DEEP RESEARCH · E-Mart/Gmarket

E-Mart: Meaning of Gmarket Turnaround and KRW 400bn Bond Deal

The retail rerating logic from Star Delivery, Alibaba partnership, and refinancing

0. Bottom line first

The key for E-Mart is not low growth at hypermarkets alone, but whether Gmarket's loss reduction and lower financial risk are confirmed in numbers. Star Delivery, the Alibaba JV, and the successful KRW 400 billion bond issue suggest the market may be starting to view E-Mart as a turnaround candidate rather than only a traditional retailer.

- Traders is presented as a growth engine that surpassed KRW 1 trillion in quarterly revenue in a high-inflation environment.

- The source cites cases where sellers using Star Delivery saw average sales rise 160% after one year.

- Star Delivery covers about 150,000 products across 14 categories, with next-day arrival for weekday orders before 8 p.m. and KRW 1,000 compensation for delays.

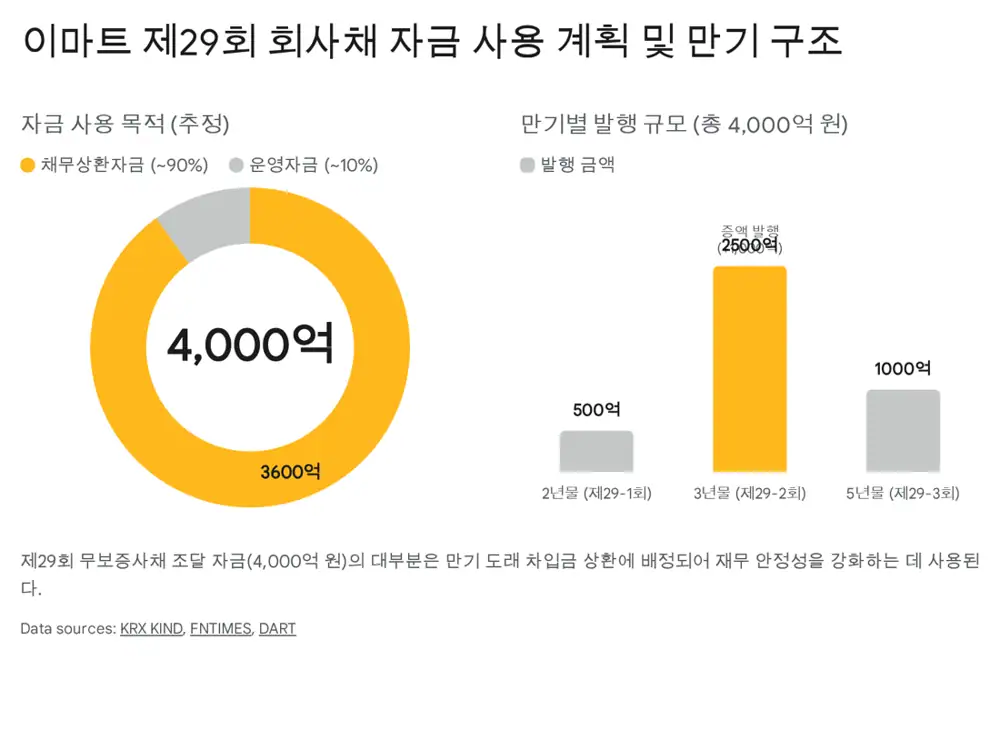

- The bond deal totals KRW 400 billion: KRW 50 billion in 2-year notes, KRW 250 billion in 3-year notes, and KRW 100 billion in 5-year notes.

1. E-Mart's Business Structure

Hypermarkets

Fresh-food strength and the No. 1 grocery strategy create defense in food, where online penetration is relatively low.

Traders

Bulk-value demand and paid membership raise basket size and lock-in.

SSG.COM and Gmarket

Online subsidiaries that caused losses are shifting from volume to profitability.

2. Why Gmarket Is Rebounding

Official fact: The source says sellers adopting Star Delivery recorded an average 160% sales increase after one year, and that the service covers about 150,000 products across 14 categories.

Interpretation: The important point is that Gmarket did not try to copy Coupang's direct fulfillment spending aggressively. Instead, it used CJ Logistics to build an arrival-guarantee service, reducing delivery uncertainty without sharply increasing fixed costs.

- The company is shifting from indiscriminate coupons to data-driven target marketing to improve ROAS.

- Promotions are being refined in high-commission or high-ticket categories such as fashion, beauty, and digital appliances.

- CEO Jung Hyung-kwon is presented as a platform and strategy figure who previously led Alibaba Korea and Alipay Europe, Middle East, and Korea.

3. Meaning of the Bond Financing

| Tranche | Size | Condition/meaning |

|---|---|---|

| 29-1, 2-year | KRW 50bn | 11bp below individual fair yield |

| 29-2, 3-year | KRW 250bn | Increased from KRW 150bn; 9bp below |

| 29-3, 5-year | KRW 100bn | 15bp below individual fair yield |

| Use of proceeds | Total KRW 400bn | Main purpose is debt repayment/refinancing |

Interpretation: Successful issuance below fair yield suggests institutional investors weighed E-Mart's turnaround potential more heavily than credit-risk concerns.

4. Financial Health and Capital Allocation

The source lists E-Mart's 2024 debt ratio at 157.4% and net-debt dependence above 30%. The burden remains, but the January 2026 bond issue diversified maturities, while cash-generative subsidiaries such as Traders and Starbucks Korea/SCK Company reduce near-term risk.

Capital allocation currently prioritizes debt repayment, store renewal, and IT infrastructure over dividends. If Gmarket earnings improve and the balance sheet stabilizes, more active shareholder returns can become possible.

5. Valuation and Risks

- The source frames PBR at around 0.2x, near historical lows.

- Street consensus target price is cited at about KRW 113,917.

- Main risks are delayed Alibaba JV results, conflicts of interest between the partners, and continued Coupang growth.

- Low growth, high inflation, and a weak won constrain consumer spending across retail.

6. Final View

E-Mart is stabilizing debt, maintaining cash generation in the offline core, and trying to turn Gmarket into an alliance-based platform. In 2026, the key will be whether offline recovery and online restructuring show up in reported numbers at the same time.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224166482355

- Source 2: https://www.g-enews.com/article/Distribution/2026/01/202601261447008871740eacf404_1

- Source 3: https://www.fntimes.com/html/view.php?ud=202601151751177719141825007d_18

- Source 4: https://v.daum.net/v/PdmO3Znb7l

- Source 5: https://www.chosun.com/english/industry-en/2024/12/27/FAIGC7ZOGVBHNM2PA5MJZFWNLY/

- Source 6: https://digitalchosun.dizzo.com/site/data/html_dir/2025/04/18/2025041880146.html

- Source 7: https://www.chosun.com/economy/market_trend/2025/04/20/TVKZQYBBCJD47F4RIAQGIMT5FI/

- Source 8: https://stardelivery.gmarket.com/seller_story/?bmode=view&idx=162809348

- Source 9: https://seo.goover.ai/report/202410/go-public-report-ko-0ac36bd7-cb62-47c5-b9ce-d7197408820d-0-0.html

- Source 10: https://www.infostockdaily.co.kr/news/articleView.html?idxno=213196

- Source 11: https://ceoscoredaily.com/page/view/2024122712481316884

- Source 12: https://m.ddaily.co.kr/page/view/2024122715402371180

- Source 13: https://v.daum.net/v/20251119163113796?f=p

- Source 14: https://biz.chosun.com/distribution/channel/2024/12/27/MJLG3I3UZ5EUHDEXGD5T75XN2Y/

- Source 15: http://www.sisaon.co.kr/news/articleView.html?idxno=179222

- Source 16: http://www.gncci.or.kr/front/boardlink/boardlinkContentsView.do?boardId=13&contId=20120943894&menuId=5109

- Source 17: https://www.shinsegaegroupnewsroom.com/2026-retail-market-outlook/

- Source 18: https://kind.krx.co.kr/external/2026/01/21/000083/20260121000127/10601.htm

- Source 19: https://news.einfomax.co.kr/news/articleView.html?idxno=4344167

- Source 20: https://kind.krx.co.kr/common/disclsviewer.do?method=searchInitInfo&acptNo=20260121000083&docno=

- Source 21: https://drive.google.com/open?id=1g6dCz1JnZf2clKhHax7HwZlgk_0xIGL7

- Source 22: https://comp.wisereport.co.kr/company/c1080001.aspx?cmp_cd=139480&cn=

- Source 23: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?pGB=1&gicode=A139480&cID=&MenuYn=Y&ReportGB=B&NewMenuID=Y&stkGb=701

- Source 24: https://drive.google.com/open?id=19aYk4GZmaivqSCix1kFeebrppPP6R85j