DEEP RESEARCH · SAMSUNG SDI / SK ON SCENARIO

Samsung SDI and the SK On Acquisition Hypothesis: Near-Zero Equity, Debt Sharing, and SDC Stake Monetization

A battery restructuring rumor examined through financial capacity, deal structure, government involvement, and integration risk

0. Bottom line first

I see selective acquisition of SK On's best assets, such as the Georgia plant, specific JV stakes, or customer contracts, as more realistic than a full absorption merger. “Free acquisition” means equity value may approach zero after debt, not that the debt burden disappears.

Debt ratio 190%+

The source ties SK On's standalone risk to debt and yield issues.

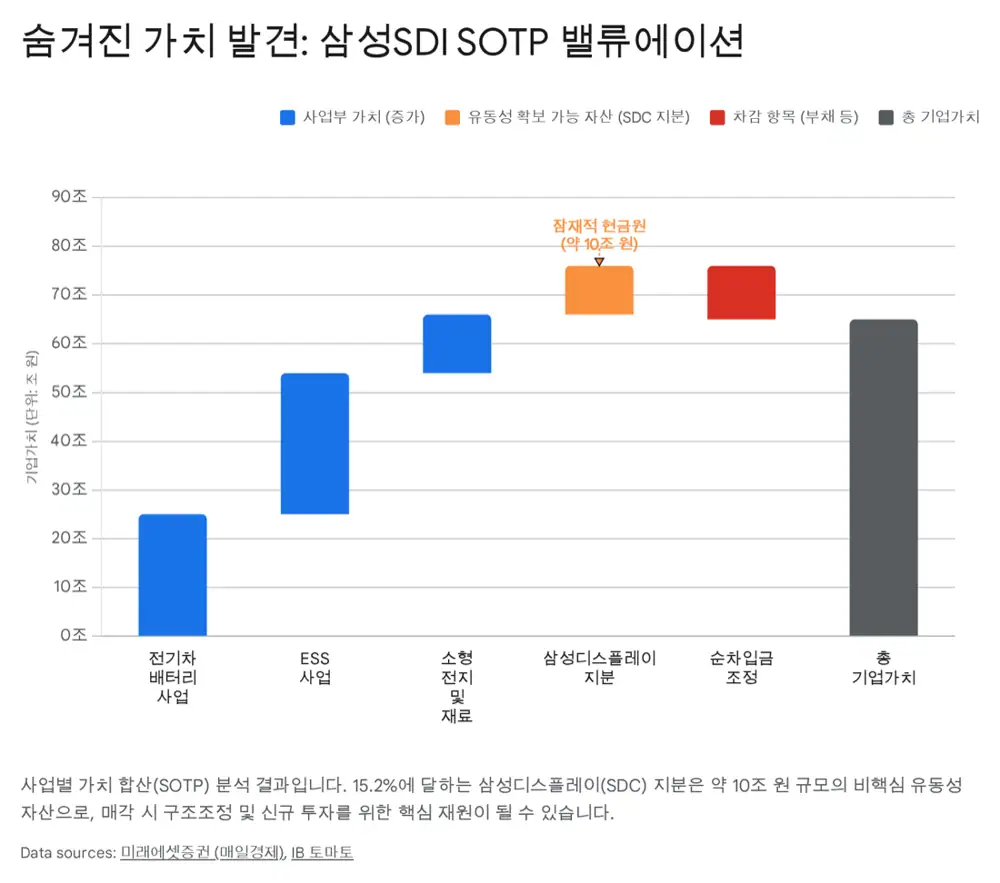

15.2% SDC stake

The Samsung Display stake is described as a card recently revalued at about KRW 10 trillion.

Selective assets

Buying only high-quality assets or stakes lowers risk versus a full merger.

Official fact: The source states that it was written using market information and financial data as of February 1, 2026. It is a scenario analysis prompted by battery-industry restructuring rumors from a government meeting.

Interpretation: This is not a confirmed transaction; it is hypothesis testing. The key question is less “Can Samsung SDI buy SK On?” and more “Which assets and liabilities would Samsung SDI accept in a structure shareholders can tolerate?”

1. Industry background: EV chasm and restructuring pressure

The source frames the EV demand slowdown that began in late 2024, CATL and BYD's LFP cost pressure, and IRA subsidy uncertainty as exposing structural weakness among Korean battery makers. LG Energy Solution, Samsung SDI, and SK On expanded aggressively under the “second semiconductor” narrative, but liquidity and profitability pressures are now rising together.

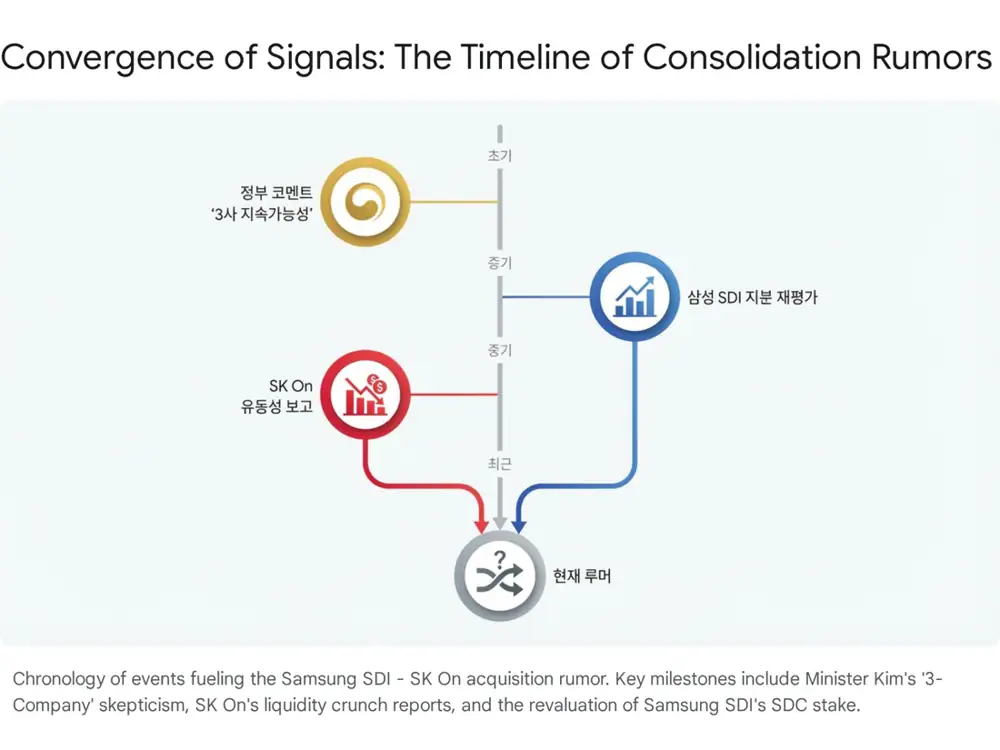

The rumor has three axes. First is the valuation paradox that SK On equity could be transferred for almost nothing. Second is a restructuring mechanism in which debt is shared between the government and Samsung SDI. Third is a funding strategy in which Samsung SDI monetizes its Samsung Display stake.

2. The asset for sale: SK On's liquidity trap

After being spun off from SK Innovation, SK On simultaneously built plants in Georgia, Ivancsa, Yancheng, and other locations, creating heavy CAPEX. High rates and the EV chasm raised interest and utilization pressure; the source treats this as the origin of the sale rumor.

| Item | Samsung SDI | SK On | Comment |

|---|---|---|---|

| Net debt | About KRW 11.0T, excluding SDC stake | About KRW 25.5T+ | SK On leverage is far larger |

| Debt ratio | About 65-70% | 190%+ | Clear financial-safety gap |

| Cash-like assets | About KRW 2.35T + KRW 10T SDC stake | About KRW 1.5T | Samsung SDI has monetizable assets |

| Credit rating | AA, stable | A+, under negative review | SK On faces continued downgrade pressure |

Interpretation: Even large facilities and operating value can leave equity worth near zero if net debt is larger. “Free acquisition” means gaining control in exchange for taking on liabilities.

The operating issue is yield. The source contrasts Samsung SDI's process-stabilization-first approach at God, Hungary, with SK On expanding capacity first on the strength of its order book. Early yield issues in Georgia and Hungary created cost losses. The IPO plan was delayed by ongoing losses and EV slowdown, and the SK E&S merger is described as a temporary patch rather than a fundamental fix.

3. Samsung SDI's funding card: 15.2% Samsung Display stake

Samsung SDI's 15.2% stake in Samsung Display is the strongest financial basis for this scenario. The source says the stake was historically carried around KRW 3.5 trillion but has recently been revalued by analysts at about KRW 10 trillion.

The logic is that Samsung Display has strong cash generation from OLED panels for Apple iPhones and iPads, while Samsung SDI's share price gives little credit because of private-company discount and double-counting concerns. A sale to Samsung Electronics or a block deal could quickly create major liquidity.

4. Strategic synergy: complementary formats and customers

Samsung SDI is strong in prismatic and cylindrical cells, with customers such as BMW, Audi, Rivian, GM, and Stellantis. SK On specializes in pouch cells and has Ford, Hyundai, Kia, and Volkswagen relationships. The source's synergy argument is that a deal could create a total battery solution supplier across all form factors.

| Company | Main production sites | Main form factor | Major customers | Note |

|---|---|---|---|---|

| Samsung SDI | Hungary God, China Xian/Tianjin, Malaysia, U.S. Indiana | Prismatic Gen 5/6, cylindrical 46-series | BMW, Audi, Rivian, GM, Stellantis | Later to North America but expanding with profitability discipline |

| SK On | Korea Seosan, U.S. Georgia/Kentucky/Tennessee, Hungary Komarom/Ivancsa, China Changzhou/Yancheng | Pouch | Ford, Hyundai, Kia, Volkswagen | Strong North American footprint but yield and utilization issues continue |

| Synergy | Southern and central U.S. complementarity | Prismatic, cylindrical, and pouch lineup | Diversified customer portfolio | Integration cost due to process differences |

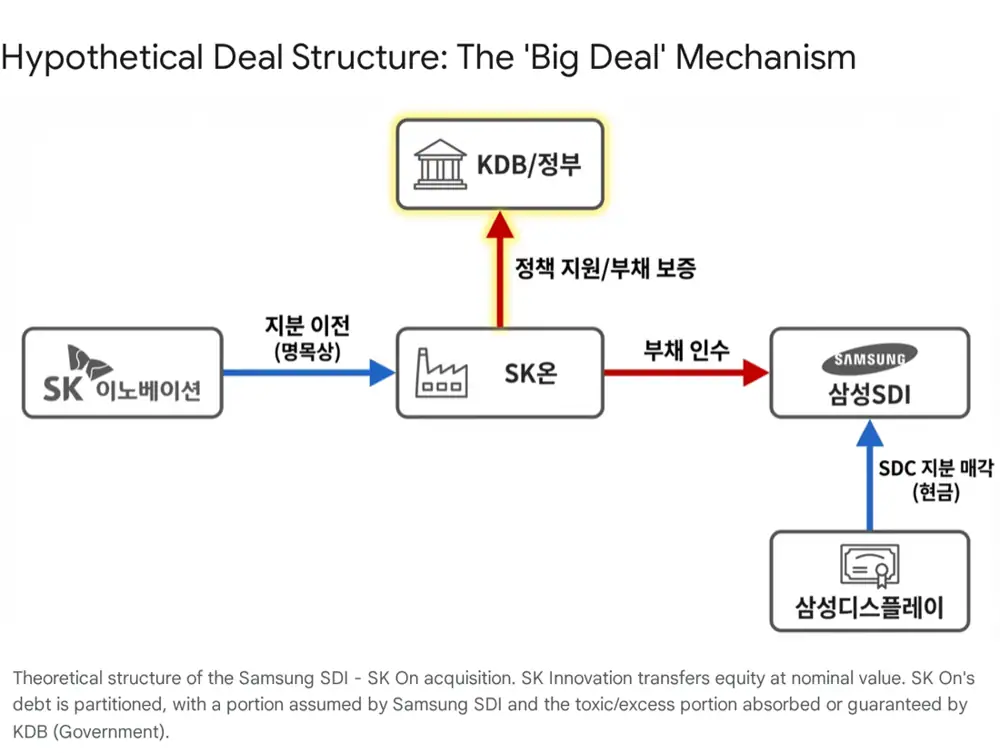

5. Deal structure: near-free equity and debt split

The source compares the “free acquisition and debt split” idea to distressed-company restructuring such as P&A or workout. The market's “free” does not literally mean zero; it means a symbolic amount, such as KRW 1,000.

- Seller benefit: SK can escape more than KRW 20 trillion of debt, annual trillion-won losses, and future CAPEX burden, allowing SK Innovation to focus on energy and defend its credit rating.

- Buyer benefit: Samsung gains existing plants, trained workers, and backlog, but the deal depends on how much debt is forgiven or deferred.

- Liability separation: Strong assets such as U.S. plants and Hyundai contracts could be split from weak early plants and bad liabilities through a good-bank/bad-bank structure.

- Policy finance: KDB and other creditors could convert debt to equity, reduce interest, or refinance residual debt with long-term low-rate loans.

Comparable cases include the 2020 KDB-led Korean Air-Asiana transaction and the late-1990s semiconductor big deal. The common point is government steering to preserve national strategic-industry competitiveness; the difference is that this battery scenario is focused more on industry competitiveness and distressed-asset cleanup than on a control dispute.

6. Government and KDB: why now?

The source reads Minister Kim Jung-kwan's comments on the “three battery makers” structure as a sign of changing government thinking. Having three companies fight over the same narrow talent pool and underbid each other overseas may be seen as a national inefficiency.

CATL has more than 30% global share as a single company and therefore major cost advantage. From the government's perspective, combining a weak No. 3 with the No. 2 could look rational. The source says KDB's 2025 restructuring support program can include tax benefits, simplified merger review, dedicated funds, and loan support.

7. Reality check: hidden risks

Technology and culture risk

Samsung SDI centers on prismatic cells, while SK On centers on pouch. Equipment and material ecosystems differ, and the source says Samsung has internal skepticism about pouch safety. Culture can also clash between Samsung's controlled operating style and SK's more aggressive and flexible culture.

Antitrust and international approval

Approval would be needed not only from Korea's Fair Trade Commission, but also from U.S., EU, and Chinese regulators. The source does not rule out China resisting the creation of a large Korean battery player.

Samsung SDI shareholder opposition

Samsung SDI has traditionally kept a conservative financial stance, and CEO Choi Yoon-ho has been cautious about unprofitable scale expansion. Taking on SK On's liabilities could raise shareholder concerns, and Samsung Electronics may not welcome SDC sale proceeds being used for a distressed acquisition.

8. Scenario probabilities

| Scenario | Source view | My condition to watch |

|---|---|---|

| “Free” SK On acquisition | High feasibility | The key is not zero equity price but what liabilities are assumed |

| Government/Samsung debt sharing | Medium feasibility | Requires industrial-policy justification, subsidy-politics management, and KDB terms |

| Samsung Display stake sale | Very high feasibility | Can be used as funding regardless of SK On |

| Selective asset acquisition | Most realistic | Focused on Georgia, specific JVs, customer contracts, and other high-quality assets |

The events to watch are Samsung SDI's SDC stake-sale disclosure, KDB battery support measures, SK On's additional liquidity actions, and utilization/yield improvement at North American plants. If those move together, the rumor can become an actual transaction structure.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224167182000

- 시사저널e: SK온 부채비율 190%: https://www.sisajournal-e.com/news/articleView.html?idxno=401677

- 연합인포맥스: SK온과 SK이노베이션 신용도: https://news.einfomax.co.kr/news/articleView.html?idxno=4354945

- SK Innovation IR: 재무 하이라이트: https://www.skinnovation.com/ir/financial_statement

- Samsung SDI 2024 3Q IR PDF: https://www.samsungsdi.com/upload/download/ir/2024.3Q_IR_Final_E.pdf

- POLITICO Pro: SK Innovation rating cut: https://subscriber.politicopro.com/article/eenews/2024/03/20/sk-innovation-cut-to-junk-by-s-p-on-battery-demand-slowdown-00147839

- 매일경제: SDC 지분 매각 가정: https://www.mk.co.kr/news/stock/11937568

- YouTube: Samsung SDI chasm discussion: https://www.youtube.com/watch?v=cqq29rndiz4

- 더게이트: 배터리 3사 체제 발언: http://www.spochoo.com/news/articleView.html?idxno=118769

- TheVC: 2025년 사업재편 지원사업 1차 PDF: https://grant-documents.thevc.kr/246872_(%EB%B6%99%EC%9E%841)+2025%EB%85%84+%EC%82%AC%EC%97%85%EC%9E%AC%ED%8E%B8+%EC%A7%80%EC%9B%90%EC%82%AC%EC%97%85+%EA%B8%B0%EC%97%85%EB%AA%A8%EC%A7%91+%EA%B3%B5%EA%B3%A0(1%EC%B0%A8).pdf

- Starrich: 2025년 사업재편 지원사업 2차 PDF: https://image.starrich.co.kr/integration/ceo_files/(%EB%B6%99%EC%9E%841)%202025%EB%85%84%20%EC%82%AC%EC%97%85%EC%9E%AC%ED%8E%B8%20%EC%A7%80%EC%9B%90%EC%82%AC%EC%97%85%20%EA%B8%B0%EC%97%85%EB%AA%A8%EC%A7%91%20%EA%B3%B5%EA%B3%A0(2%EC%B0%A8)_1052.pdf

- Stockplus: 공정위 삼성SDI 현장조사: https://news.stockplus.com/m?news_id=15248455