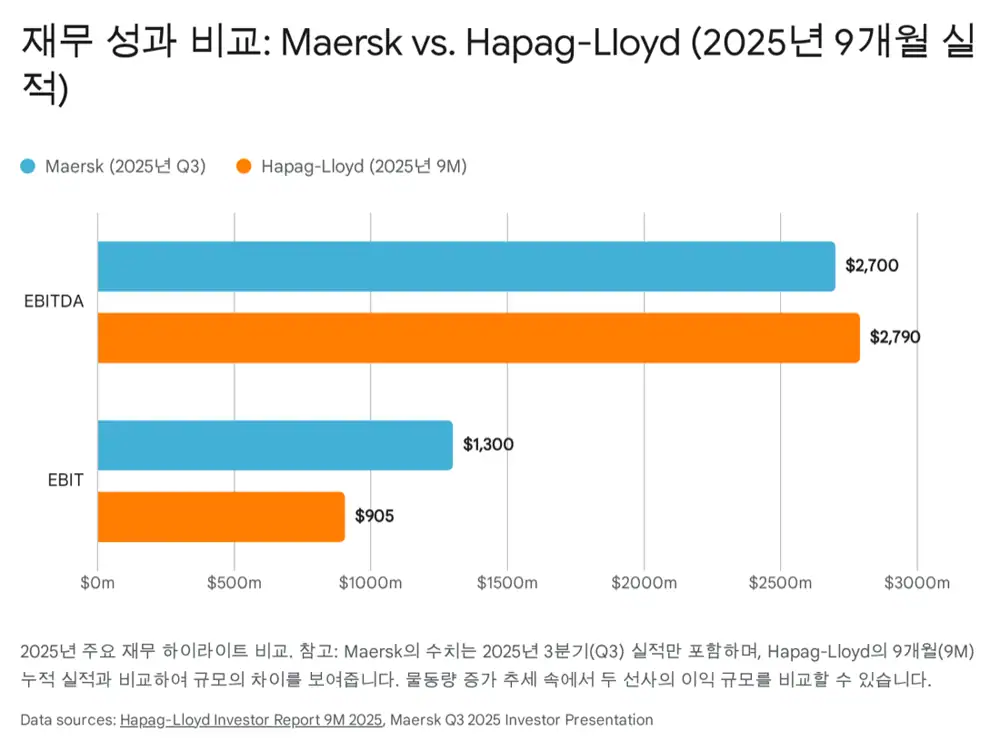

| Core revenue/profit | 9M revenue of $16.0bn, up 5.0% YoY | Q3 EBITDA of $2.7bn and EBIT of $1.3bn |

| Volume | 10.17m TEU, up 9.1% YoY | Ocean volume growth and Gemini cost savings |

| Profit pressure | EBITDA $2.68bn (-23%), EBIT $858m (-54%) | Same rate pressure, partly defended by logistics and terminals |

| Details | Average freight rate $1,397/TEU, down 4.8% YoY | Logistics & Services EBIT margin of 5.5% |

| Balance sheet | Shifted from net cash to $665m net debt, equity ratio 61% | Terminals achieved record-high revenue and profitability |

4. Logistics, Terminals, and Green Fuel Choices

Maersk’s Logistics & Services segment grew revenue 2.3% year on year and showed sequential revenue growth. But it is not yet large enough to fully replace ocean profits, so organic growth and margin improvement remain key proof points.

Hapag-Lloyd’s Terminal & Infrastructure revenue reached $375 million in 9M 2025, up 14.7% year on year. Le Havre terminal acquisition and Brazilian greenfield investment are strategic assets that support Gemini reliability.

Decarbonization also differs. Maersk is the green-methanol first mover, with methanol-powered vessels and supply-chain investments. Hapag-Lloyd is more pragmatic and diversified: 22 newbuilds below 5,000 TEU, biofuels, vessel retrofits, LNG dual-fuel operation, and ZEMBA e-fuel contracts.

5. Valuation and 2026 Outlook

The source places Hapag-Lloyd at about 1.2x P/B and Maersk at about 0.6x P/B as of November 2025. Hapag-Lloyd’s premium reflects its Pure Play model, dividend profile, and Gemini efficiency expectations. Maersk’s discount reflects conglomerate complexity in logistics integration and near-term pressure from green investments.

- Oversupply risk: In 2026, containership orderbook exceeds 30% of the existing fleet and large newbuilding deliveries are expected.

- Maersk watchpoint: Whether logistics profit contribution can meaningfully reduce ocean-cycle volatility.

- Hapag-Lloyd watchpoint: Whether it can maintain roughly 90% Gemini reliability while protecting liner margins and terminal profits.

For investors, Hapag-Lloyd fits a view based on core shipping recovery and dividends, while Maersk fits a view based on global logistics growth and valuation re-rating.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224167793173

- Hapag-Lloyd: Strategy 2030 announcement

- WorldCargo News: Global schedule reliability rises to 64% in November

- Hellenic Shipping News: Gemini raises schedule reliability despite congested ports

- Hapag-Lloyd: Statements and updates

- Freightender: 20 largest container shipping companies in 2025

- Finbox: Price / Book for Hapag-Lloyd AG

- Supply & Demand Chain Executive: Shipping rates to fall in 2026