DEEP RESEARCH · BL Pharmtech

BL Pharmtech: Survival financials versus breakout pipelines

A combined review of 3Q 2025 performance, governance transition, Mr.Min exports, Gynepad, and molecular-glue momentum.

0. Bottom line first

BL Pharmtech is a company where financial survival must be checked first. Still, if restructuring under CEO Park Young-chul, Mr.Min ramen exports to Europe, Gynepad's FDA 510(k), and the molecular-glue platform all progress, a high-risk turnaround option remains.

3Q 2025 cumulative losses

Consolidated revenue was about KRW 5.7 billion, operating loss was KRW 1.68 billion, and net loss was KRW 2.96262 billion.

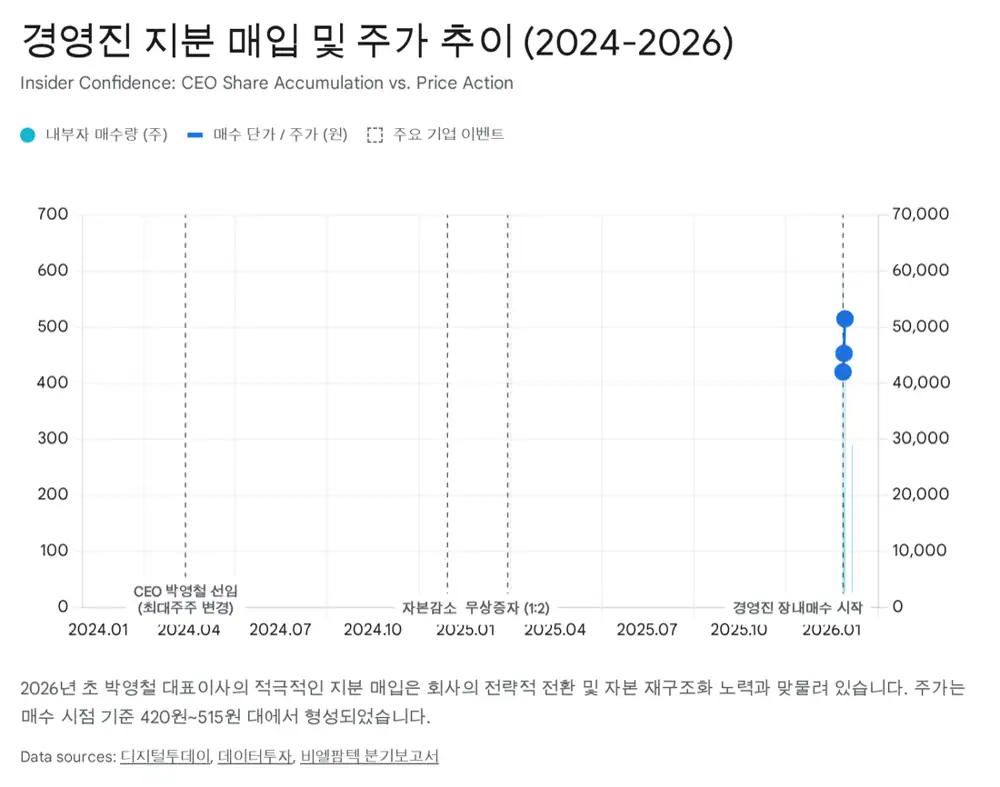

Ownership aligned with management

The largest shareholder changed to CEO Park Young-chul on March 28, 2024, and his stake expanded to 25.79% through market purchases in January 2026.

Food and biotech momentum

The KRW 3.02 billion Mr.Min supply contract, Gynepad's FDA clearance, and molecular-glue technology are the re-rating variables.

Official fact: Based on the 31st fiscal-year third-quarter report disclosed on November 14, 2025, cumulative consolidated revenue for 3Q 2025 was KRW 5.69526 billion, and cumulative operating loss was KRW 1.68145 billion.

Interpretation: I view this not as a stable earnings stock, but as a high-risk, high-return candidate that needs both financial normalization and new-business proof.

1. Governance Transition: Responsibility signal and defensive character

As of 3Q 2025, BL Pharmtech is trying to move beyond its former health-supplement distribution base and become a global food-distribution and advanced biotech company. The starting point is the governance transition that ran from 2024 into early 2026.

Official fact: On March 28, 2024, BL Pharmtech's largest shareholder changed from BL Corp. to current CEO Park Young-chul. From January 12 to 14, 2026, Park continued market purchases and increased his stake to 25.79%.

Interpretation: Management stake buying sends two signals: belief that the current price is below intrinsic value or growth potential, and a commitment to responsible management. However, because the purchases occurred when volatility and managed-issue concerns were rising, I also read them as defensive.

2. Consolidated Subsidiaries: A four-part strategic portfolio

BL Pharmtech is not only a health-supplement distributor. It has a holding-company-like structure spanning biotech, distribution, resource development, and materials. At the end of 3Q 2025, it had four consolidated subsidiaries.

| Subsidiary | Ownership | Business | Investment read |

|---|---|---|---|

| BL Science | 97.41% | In-vitro diagnostics, development and manufacturing of Gynepad HPV self-test kit | Core asset for biotech valuation |

| Next S&L | 100.00% | Wholesale and retail distribution of health supplements and cosmetics | Distribution channel that must become a cash cow |

| NRD MGL LLC | 100.00% | Mongolia-based resource development and services | Possible revaluation with critical-mineral supply-chain themes |

| BL Materials | 100.00% | Founded in May 2024 for eco-friendly materials and raw-material recycling | ESG-related new-business option |

Interpretation: The portfolio is broad, but the assets most likely to affect valuation are BL Science's Gynepad and the molecular-glue technology connected to BL Melanis. Next S&L must prove cash-flow recovery.

3. 3Q 2025 Financial Performance: Liquidity strain and capital impairment concern

The 3Q 2025 financial statements show the company's dilemma clearly: falling revenue, continuing operating losses, and liquidity pressure.

| Item | Figure | Meaning |

|---|---|---|

| Cumulative consolidated revenue | KRW 5.69526 billion | Declining year on year |

| Health-supplement revenue share | 79.3%, about KRW 4.5 billion | Still the dominant core business |

| General food and other | 20.7%, about KRW 1.19 billion | Early contribution from new food business |

| Cumulative operating loss | KRW 1.68145 billion | Fixed-cost burden and new-business expense |

| Cumulative net loss | KRW 2.96262 billion | Non-operating costs including financing costs |

| Current assets | About KRW 5.9 billion | Short-term liquid assets |

| Current liabilities | About KRW 9.8 billion | About KRW 3.9 billion more than current assets |

| Accumulated deficit | About KRW 87.4 billion | Pressuring total equity of about KRW 21.7 billion |

| Capital stock | About KRW 13.3 billion | Partial capital-impairment concern |

Official fact: The external auditor included uncertainty over the going-concern assumption in the audit-report notes. This means accounting-level doubt about whether normal operations can continue over the next 12 months.

The company executed a 10:1 no-consideration capital reduction at the end of 2024 and then adjusted its capital structure through measures such as transferring capital reserves into capital, effectively a bonus-issue-style accounting repair. These actions can be read as a difficult measure to cover accumulated deficits, lower the capital-impairment ratio, and meet KOSDAQ listing-maintenance requirements.

Interpretation: Capital reduction and capital repair can reduce accounting pressure, but they do not directly improve cash flow. The real question is whether operations can generate cash.

4. Operating Strategy: Mr.Min and upgrading health supplements

With growth in the legacy health-supplement business stalled, the company is seeking a breakthrough in global food distribution. Mr.Min ramen is at the center of that strategy.

Large European retailers

The source mentions listings at tier-one retailers such as Morrisons in the UK and E.Leclerc and Carrefour in France.

KRW 3.02 billion

Contrary to market rumors of KRW 30 billion, the disclosed and confirmed supply contract size is about KRW 3.02 billion.

12.3% of 2023 revenue

The KRW 3.02 billion supply contract equals about 12.3% of 2023 annual revenue.

Official fact: BL Pharmtech signed a supply contract with Anyone F&C for Mr.Min ramen products, including king-cup and yakisoba items, and the confirmed contract size is about KRW 3.02 billion.

Interpretation: Entry into European retailers is a positive signal on quality and distribution competitiveness. But until repeat orders are confirmed after the initial shipment, it is safer to discount it as potentially one-off revenue.

In health supplements, the company is pursuing a strategy to raise repeat-purchase rates through big-data analysis. The goal is to move beyond simple product sales and improve marketing efficiency and profitability through customized customer-data-based marketing. It is also trying to overcome domestic-market limits by exporting locally tailored products to markets such as China.

5. Biotech Pipeline: Gynepad and molecular glue

BL Pharmtech's current enterprise value depends more on biotech technology held by subsidiaries and affiliates than on current earnings. Gynepad and molecular glue are the key stock-price catalysts.

5.1 BL Science and Gynepad

Gynepad, developed by BL Science, is a self-diagnostic kit targeting HPV, the virus linked to cervical cancer. Conventional Pap smear testing can be invasive and uncomfortable because it requires a clinician-collected sample. Gynepad uses a sanitary-pad-like format to collect a sample non-invasively, improving convenience and privacy.

Official fact: Gynepad received U.S. FDA 510(k) medical-device clearance. The company plans U.S. market penetration through cooperation with telemedicine providers and is working with Sidley Austin to refine the market-entry strategy.

5.2 BL Melanis and molecular glue

Affiliate BL Melanis is described as holding a molecular-glue platform. Molecular glue is a form of targeted protein degradation, or TPD, that does not merely inhibit disease-causing proteins but removes them using the body's protein-degradation systems, such as E3 ligases.

This approach is innovative because it can target so-called undruggable proteins that are hard to address with conventional small molecules. Globally, Monte Rosa Therapeutics, NASDAQ: GLUE, is cited as a leader in this field.

Interpretation: If a trillion-won-scale technology-export agreement is signed, the company could re-rate sharply. But investing only on news that talks are underway is risky given biotech-sector volatility. Until contract execution and upfront-payment terms are visible, I treat it as option value.

6. Key Risks: Managed issue, CB overhang, business uncertainty

| Risk | Source basis | Indicator to check |

|---|---|---|

| Managed-issue designation | Four consecutive fiscal years of operating losses can lead to managed-issue designation; five can lead to delisting substantive review | Whether 4Q 2025 turns profitable |

| Convertible-bond overhang | Outstanding balances remain for the 19th, 20th, and 21st CBs | Conversion price, refixing, actual conversion volume |

| 21st CB terms | Coupon rate set at 0% | Whether investors are targeting conversion gains rather than interest income |

| Food-export persistence | Repeat orders after initial Mr.Min shipments are not yet confirmed | European sell-through and reorders |

| Biotech license-out | L/O talks can be delayed or fail | Signed contract, upfront payment, milestones |

Interpretation: Recent moves by financial authorities to ease delisting requirements may be a variable, but they remain uncertain. Conservatively, operating-profit turnaround and liquidity stabilization need to be confirmed first.

7. 2026 Scenarios and Conclusion

2026 could determine BL Pharmtech's survival path. I divide the outlook into three scenarios.

Large license-out plus food-market traction

If molecular-glue technology is licensed to global big pharma and Mr.Min becomes a steady seller in Europe, the balance sheet can improve quickly.

Gradual Gynepad sales and stable exports

U.S. sales and ramen exports continue modestly, but profitability takes time and additional funding may be required.

Failed talks and one-off exports

If technology-transfer talks fail or are delayed and ramen exports are one-off, liquidity stress and restructuring pressure can intensify.

In conclusion, BL Pharmtech is a classic high-risk, high-return company. The 3Q 2025 financial numbers are harsh, but the biotech pipeline and management share purchases preserve the possibility of a reversal. My key KPIs are whether the molecular-glue technology-transfer contract is signed, real sell-through of Mr.Min ramen in Europe, and whether 4Q 2025 operating profit can turn positive.

Interpretation: This is a period where verification matters more than expectation. By the first half of 2026, it should become clearer whether the restructuring tunnel ends in a breakout or in additional risk.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224167209503

- DigitalToday: https://www.digitaltoday.co.kr/news/articleView.html?idxno=621073

- Data Tooza: https://www.datatooza.com/article/2026012117305226952ef34ca12_80

- MedicoPharma: https://www.medicopharma.co.kr/news/articleView.html?idxno=62917

- Korea Economic Daily on Leclerc MOU: https://www.hankyung.com/article/2025031935116

- Korea Economic Daily contract disclosure: https://www.hankyung.com/article/202503129200L

- Mobile Hankyung contract disclosure: https://plus.hankyung.com/apps/newsinside.view?aid=202503129200L&category=&sns=y

- Yakup: http://m.yakup.com/news/index.html?mode=view&nid=280271

- Hit News: http://www.hitnews.co.kr/news/articleViewAmp.html?idxno=44635

- Daum: https://v.daum.net/v/20260116183244518

- Macrotrends: https://www.macrotrends.net/stocks/charts/GLUE/monte-rosa-therapeutics/market-cap

- Edaily Pharm: https://pharm.edaily.co.kr/news/read?newsId=02371446645318048

- KRX investment caution designation: https://kind.krx.co.kr/external/2025/03/21/001764/20250321006576/70736.htm

- Kiwoom disclosure: https://invest.kiwoom.com/inv/disclosure_detail?date=2025.03.21&seq=00027738&type=02&code=02&keyword=%EB%B9%84%EC%97%98%ED%8C%9C%ED%85%8D&stockCode=&tp=

- KRX convertible-bond issuance decision: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20230622000531&rcpno=20230622000508&orgid=F&tran=Y&langTpCd=0