DEEP RESEARCH · HYOSUNG TNC

Hyosung TNC: The End of the Spandex Chicken Game and a 2026 Supplier-Led Cycle

Why Zhuji Huahai’s distress and the capex cliff matter more than weak Q4 earnings

0. Bottom line first

My focus is not the expected Q4 2025 earnings dip, but the 2026 shift in spandex supply and demand. New capacity is expected to fall to roughly 30,000 tons, demand may rise by 80,000-110,000 tons, and the bankruptcy risk at China’s No. 3 producer Zhuji Huahai reads as a signal of supply removal and recovering pricing power.

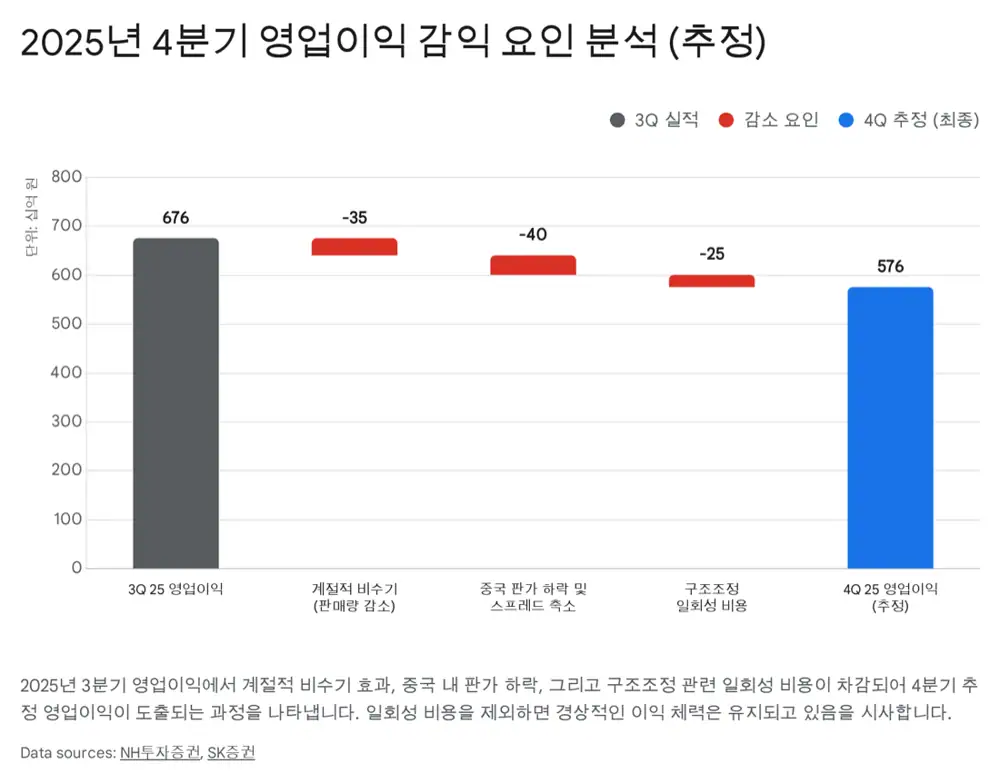

Official fact: The source frames Q4 2025 revenue at about KRW 1.8-1.9 trillion and operating profit at KRW 55-58 billion, down roughly 14-17% quarter on quarter. Year on year, it still implies about 90-100% growth from a low base.

Interpretation: The quarter-on-quarter drop looks driven by seasonality, Chinese dumping pressure, and restructuring charges for old Chinese facilities. I read it less as fundamental damage and more as pre-2026 cost cleanup.

1. Q4 Earnings: A Bottoming Quarter and Cost Cleanup

Q4 is normally a textile and apparel off-season. Global brands and retailers build inventory in Q2-Q3 for Black Friday and Christmas, then focus on destocking in Q4. In late 2025, tighter inventory control amid macro concerns amplified this seasonal softness.

Official fact: The source says Hyosung TNC recovered KRW 138 billion of a deposit previously paid for Hyosung Chemical’s specialty gas business and completed cleanup actions such as liquidating the loss-making Hyosung Singapore entity.

Interpretation: The KRW 138 billion cash inflow improves liquidity in a high-rate environment. Restructuring charges for older Chinese assets hurt near-term income, but they look like a big-bath move to improve margins from 2026 onward.

2. Zhuji Huahai: A Signal That the Chicken Game Is Ending

The strongest trigger is bankruptcy risk at Zhuji Huahai, China’s No. 3 spandex producer. The source says Huahai has about 225,000 tons of annual spandex capacity, or about 15.6% of China’s total. It also tried to vertically integrate into BDO and PTMEG with roughly KRW 2 trillion of investment in 2023, but heavy leverage collided with a weak cycle.

30-50%

The source says Huahai’s utilization has fallen sharply and could fully stop as bankruptcy or rehabilitation procedures advance.

RMB 1.3bn

A December court enforcement action of RMB 1.3 billion, roughly KRW 275 billion, reportedly cut off funding.

6-15% of China capa

Full exit could remove about 15% of Chinese capacity; even rehabilitation may permanently remove more than 6% through restructuring.

Interpretation: This is not just one competitor’s failure. It suggests years of below-cost competition have reached a breaking point. Once distressed producers stop dumping, the No. 1 producer’s pricing power should recover.

3. Price Hikes and 2026 Earnings Leverage

The source says major Chinese producers, including Huafon Chemical, notified customers of a RMB 1,000 per ton spandex price increase around January 20, 2026. A January price hike during the usual off-season is meaningful because it implies a shift from buyer power to seller power.

| Variable | Source figure | Meaning |

|---|---|---|

| 2026 new capacity | About 30,000 tons | More than 80% lower year on year, about 2% of global capacity |

| 2026 demand growth | About 80,000-110,000 tons | Expected growth of 6-8% year on year |

| Hyosung TNC utilization | Above 90% expected | Lower fixed-cost burden and operating leverage |

| Price sensitivity | RMB 1,000/ton increase may lift annual OP by over KRW 45bn | High earnings sensitivity to pricing |

| NH 2026 OP forecast | KRW 326.9bn, up 23.7% YoY | Base case for supply improvement flowing into profit |

4. Hyosung TNC’s Differentiation

The key advantage is a diversified global production footprint. The source says Hyosung TNC has about 20% share in China but 70-80% share outside China. Vietnam, India, Turkey, and Brazil reduce the shock from Chinese oversupply and help navigate trade barriers in the U.S. and Europe.

Eco-friendly materials are another option. Bio-based spandex and recycled nylon made from discarded fishing nets under the Regen product family target ESG demand from high-end brands in Europe and North America. NF3 specialty gas for semiconductor and display processes is presented as a cash generator that can partially offset textile cyclicality.

5. Risks and My View

- If Zhuji Huahai’s restructuring is slower than expected or capacity returns to market, the supply-removal effect weakens.

- If BDO and PTMEG costs rebound, price increases may not fully translate into wider spreads.

- If apparel brand destocking lasts longer, the 2026 demand-growth assumption could be too optimistic.

Even with those risks, I see the current phase as the beginning of a structural upcycle after the worst oversupply. The key monitoring points are Q1 2026 price increases, spreads, and competitor utilization rather than one weak Q4 print.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224166534321

- Buffett Lab: Hyosung TNC 2026 spandex additions decline

- Pinpoint News: Hyosung TNC Q4 earnings weakness

- Biztribune/SK Securities: Hyosung TNC profit improvement and share price

- Edaily/NH: Spandex supply-demand balance improvement

- CNews: China No. 3 spandex producer bankruptcy risk

- TIN News: Chinese competitor bankruptcy benefit

- Edaily/Hana: Price hike and competitor distress benefit

- TradingView/Hankyung: Target price raised from KRW 300k to 510k

- Asia Economy: Hyosung TNC jumps on spandex price hike

- FinancialContent: Lululemon Athletica investment case

- ChemAnalyst: PTMEG price trend and forecast

- Today Mild: NH Securities spandex supply improvement phase

- iM Securities: Hyosung TNC 298020 PDF

- Lead Economy: China steps aside for Hyosung TNC

- Naver Premium: No. 3 spandex producer bankruptcy risk expands

- Dealsite: Turnaround after Chinese low-price pressure