DEEP RESEARCH · DRY BULK

Dry Bulk Shipping: The 2026 Cycle Built on Supply Constraint and Ton-Mile Growth

Investment implications of dry-bulk supply scarcity, Chinese demand, and environmental rules through SBLK and GOGL

0. Bottom line first

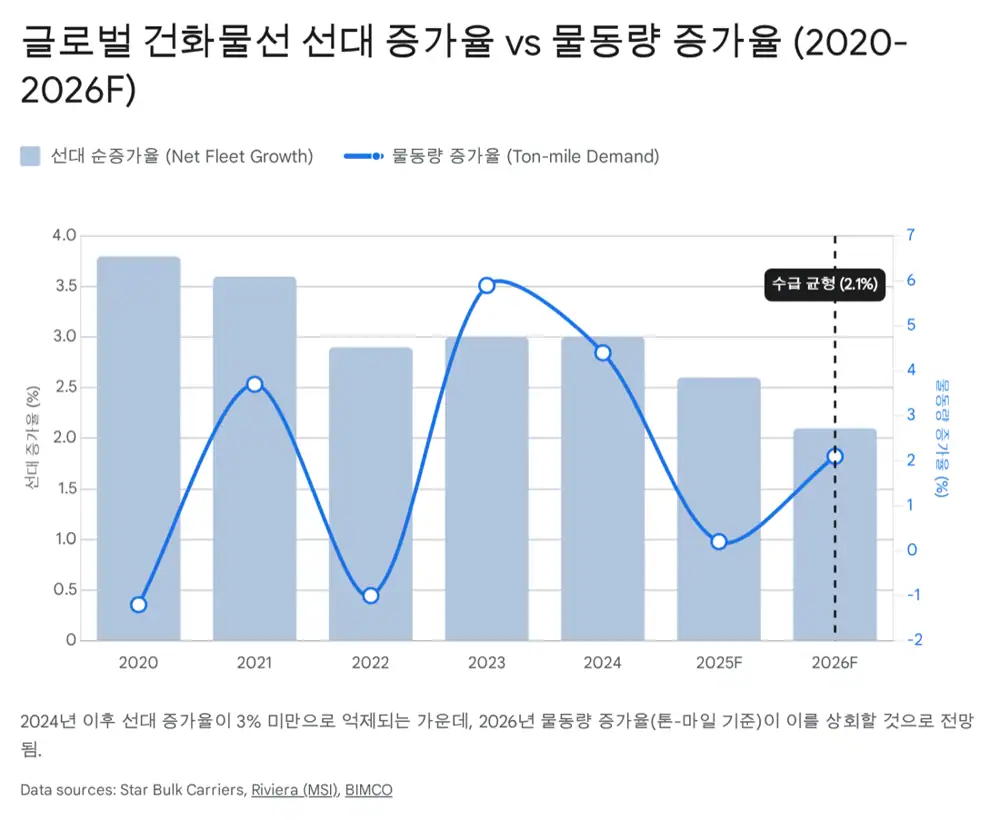

For 2026 dry bulk, supply constraint looks more important than a normal economic cycle. The orderbook is only about 10.9% of the fleet, yards are filled with LNG carriers and containerships through 2028, and ton-mile demand can expand through Simandou iron ore and longer diversion routes.

Official fact: The source says the BDI reached 2,148 points at the end of January 2026, up about 14.13% month on month and 192.24% year on year. The Capesize index reached 3,507 points, with TCE in the $24,000-$28,000 per day range.

Interpretation: BDI strength in the usual Q1 off-season suggests Red Sea/Panama Canal frictions and low effective supply are supporting rate floors. The larger investment point is the inelasticity of available tonnage.

1. Market Setup: “There Are No Ships”

The source puts supply scarcity at the center of the dry-bulk thesis. Newbuilding orders from January to November 2025 totaled 25 million DWT, down 54% year on year and the lowest since 2020. Yard slots are already filled by LNG carriers and large containerships, so dry-bulk ships ordered now may not arrive until after 2029.

Environmental rules also reduce effective supply. To maintain CII ratings, older vessels may need engine-power limits or slower speeds. A one-knot reduction in average speed can reduce effective capacity by about 4-5%. The source also says vessels older than 15 years account for about 30% of the fleet, increasing scrapping or retrofit decisions around 2026-2027 special surveys.

2. Demand: China Stimulus and Simandou Ton-Miles

On the demand side, China stimulus and a changing commodity map matter together. The source says China’s January 2026 reserve-requirement cut and fiscal spending expansion supported steel and energy demand, while iron-ore futures exceeded $109 per ton.

Official fact: The Simandou iron-ore project in Guinea is expected to begin initial shipments in 2026 and expand to 120 million tons per year by 2028. The Guinea-China route is about three times the Australia-China distance, creating much higher ton-mile demand for the same cargo volume.

Interpretation: Even if property-related steel demand is weaker than before, manufacturing-led plate demand from EVs, renewable infrastructure, and shipbuilding can still support large-vessel iron ore and bauxite demand.

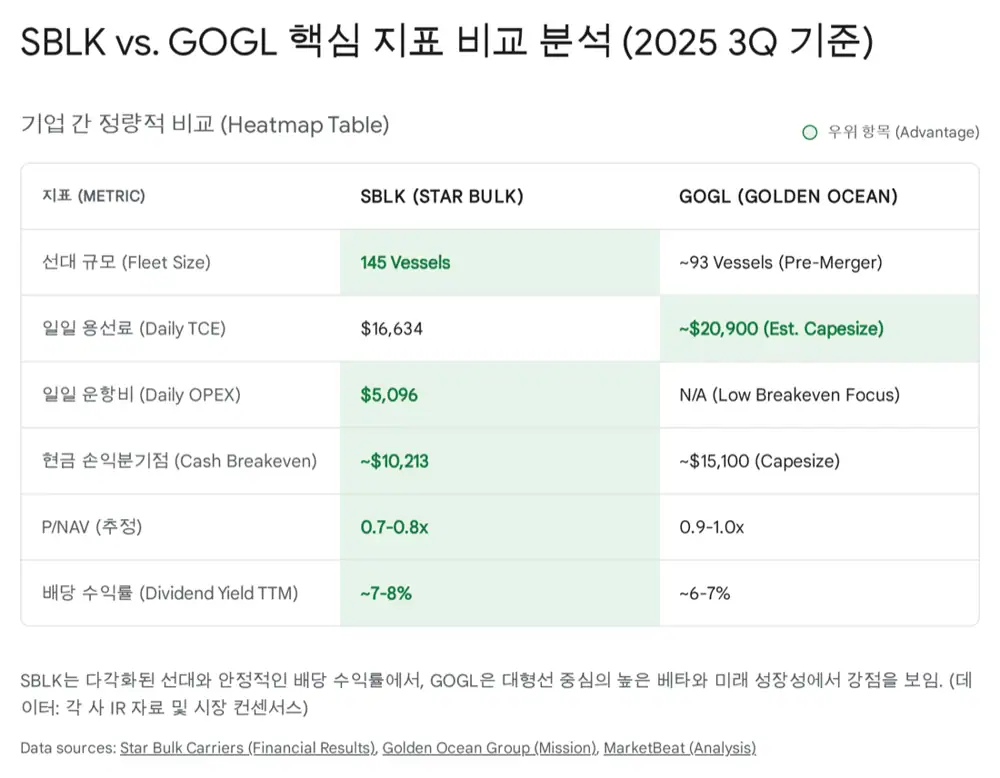

3. SBLK: Stability and Dividends

Star Bulk Carriers operates 145 vessels on a fully delivered basis, making it a major Nasdaq-listed dry-bulk carrier. Its fleet spans Newcastlemax to Supramax, giving it flexibility across iron ore, coal, grains, fertilizer, and other dry-bulk cargoes.

| Item | SBLK source figure | Interpretation |

|---|---|---|

| Scrubber coverage | About 94% | Creates extra cash flow if VLSFO-HSFO spreads hold at $100-$150/ton |

| 3Q25 average TCE | $16,634/day | Capesize/Newcastlemax reached $24,646/day |

| Daily OPEX | $5,096 | With net cash G&A of $1,325, cash cost was about $6,421/day |

| Cash | $454m | Total debt of $1.028bn and 15 debt-free vessels |

| 3Q25 dividend | $0.11/share | Cumulative dividends since 2021 reached $13.2/share |

After the 2024 Eagle Bulk Shipping merger, SBLK had already realized more than $40 million of synergy by Q1 2025. It also sold six older vessels for $75.5 million and used the proceeds to secure three efficient Kamsarmax newbuildings for 2026 delivery.

4. GOGL: Large-Vessel Beta and Green Technology

Golden Ocean Group, linked to John Fredriksen, has historically focused on large vessels such as Capesize and Panamax. The source views the August 2025 CMB.TECH merger as a structural shift because it adds ammonia/hydrogen co-combustion engine technology and next-generation green-vessel exposure.

Capesize exposure

GOGL is more sensitive to iron-ore volumes and China’s economic cycle, creating higher upside in rate rallies.

$23,600/day

Newcastlemax/Capesize performance exceeded market indices and was close to SBLK’s comparable figure.

$15,100/day

Low Capesize cash breakeven generated over $8,500/day per vessel at 3Q TCE levels.

5. Which Investor Fits Which Stock?

SBLK offers a discount at about 70-80% of NAV, a diversified fleet, scrubber-backed cash generation, and a clear dividend policy. GOGL trades around 90-100% of NAV, sometimes at a slight premium, with stronger green-fleet optionality and large-vessel beta.

- SBLK: Better suited to value and income investors who prioritize dividends and margin of safety.

- GOGL: Better suited to aggressive investors betting on China recovery and a Capesize freight-rate rally.

- Common risks: Prolonged Chinese property weakness, iron-ore demand slowdown, carbon-regulation costs, and high interest rates.

My practical approach would be to treat SBLK as the core holding candidate and add GOGL tactically when leading indicators such as China PMI, new lending, and port inventories turn clearly upward.