DEEP RESEARCH · Lam Research (LRCX)

Lam Research — the etch king becomes the master architect of advanced packaging

Front-end DNA grafted onto back-end, HBM / hybrid-bonding standardization, riding the 2026 $135B WFE

0. Bottom line first

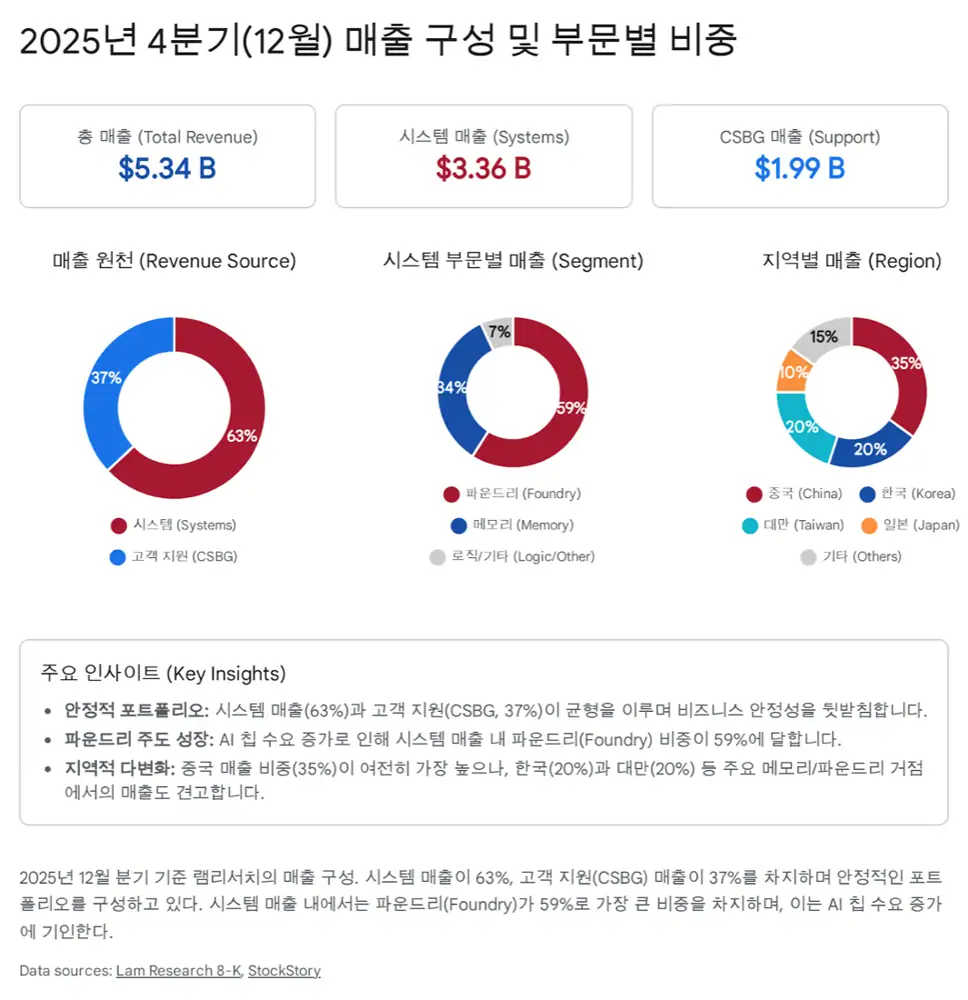

The 2012 Novellus deal completed Lam’s ‘etch + deposition + clean’ stack. Now the AI-driven ‘back-end becomes front-end’ shift (More than Moore) is turning Lam into the default supplier for advanced packaging. 2025 results — Dec quarter revenue $5.34B, FY $20.6B, Non-GAAP GM 49.7%, OPM 34.3% — confirm the start of the supercycle. 2026 WFE is guided at $135B (+23% YoY), inside which advanced-packaging tools should compound at 40%+. Four flagship tools (SABRE 3D, Syndion, VECTOR TEOS 3D, Striker) absorb the HBM4 / hybrid-bonding / GAA / BSPDN inflections all at once.

1. Why AI is rewriting the semi hardware playbook

Moore’s Law has hit physical limits — node scaling costs are exploding, performance gains are shrinking. The industry’s attention is moving to packaging — stacking and side-connecting chips in 3D to push system-level performance. More than Moore is opening both opportunity and risk for front-end giants.

On the Dec 2025 call, CEO Tim Archer said the company is matching AI’s acceleration with execution speed and that its expanded portfolio enables the move to smaller, more complex 3D devices and packages — i.e., Lam is positioning as an architect of the AI semiconductor ecosystem, not a tool vendor. Lam press release

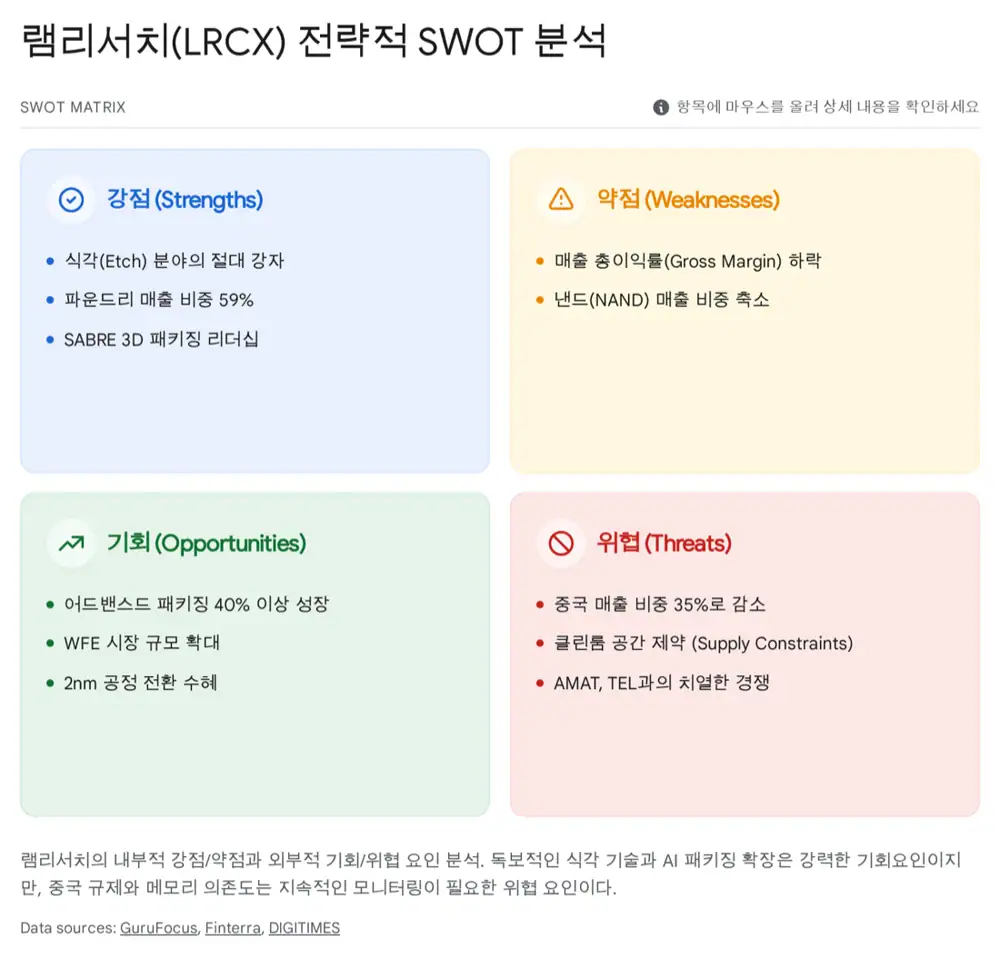

2. The business — where the moat comes from

2.1 Etch — the king

- 40–50% share in conductor/dielectric etch. Essentially monopolises 3D NAND channel-hole etch.

- Workhorses: Sense.i platform (best productivity per footprint), Vantex chamber (uniformity).

- Cryogenic etch is the breakthrough enabling 400-layer+ 3D NAND.

2.2 Deposition / clean

- ALTUS — ALD-based W / Mo metal deposition; essential for 3D NAND wordlines and logic interconnects.

- EOS / Da Vinci — spin-clean wafer cleaning.

2.3 CSBG — the ‘razor & blade’ engine

- Installed base of roughly 100,000 chambers.

- Dec-25 CSBG revenue was $1.99B (~37% of total) — not a side service but a core revenue pillar.

- Equipment Intelligence adds predictive maintenance — improving the quality of CSBG revenue.

2.4 2025 financial scorecard

| Metric | Value | Notes |

|---|---|---|

| FY 2025 revenue | $20.6B | — |

| Dec-25 quarter revenue | $5.34B | Above guidance midpoint |

| Non-GAAP GM (Dec-25) | 49.7% | Above guidance top end |

| Non-GAAP OPM (Dec-25) | 34.3% | — |

| FY25 R&D | $2.3B (~11% of revenue) | Sustained tech-leadership investment |

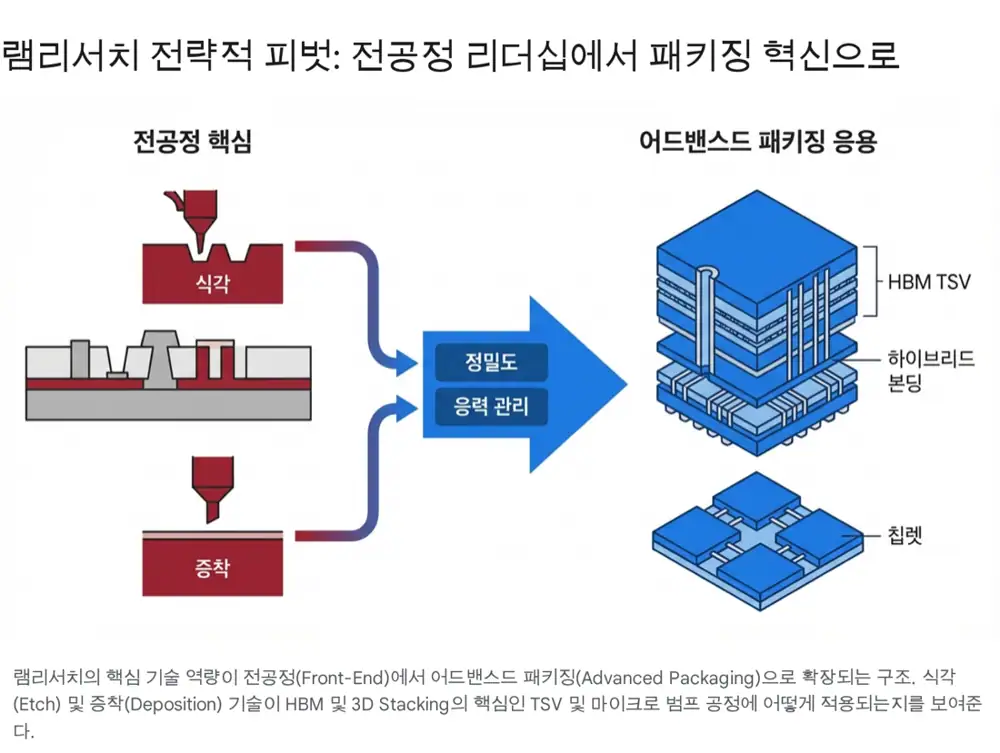

3. Advanced packaging — five-step analysis

3.1 Background

AI compute’s bottleneck is memory bandwidth. HBM solves it by stacking DRAM with thousands of TSVs for high-speed transfer. Chiplet and heterogeneous integration are becoming standard — they demand µm-level precise connection. That is the back-end becoming front-end. Lam — AI Revolution Relies on Advanced Packaging, Lam — Manufacturing Breakthroughs

3.2 Rationale

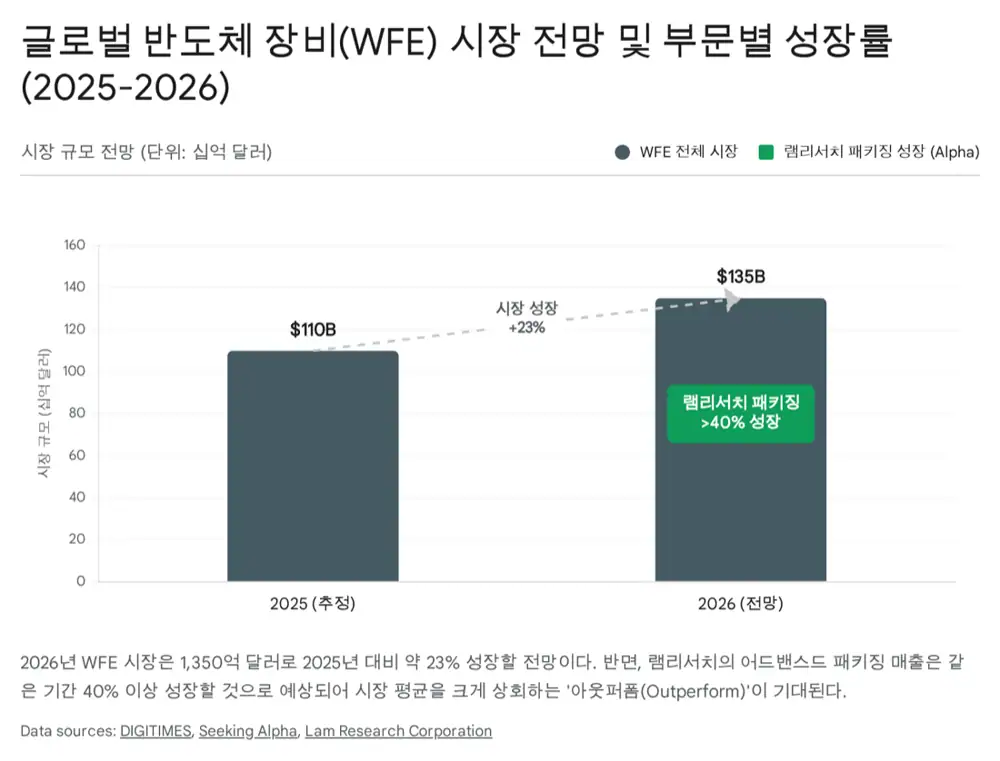

- Growth: Packaging tools should grow 40%+ vs ~23% for WFE overall — 2× the broader market.

- Moat: TSV formation, micro-bump plating, hybrid-bond surface prep all require nm-class control — directly transferable from front-end.

- Hedging: Offsets the risk of slowing logic-node scaling with high-margin packaging.

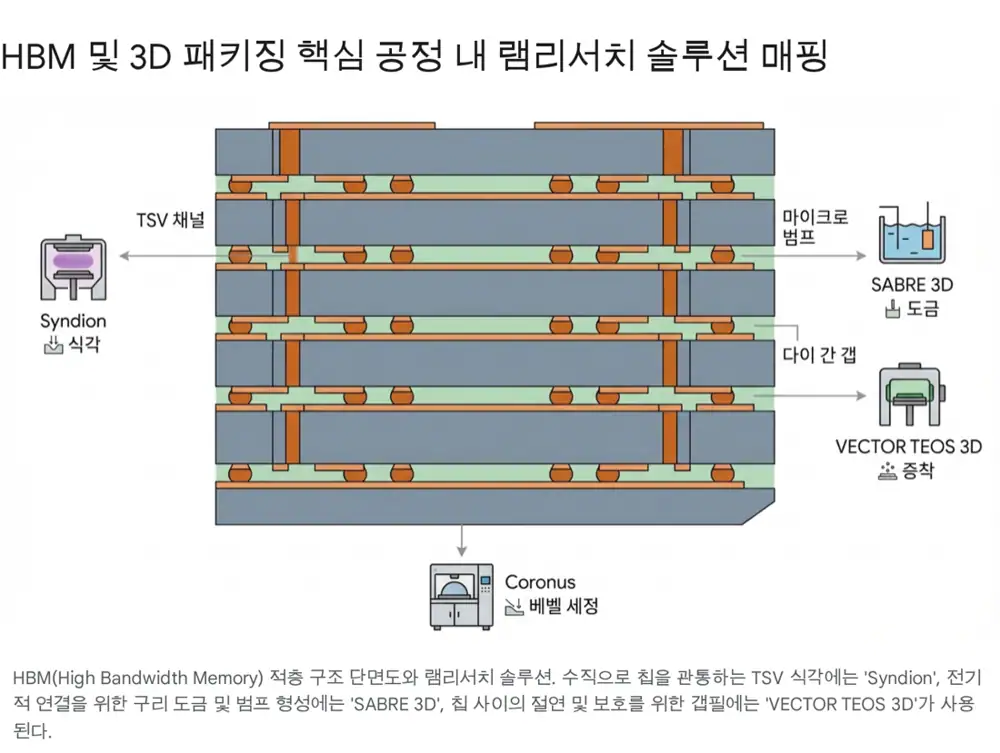

3.3 Players & method — ‘Lab-to-Fab’ + four flagship tools

SABRE 3D

Cu fill in TSVs, micro-bump formation. Mandatory on HBM lines; expects 5+pp share gain in 2025.

Syndion

High-aspect-ratio etch know-how applied to packaging — fast, smooth TSV profiles.

Striker

Atomic-layer surface films for hybrid-bonding yield.

Lam Packaging Solutions portal, Nasdaq — TEOS 3D bet

3.4 Timing — the HBM4 / accelerator roadmap

- 2025 (accelerators): Blackwell + HBM3E ramp → SABRE 3D / Syndion bookings surge. Packaging revenue expected to exceed $3B in 2025.

- 2026–27 (eruption): HBM4 (16-stack+), heterogeneous integration, hybrid bonding in volume.

4. Competition

| Competitor | Strength | vs Lam |

|---|---|---|

| Applied Materials (AMAT) | Broad packaging lineup, chiplet/PLP | Turn-key, but Lam leads in high-aspect-ratio etch and selected depositions. SemiWiki, Nasdaq — AMAT vs LRCX |

| Besi (NL) | Hybrid-bonding (die-bonding) leader | Symbiotic, not competitive — Lam surface prep + Besi bonding run side-by-side. Bits&Chips |

| Tokyo Electron (TEL) | Coater/developer monopoly; bonding/debonding | Direct etch competitor. TrendForce |

Differentiation: One of the only companies with all three of etch / deposition / clean — letting customers buy an optimised packaged stack. Semiverse Solutions virtual-fab simulation creates strong lock-in.

5. End-market — the 2026 $135B WFE supercycle

2026 WFE forecast is $135B, ~23% above 2025’s estimated $110B. Hyperscaler AI capex continues — HBM DRAM and AI-accelerator logic capacity is expanding. Growth path is back-end-loaded, accelerating into 2H as HBM4 ramps and 2nm enters. DigiTimes, Seeking Alpha, Deep Dive — Architect of the AI Era

Tech inflection — Lam tailwinds

- GAA (2nm-): The 4-side gate requires precise selective etch — new Akara expected to 2× its adoption.

- BSPDN (back-side power): Requires extreme wafer thinning and back-side processing — etch / clean become critical.

- 3D NAND scaling: Roadmap to 200-300+ and eventually 1,000 layers — cryogenic etch leadership. Fountyl — etch market, Intellectia — 2026 memory stocks

6. Valuation / risks

6.1 The ‘AI-infrastructure essential’ premium

Early-2025 forward P/E is ~45–50×, well above the historical 15–20×. The premium is being justified by the market’s re-rating of Lam as ‘AI-infrastructure essential.’ Finbox — fwd PER, Finbox — peers

Foundry/logic mix expanding to 59% and surging packaging revenue are reducing the ‘memory-cyclicality discount’. RBC raised PT $260 → $290; Cantor Fitzgerald to $320. RBC, Cantor Fitzgerald, InsiderFinance — earnings beat, Futurum — Q2 FY26

6.2 Risks

- China export controls: ~35% of Dec-25 revenue is China. Further tightening remains possible — mitigation via Malaysia and other supply-chain diversification.

- Memory cycle: Slow recovery in consumer PC/smartphone could push memory makers to slow capex — short-term earnings risk.

- Tech-competition: If Lam fails to set standards in hybrid bonding etc., growth momentum could ease.

7. Summary — master architect of the AI era

Front-end → packaging

Key supplier to HBM / 3D packaging; SABRE 3D, Syndion lead growth.

$135B WFE

AI-chip manufacturing tools in sustained demand; packaging segment grows fastest.

CSBG stable cash

~100k installed chambers buffer memory-cycle volatility.

Despite short-term earnings swings and geopolitical risk, Lam is an indispensable player in the long-term AI semiconductor ecosystem. The moat strengthens as ‘back-end becomes front-end’ progresses — supporting today’s premium multiple. Next things to watch: share gains in hybrid bonding and glass-substrate readiness.

Sources

- Naver blog source: m.blog.naver.com/.../224166265873

- Deep Dive — Architect of the AI Era: financialcontent.com

- Lam Research — June 2025 earnings slides: PDF

- Lam — AI Revolution Relies on Advanced Packaging: newsroom.lamresearch.com

- DigiTimes — $20.6B FY revenue, 2026 WFE $135B: digitimes.com

- Nasdaq — TEOS 3D bet: nasdaq.com

- Fountyl — etch market analysis: fountyltech.com

- Intellectia — 2026 memory stocks: intellectia.ai

- Lam — Manufacturing Breakthroughs in Chip Packaging: newsroom.lamresearch.com

- Lam IR — VECTOR TEOS 3D launch: investor.lamresearch.com

- Lam Packaging Solutions portal: lamresearch.com

- Lam — Dec 2025 quarter results: newsroom.lamresearch.com

- Nasdaq — AMAT vs LRCX: nasdaq.com

- SemiWiki — Comparing AMAT with Lam Research: semiwiki.com

- Bits&Chips — Solmates to Lam, Besi to Applied: bits-chips.com

- BCG matrix — Besi competitive landscape: matrixbcg.com

- TrendForce — Chip Tool Giants Accelerate Packaging Push: trendforce.com

- Lam — Semiverse Solutions: lamresearch.com

- Seeking Alpha — $135B WFE forecast: seekingalpha.com

- Futurum — Q2 FY 2026 Highlights: futurumgroup.com

- Finbox — forward PER: finbox.com

- InsiderFinance — earnings beat: insiderfinance.io

- Finbox — peer comparison: finbox.com

- RBC Capital — PT raised to $290: investing.com

- Cantor Fitzgerald — PT raised to $320: investing.com