DEEP RESEARCH · TOSS/VIVA REPUBLICA

Toss: The 2025 Monetization Inflection and 2026 U.S. IPO Strategy

A review of super-app monetization, Toss Securities/Bank, insurance-GA disruption, KakaoPay comparison, and the U.S. listing pivot.

0. Bottom line first

My read is that Toss in 2025 shifted from a growth-at-a-loss fintech into a profitable fintech where operating leverage is working. After the first annual profit in 2024, revenue and earnings accelerated together in H1 2025, forming the basis for the U.S. IPO strategy.

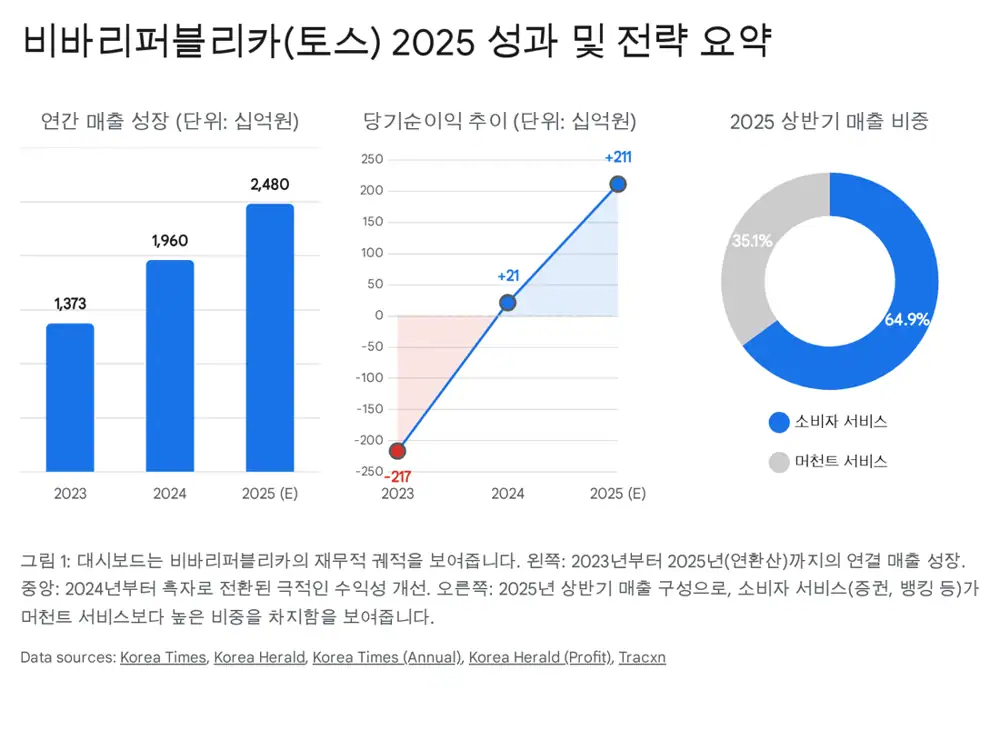

Official fact: The source states that 2024 consolidated revenue was KRW 1.956T, up 42.7% YoY, with operating profit of KRW 90.7B and net income of KRW 21.3B, marking Toss' first annual profit. In H1 2025, consolidated revenue exceeded KRW 1.2T, up 35.2% YoY, with operating profit of KRW 154.6B and net income of KRW 105.7B.

Interpretation: The funnel that gathers traffic through free transfers and converts it into loans, securities, insurance, tax services, and advertising appears to have crossed critical mass. Toss Securities and Toss Bank prove that numerically, while Toss Insurance shows how data can reshape the traditional GA market.

1. Fintech industry backdrop and Toss' position

The source divides Korean fintech into a mid-2010s traffic-acquisition phase through simple transfers and payments, an early-2020s unbundling/rebundling phase, and a 2025 monetization completion phase. Toss expanded captured traffic into lending, deposits, investment, and insurance brokerage, encroaching on traditional financial institutions' core areas.

Official fact: The source says financial regulatory sandbox programs and MyData activation created a legal foundation for platforms such as Toss to recommend and sell hyper-personalized financial products using data. At the same time, regulatory risk remains through discussions such as the Online Platform Regulation Act.

Interpretation: The move from a domestic IPO to a U.S. listing reflects domestic-market limits, platform-regulation risk, and Korea-discount avoidance. It is not just a change in listing venue; it is a choice to redefine the company as a global fintech.

2. Financial performance: operating leverage realized

| Item | Source figure | Meaning |

|---|---|---|

| 2024 revenue | KRW 1.956T, +42.7% YoY | Record revenue |

| 2024 operating profit | KRW 90.7B | First annual profit after operating losses above KRW 200B through 2023 |

| 2024 net income | KRW 21.3B | Entry into profitable structure |

| H1 2025 revenue | Above KRW 1.2T, +35.2% YoY | Growth continued |

| H1 2025 profit | Operating profit KRW 154.6B, net income KRW 105.7B | About five times 2024 full-year net income in one half |

| Q2 2025 | Revenue KRW 668.0B (+41% YoY), net income KRW 57.0B | Revenue growth outpaced cost growth |

The source explains this as operating leverage. Toss appears to have moved beyond the fixed-cost burden of initial platform building and user acquisition into a zone where incremental users carry low marginal cost.

Consumer vs. merchant

| Segment | H1 2025 revenue | Share | Composition |

|---|---|---|---|

| Consumer services | KRW 802.1B | 64.9% | Transfers, loan brokerage, stock trading, ads, Toss Income, identity verification |

| Merchant services | KRW 433.3B | 35.1% | Toss Payments PG, Toss Place offline terminals and solutions |

Interpretation: The consumer segment monetizes through higher-margin financial products, while merchant services lock enterprise customers into the payment network and create a bridge to B2B loans and business financial products.

3. Core subsidiaries: Toss Securities and Toss Bank

Overseas-stock brokerage engine

H1 2025 operating profit was KRW 168.9B, up 452% YoY. Operating revenue was KRW 354.0B, double YoY, and net income of KRW 131.4B nearly matched 2024 full-year net income of KRW 131.5B.

Stabilized internet bank

Q3 2025 cumulative net income was KRW 81.4B, up 136% YoY. Non-interest income rose 52% to KRW 129.6B, and NIM improved to 2.56% from 2.49% a year earlier.

Toss Payments and Toss Place

PG transaction growth, offline terminal rollout, and technologies such as FacePay extend app payment UX into offline commerce.

Official fact: The source says Toss Securities' overseas stock trading value rose 211% YoY by the end of 2024. Mobile-first overseas trading, real-time fractional trading, and daytime trading services attracted Korean retail investors without a complex HTS experience.

4. Competitive landscape: Toss vs. KakaoPay

| Item | Viva Republica/Toss | KakaoPay | Implication |

|---|---|---|---|

| 2024 revenue | KRW 1.956T | KRW 766.2B | Toss revenue was about 2.5x KakaoPay's |

| H1 2025 revenue | KRW 1.24T | About KRW 470.0B estimated | Gap widened |

| 2024 profitability | Net income KRW 21.3B | Net loss KRW 21.5B | Toss entered profit; KakaoPay remained loss-making |

| Core driver | Securities, banking | Payment TPV, loan brokerage | Toss is stronger in manufacturing/selling financial products |

| User base | App MAU about 19M | Subscribers about 25M | KakaoPay has reach; Toss has deeper financial activity per user |

Interpretation: KakaoPay has huge KakaoTalk traffic, but its revenue mix remains more payment-fee heavy and KakaoBank is a separately listed entity, limiting banking/securities/payment integration. Toss lowers CAC and raises LTV by combining banking, securities, insurance, and payments in one app.

5. Insurance GA disruption: data-driven push model

The source sees insurance GA as the battlefield where Toss most clearly disrupts with data. The market is shifting from labor-centered selling to a hybrid model combining technology and human advisors.

Official fact: Toss Insurance's face-to-face agent organization grew from 2 people in 2022 to about 2,300 by February 2025. H1 2024 revenue grew 3.3x YoY to KRW 52.5B, and the company recorded its first half-year profit of KRW 350M. Per-agent productivity was about KRW 760,000 per month in H1 2024, according to the source.

| Comparison | Toss Insurance | Hanwha Life FS | Kakao Pay Insurance |

|---|---|---|---|

| Core model | Data-driven push | Large human network | Digital pull |

| Sales method | App data analysis → free leads → agent matching | Acquaintance selling, prospecting, purchased DBs | User-initiated purchase |

| Agent count | About 2,300 (2025.02) | More than about 30,000 (2024) | None, digital direct sales |

| Main products | Long-term protection insurance such as cancer and health | Life insurance and third-sector insurance overall | Mini insurance for travel, mobile phones, golf, and others |

| Performance | Turned profitable | Contributed KRW 866.0B consolidated net income | Revenue up 377%, driven by overseas travel insurance |

Interpretation: Toss' edge is giving agents free warm leads from app actions such as insurance-coverage analysis and medical-expense reimbursement, instead of cold-call lists. Lower customer-discovery cost lets agents focus on consultation and closing, which shows up as productivity.

6. IPO strategy: from KOSPI to the U.S.

The source says Viva Republica's IPO strategy pivoted sharply from a domestic KOSPI listing to a U.S. Nasdaq or NYSE listing from late 2024.

- In February 2024, Toss selected Korea Investment & Securities and Mirae Asset Securities as domestic IPO underwriters.

- In 2H 2024, it told the underwriting group to stop the listing work.

- The source says domestic platform sentiment had frozen after KakaoBank and KakaoPay shares fell 70-80% from their highs. The Korean market wanted PBR of around 2-3x, while Toss wanted a higher growth multiple.

- Toss targets a U.S. valuation from at least KRW 10T, about USD 7.2B, to as much as KRW 20T, about USD 14.4B. Its 2022 pre-IPO valuation was about KRW 8T.

- The expected schedule is U.S. underwriter selection by the end of 2025 and a Q2 2026 listing target.

- Preparation items include establishment of Toss Securities Americas, an ESG-dedicated team, and internal-control system improvements.

U.S. listing risks

- Higher compliance cost under U.S. listing rules such as SOX.

- Frequent shareholder-litigation risk in U.S. equity markets.

- Low awareness among Wall Street investors, who may still view Toss as an unfamiliar Asian fintech.

7. Final view

Interpretation: My conclusion is that Toss is a rare fintech case where the strategy of bundling banking, securities, payments, and insurance into one app has been verified in profits. The data-driven insurance GA model removed traditional-industry inefficiency, while Toss Securities and Toss Bank showed super-app profitability in numbers.

The remaining question is whether Toss can sell this model convincingly to global investors in the 2026 U.S. IPO process. Sustained Toss Securities earnings growth, Toss Insurance agent expansion speed, and regulatory readiness for the U.S. listing are the key monitoring indicators.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224166557521

- The Korea Times: https://www.koreatimes.co.kr/business/banking-finance/20250814/toss-posts-35-revenue-growth-in-first-half-of-2025

- The Korea Herald: https://www.koreaherald.com/article/10554500

- KakaoPay Earnings Release PDF: https://t1.kakaocdn.net/pay_brand_admin/file/VPAedkjsvZE0cz8Klhgzm/kakaopay_4Q24_Earnings_Release_Eng__F.pdf

- IPOX Update: https://www.ipox.com/ipox/the-ipox-update-07252025

- KED Global: https://www.kedglobal.com/ipos/newsView/ked202410290017

- MDPI: https://www.mdpi.com/2076-3387/15/1/25

- ProMarket: https://www.promarket.org/2025/09/02/the-future-of-the-online-platform-regulation-act-in-south-korea/

- The Korea Times: https://www.koreatimes.co.kr/business/banking-finance/20250328/toss-posts-first-ever-annual-profit-in-2024

- The Korea Herald: https://www.koreaherald.com/article/10453004

- PR Newswire: https://www.prnewswire.com/news-releases/toss-surpasses-krw-668-billion-in-consolidated-revenue-for-q2-2025-achieving-41-year-over-year-growth-302530252.html

- Toss Feed: https://toss.im/tossfeed/article/2025-2Q-growth

- The Korea Herald: https://www.koreaherald.com/article/10554501

- The Korea Herald: https://www.koreaherald.com/article/3835690

- KoreaTechDesk: https://koreatechdesk.com/toss-bank-achieves-first-ever-profit-in-2024-paving-the-way-for-global-expansion

- The Korea Herald: https://www.koreaherald.com/article/10420313

- GL Insight: https://www.glinsight.com/toss-bank-posts-record-earnings-in-q3-gl-insight/

- CHOSUNBIZ: https://biz.chosun.com/en/en-finance/2025/07/03/GD5CZWN3DJDVHNLPWMUIZANCAE/

- Alpha Spread: https://www.alphaspread.com/security/krx/377300/investor-relations/earnings-call/q2-2025

- CHOSUNBIZ: https://biz.chosun.com/en/en-finance/2025/02/12/LFVKQYA5IFDVHDC5TCSBABLSYA/

- Asia Economy: https://cm.asiae.co.kr/en/article/2024092609012020609

- Hanwha Life Financial Services: https://www.hanwha.com/companies/hanwha-life-financial-services.do

- Qorus: https://www.qorusglobal.com/content/29036-user-centric-innovation-drives-kakaopay-insurances-market-leadership

- THE INVESTOR: https://www.theinvestor.co.kr/article/3317622

- Korea JoongAng Daily: https://koreajoongangdaily.joins.com/news/2024-10-30/business/finance/Viva-Republica-considers-tossing-local-IPO-in-favor-of-US-listing/2166993

- Connecting the Dots in FinTech: https://www.connectingthedotsinfin.tech/viva-republica-prepares-esg-ahead-of-u-s-listing/