DEEP RESEARCH · DongA Eltek

DongA Eltek: Sunic System's 2025 J-curve and an OLED equipment holdco re-rating

A combined view of the inspection-equipment cash cow, OLED deposition growth engine, and K-Display policy tailwind

0. Bottom line first

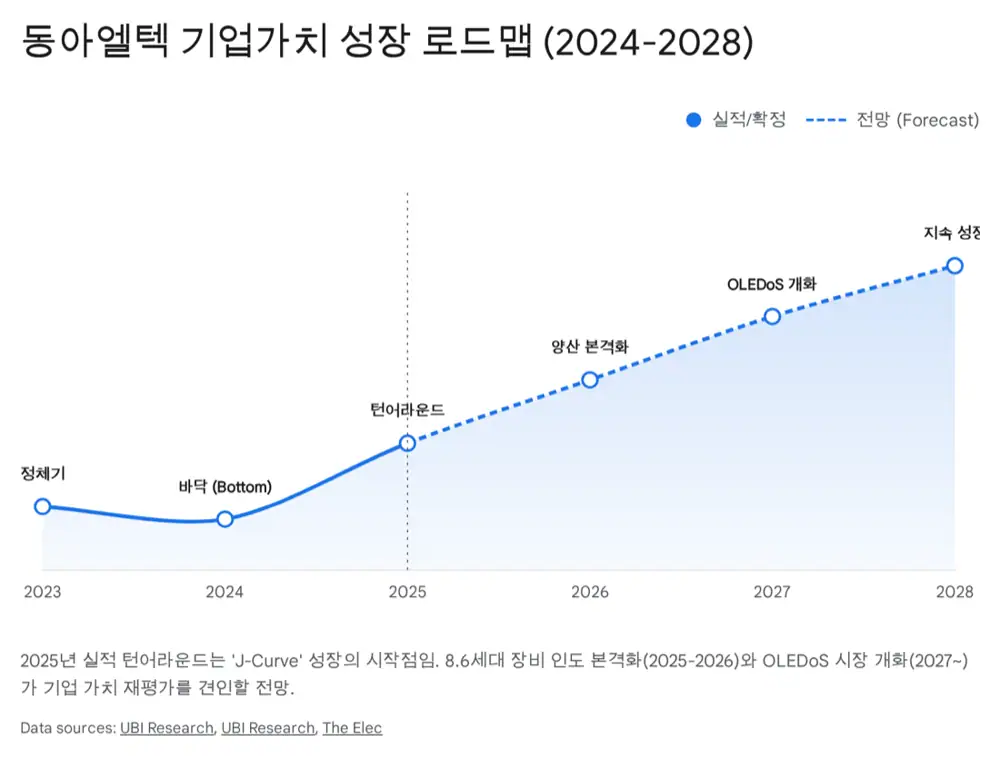

My view is that DongA Eltek's 2025 earnings surprise was not just a rebound. It was a structural inflection where Sunic System's Gen-8.6 OLED and OLEDoS deposition equipment became the center of consolidated earnings.

Official fact: The source cites 2025 provisional consolidated revenue of KRW 582.4bn, up 226.4%; operating profit of KRW 113.4bn, up 669.6%; and net profit of KRW 96.4bn, reversing a KRW 43.3bn loss in the prior year.

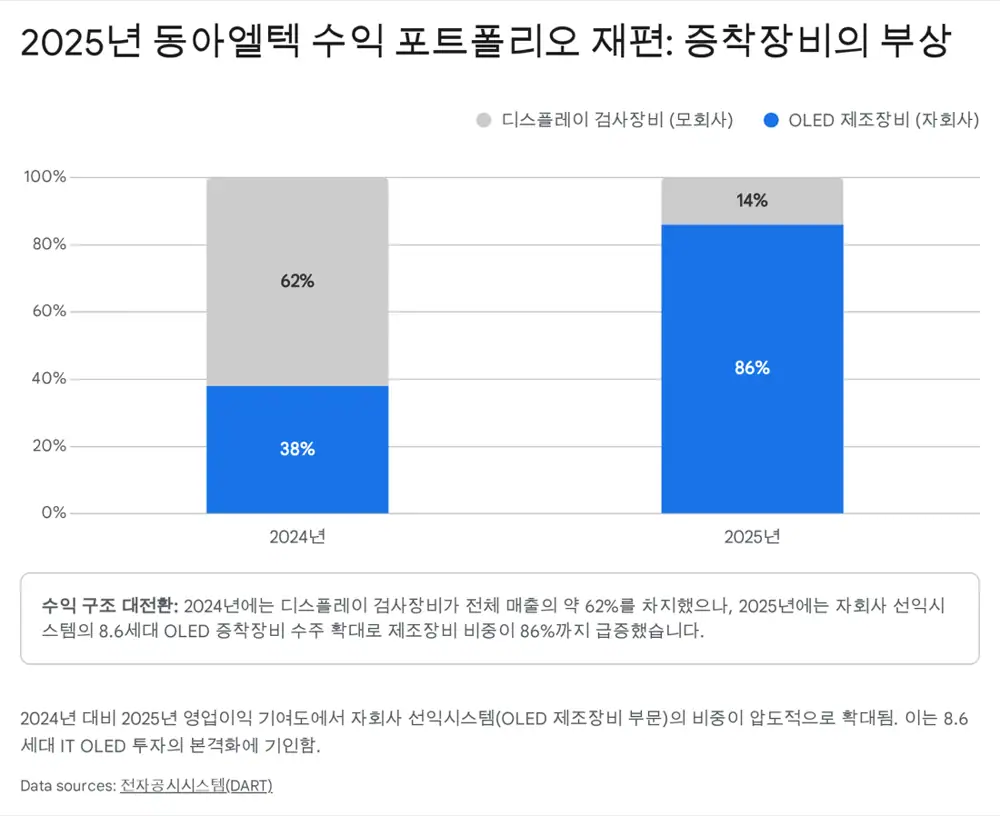

Interpretation: The quality of the numbers comes from large OLED deposition-equipment revenue recognition at Sunic System. DongA Eltek should now be viewed as an operating holding company with both a Sunic stake and a legacy cash cow, not just as an inspection-equipment stock.

KRW 582.4bn

2025 consolidated revenue increased 226.4% year on year.

KRW 113.4bn

The source calculates 2025 operating margin at about 19.5%.

KRW 96.4bn net profit

The company fully turned around from a KRW 43.3bn net loss in the prior year.

1. Operating holdco structure: legacy business plus Sunic System

DongA Eltek is not a pure holding company. It runs its own manufacturing business while controlling a key subsidiary. The parent makes display inspection equipment, while Sunic System makes OLED deposition equipment. One side provides steady cash flow; the other can lift earnings stepwise when large orders are recognized.

| Affiliate | Stake or position | Source role |

|---|---|---|

| Sunic System | DongA Eltek 47.14%, effective 51.47% after treasury shares | Core OLED deposition-equipment asset explaining 70-80% of group value |

| Prime Engineering | 100% subsidiary | Equipment parts machining and assembly, utilization tied to Sunic orders |

| DA Value Investment | 100% subsidiary | Venture investing and exit gains, sensitive to rates and IPO slowdown |

| SUNIC SYSTEM Chengdu | 100% owned by Sunic System | Customer support and CS hub for BOE and other Chinese customers |

2. Growth engine: Sunic System and Gen-8.6 OLED

The source says OLED manufacturing equipment accounted for more than 80% of consolidated revenue in 2025 and generated most operating profit. Gen-8.6 IT OLED deposition equipment and micro OLED, OLEDoS, equipment are described as high-margin products that lifted group profitability.

BOE B16

The source views selection for BOE's B16 Gen-8.6 deposition equipment as the event that changed the earnings level.

Canon Tokki challenger

Sunic is framed as the key challenger in large OLED deposition equipment, where Japan's Canon Tokki has been dominant.

KRW 41bn order

An early-2026 KRW 41bn micro OLED mass-production deposition equipment order supports the technology story.

3. Legacy business: inspection equipment and the Demura moat

DongA Eltek's own business is not explosive, but it is the group's base. It supplies light-leak inspection systems, aging equipment, and image-quality correction equipment to customers such as LG Display, while also generating maintenance revenue from installed equipment.

Official fact: The source identifies Demura, which detects and corrects pixel-to-pixel luminance unevenness in OLED panels, as the core technology of DongA Eltek's own business.

Interpretation: As IT OLED and automotive displays become higher resolution, correction algorithms and inspection precision become more important. Sunic's deposition orders and the parent's inspection business may move together.

4. Capital allocation: CAPEX, R&D, and dividend optionality

| Item | Source number or detail | Meaning |

|---|---|---|

| Pyeongtaek Brain City new plant | About KRW 19bn new facility investment | Assembly and testing space for large Gen-8.6 deposition equipment |

| R&D | Reinvestment to catch Canon Tokki and lead micro OLED | Technology independence supported by materials/parts/equipment policy |

| Balance sheet | End-2025 liabilities KRW 260.5bn, assets KRW 502.6bn | Debt ratio about 108%; real debt burden eased after contract liabilities |

| Dividend | Historical dividend around KRW 150 per share in profitable years | KRW 96.4bn 2025 net profit raises the possibility of dividend resumption or expansion |

5. Peer comparison: between APS and SFA

The source compares DongA Eltek with APS and SFA. APS is an OLED technology holding company betting on FMM material localization, while SFA is a mid-sized equipment group that expanded from display logistics equipment into semiconductors and secondary batteries.

| Item | DongA Eltek | APS |

|---|---|---|

| Core battleground | Deposition equipment | FMM core material |

| Revenue structure | Stepwise growth from large equipment orders | Recurring material revenue if commercialization succeeds |

| Risk | Front-end investment-cycle volatility | Long R&D and commercialization failure risk |

| Market view | The source says market cap is below 30-40% of Sunic stake value | Higher multiple reflecting future material expectations |

| Investment character | Value stock proven by earnings | Growth stock driven by technology expectations |

6. Policy and industry trend: K-Display 2027 and on-device AI

Korea's K-Display 2027 strategy aims to regain global leadership and induce KRW 65tn of private investment. The source says OLED and micro displays designated as national strategic technologies can receive up to 15-25% tax credits for R&D and capex, while KRW 900bn of policy financing can support funding stability.

On the industry side, on-device AI can accelerate OLED adoption in laptops and tablets. AI-device OLED uses a two-stack tandem structure to raise lifetime and brightness, and the source explains that this can theoretically double deposition process demand.

The watchpoints are order backlog through 2026-2027 and expansion into Chinese and global customers. The 2025 numbers should be read as a signal that years of technology investment have entered the harvesting period.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224165872056

- UBIResearch BOE archives: https://en.ubiresearchnet.com/tag/boe/

- UBIResearch OLED for IT archives: https://en.ubiresearchnet.com/tag/oled-for-it/

- Sunic System investment analysis: https://ai.skill.or.kr/entry/Sunic-System-Investment-Analysis-Core-beneficiary-of-Gen-8-OLED-OLEDoS-deposition-upcycle

- Hankyung Sunic micro OLED order: https://www.hankyung.com/article/202601088908L

- K-Display 2027 YouTube: https://www.youtube.com/watch?v=nyR0-ybx9D0

- Digital Daily K-Display 2027: https://m.ddaily.co.kr/page/view/2023051815472618684

- Yeongnam Economy materials company support: https://www.ynenews.kr/news/articleView.html?idxno=70831