DEEP RESEARCH · SK NETWORKS/MINTIT

SK Networks: Re-Rating MINTIT in the Chipflation Era

How treasury-share cancellation and rising smartphone prices could reshape used-phone platform value.

0. Bottom line first

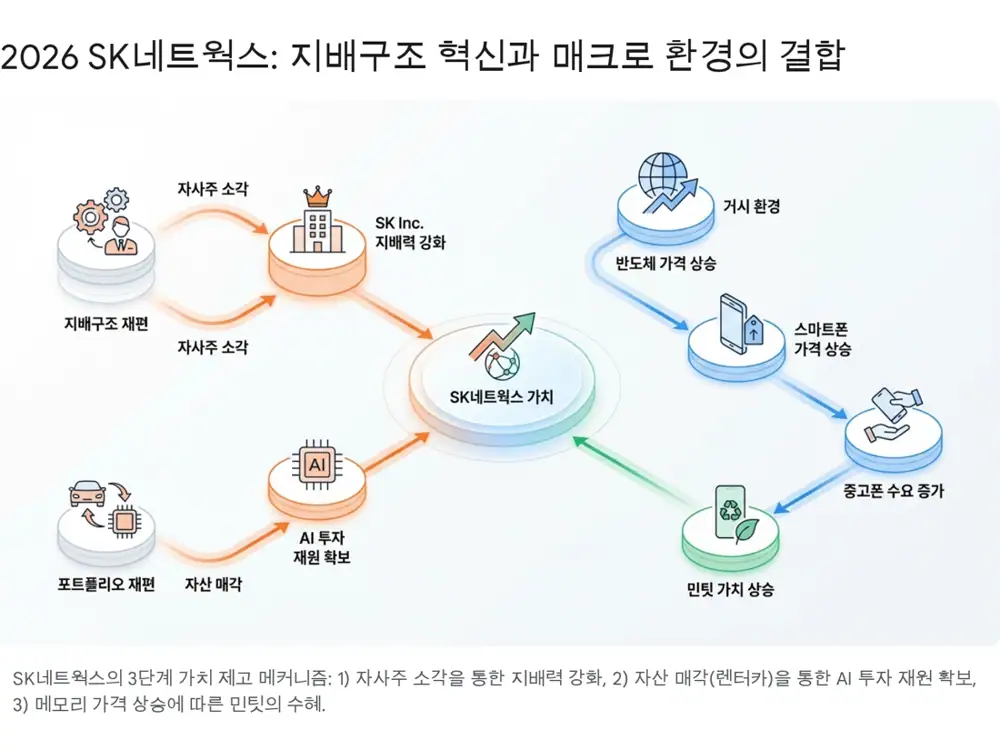

The source redefines SK Networks as an AI-driven operating investment company rather than an old trading and rental company. Within that frame, MINTIT is not just a used-phone collection machine; it is a platform that can benefit when memory-price inflation pushes up new smartphone prices and used-phone residual values.

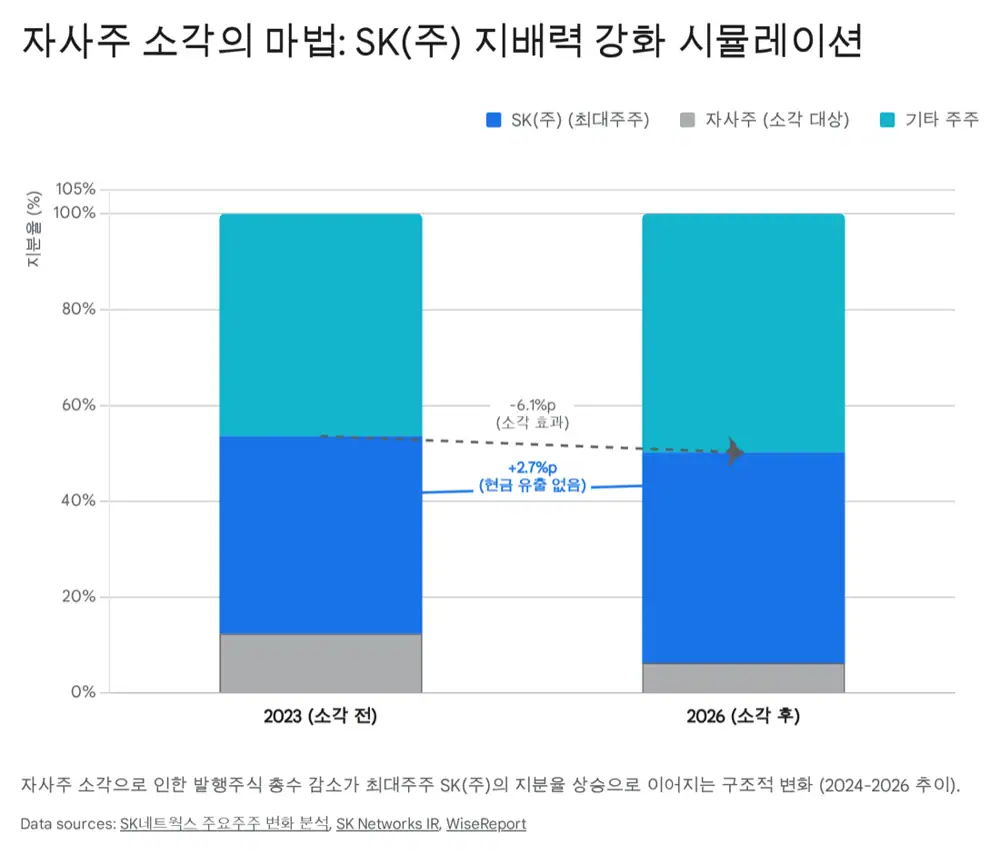

Official fact: The source says SK Inc.’s stake rose from 41.20% to 44.76% as of Jan. 15, 2026, while treasury shares fell from 12.40% to 6.10%. It also says MINTIT surpassed 4.5 million cumulative purchased devices as of October 2025.

Interpretation: Treasury cancellation is financial engineering that can support both minority-shareholder return and controlling-shareholder influence. MINTIT can enter a P-Q simultaneous growth zone if chipflation lifts both used-phone purchase prices and transaction volume.

1. Governance: the dual effect of treasury-share cancellation

The source views the Jan. 15, 2026 shareholder register not as a simple list of percentages but as the result of two years of financial engineering aimed at both shareholder return and control reinforcement.

| Shareholder | Type | End-2023 | Jan. 15, 2026 | Change | Main reason |

|---|---|---|---|---|---|

| SK Inc. | Largest shareholder | 41.20% | 44.76% | +3.56%p | Natural stake increase from treasury cancellation |

| National Pension Service | Institution | 6.12% | 5.15% | -0.97%p | Portfolio rebalancing and profit taking |

| Choi Sung-hwan | Business head | 3.12% | 2.90%(est.) | -0.22%p | Partial sales for gift-tax funding and offsetting cancellation effect |

| Treasury shares | Treasury stock | 12.40% | 6.10% | -6.30%p | Strategic cancellation for shareholder value |

| Others | Free float | 37.16% | 41.09% | +3.93%p | More active trading and slight foreign-ownership increase |

Official fact: The post says SK Inc. owns about 99,033,269 shares, representing 44.76%. Treasury shares were about 12.4% in early 2024, but after 14.5mn shares were cancelled in March 2024 and additional cancellation policies followed, treasury shares were down to the 6% range in 2026.

Interpretation: The math of cancellation is denominator reduction. SK Inc. increased its stake without cash outflow while also gaining an EPS-improvement and overhang-removal shareholder-return narrative. I view it as lowering governance risk while creating a Value-Up story.

2. Choi Sung-hwan’s changing role

The source estimates Business Head Choi Sung-hwan’s standalone stake at around 2.9% as of January 2026. That is not enough to defend control alone, but his group standing is described as stronger because AI and global investment businesses were moved to the front.

- Stake movement: After aggressive open-market purchases in the past, the post says he sold some shares or paused buying from 2024 to fund gift taxes and rebalance personal assets.

- Responsible management: The 2026 organization places AI and global investment at the center, while board-centered governance and professional management help offset the low personal stake.

- Interpretation: The source’s key point is a move from pure succession math to proving leadership through business performance.

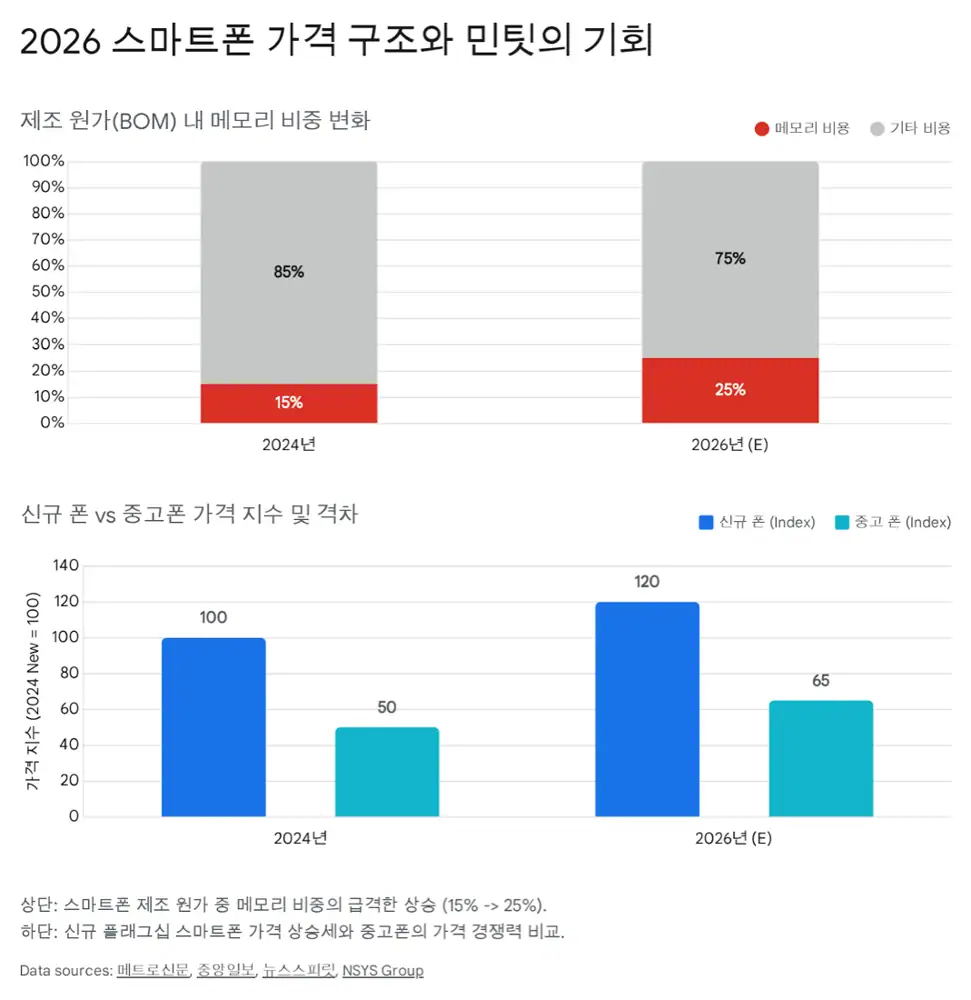

3. Chipflation: memory shortages pressure phone prices

The source argues that the memory-semiconductor supercycle that began in 2H25 became a cost shock for smartphones in 2026. Generative AI demand has concentrated capacity into HBM and high-capacity DDR5, reducing room for mobile LPDDR and NAND flash.

| Item | Source figure/content | Meaning |

|---|---|---|

| Memory prices | Expected to rise 40-50%+ YoY in 1Q26 | Cost pressure for smartphones and PCs |

| Smartphone NAND | About 100% increase | Major driver of BOM inflation |

| Memory share of BOM | From 10-15% historically to more than 20% in 2026 | Structural change in finished-device pricing |

| Galaxy S26 | KRW 100,000-150,000 price hike under review by model | High-capacity memory for on-device AI |

| 2026 smartphone shipments | Expected to decline about 2% YoY | Backdrop for used-phone substitution |

Interpretation: If AI data centers absorb the best memory capacity, smartphone makers must either raise flagship prices or cut low-end models. For consumers, new phones become expensive and choices narrow.

4. MINTIT: structural beneficiary of chipflation

Higher new-phone prices lift used-phone residual values. The source expects this to activate MINTIT’s transaction platform.

Substitution demand

If new flagships exceed KRW 2mn, demand can rise for S-grade phones from one or two years ago.

Higher residual value

When consumers believe “selling now pays,” dormant phones are more likely to flow into MINTIT ATMs.

Emerging-market demand

Used-phone demand is strong in emerging markets under global inflation, and a high FX environment can help export channels.

Official fact: The source says MINTIT surpassed 4.5mn cumulative purchased devices as of October 2025 and could set a new annual purchase-volume record in 2026.

MINTIT’s moat is AI visual inspection and trusted data erasure. The source says MINTIT ATMs use vision AI to grade exterior condition within seconds, while Q-Eraser and similar data-deletion technology provides irrecoverable deletion and certificates that reduce privacy concerns.

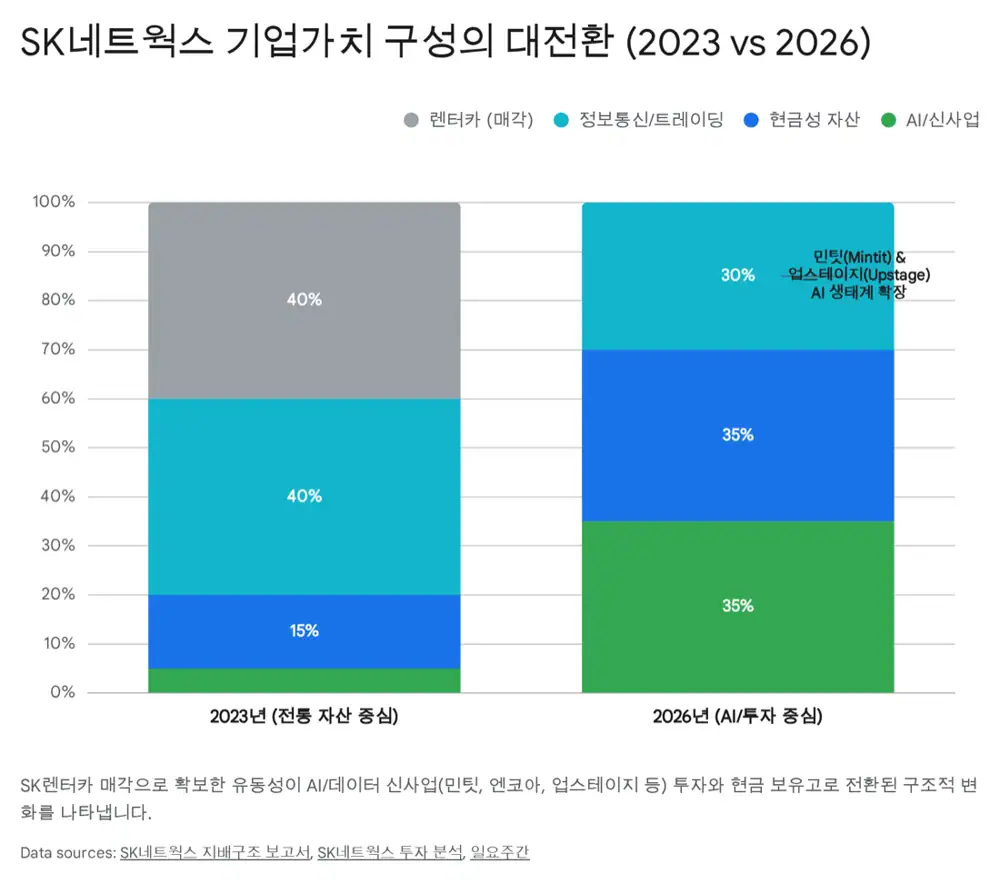

5. MINTIT valuation and IPO scenario

The source says SK Networks is timing MINTIT’s IPO so the market values it as a data platform using P/E or EV/EBITDA, not as a simple distribution-margin business using P/S.

| Item | Source content | Investment watch point |

|---|---|---|

| 2025 target | Annual revenue target of KRW 100bn | Base revenue scale |

| 2026 growth | Chipflation could drive growth above 20-30% YoY | Whether P and Q rise together |

| Profitability | Higher mix of data-erasure solution licensing and AI-inspection B2B sales | Multiple shift from distributor to technology platform |

| 2024 value | Market value around KRW 300-400bn | Historical benchmark |

| 2026 value | Conservative KRW 600bn to as high as KRW 1tn discussed | Subsidiary value versus SK Networks market cap in the low KRW 1tn range |

The possible IPO window is described as 2H26 or 1H27. Proceeds are expected to support global used-phone distribution, AI technology upgrades, and investments in robotics and new businesses.

6. Conclusion: can the company turn a shock into platform value?

The source concludes that SK Networks can no longer be evaluated only with its old trading and rental-company yardstick. Treasury cancellation created both shareholder-friendliness and control reinforcement, while the memory-price spike created a favorable soil for MINTIT through higher used-phone residual value.

Bull Case

- Higher smartphone prices suppress new-device demand and lift both used-phone volume and price.

- MINTIT expands AI inspection and data-erasure technology into B2B solutions.

- Pre-IPO earnings maximization brings valuation closer to the KRW 600bn-1tn range.

Bear Case

- If memory prices normalize faster than expected, the used-phone price-up logic weakens.

- MINTIT may be valued as a distributor rather than receiving a platform multiple for AI and data erasure.

- If the operating-investment-company strategy does not improve cash flow, the conglomerate discount remains.

7. Checklist

- SK Inc. stake and remaining treasury-share balance

- Mobile memory prices and 2026 smartphone launch-price increases

- MINTIT monthly device purchases, ASP, and B2C channel growth

- B2B sales mix from data-erasure solutions and AI inspection technology

- MINTIT IPO underwriter, preliminary-review filing, and valuation method

My key question is whether MINTIT is recognized as an AI-based circular-economy data platform, not just a used-phone distributor. That requires 2026 chipflation benefits to show up in transaction volume, unit price, and profitability at the same time.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224165216807

- Reference 1: https://drive.google.com/open?id=1b8RBExYBaKV5NI6N1GG31ZZ6O_0k3KfIlQIkyg6Xaxw

- Reference 2: https://www.sknetworks.co.kr/en/ir/stock/stock-price-information

- Reference 3: https://comp.wisereport.co.kr/company/c1070001.aspx?cmp_cd=001740&cn=

- Reference 4: https://www.sknetworks.co.kr/pr/news-room/15814?currentPage=&searchWord=

- Reference 5: https://www.chosun.com/economy/industry-company/2026/01/21/KMOIQH6SM5GBPFJ3S2K7O75PIY/

- Reference 6: https://mobile.newsis.com/view/NISX20250520_0003183247

- Reference 7: https://www.newswire.co.kr/newsRead.php?no=1024638

- Reference 8: https://marketin.edaily.co.kr/News/ReadE?newsId=03562086645322968

- Reference 9: https://www.g-enews.com/article/Global-Biz/2026/01/2026012221113328939a1f309431_1

- Reference 10: https://api.emetro.co.kr/article/20260121500530

- Reference 11: https://www.cstimes.com/news/articleView.html?idxno=689962

- Reference 12: https://www.metroseoul.co.kr/article/20260121500530

- Reference 13: https://www.joongang.co.kr/article/25401093

- Reference 14: https://www.newsspirit.kr/news/articleView.html?idxno=28256

- Reference 15: https://www.dailian.co.kr/news/view/1604497

- Reference 16: https://www.digitaltoday.co.kr/news/articleView.html?idxno=620759

- Reference 17: https://quasarzone.com/bbs/qn_hardware/views/1924155?_method=post&_token=46mAOUKM18lMhgGJTyElPxsp2GmpyhOTdQx8lLTH&category=CPU%2FMB%2FRAM&kind=subject&page=1&sort=num%2C%20reply

- Reference 18: https://counterpointresearch.com/en/insights/2026-smartphone-shipment-forecasts-revised-down-as-memory-shortage-drives-bom-costs-up

- Reference 19: https://www.businesswire.com/news/home/20260129170791/en/Omdia-Global-Smartphone-Market-Grew-2-in-2025-While-Memory-Headwinds-Set-the-Stage-for-a-Challenging-2026

- Reference 20: https://www.sknetworks.co.kr/business/mintit

- Reference 21: https://v.daum.net/v/x0tv4yiPz3?f=p

- Reference 22: https://www.sknetworks.co.kr/en/business/mintit

- Reference 23: https://www.thekunm.com:51450/bbs/board.php?bo_table=info&wr_id=369&sfl=mb_id%2C1&stx=admin&sst=wr_hit&sod=desc&sop=and&page=3

- Reference 24: https://www.ilyoweekly.co.kr/news/newsview.php?ncode=1065574381033758&dt=m

- Reference 25: https://news.crunchbase.com/public/crunchbase-predicts-15-companies-ipo-ai-fintech-defense-forecast-2026/

- Reference 26: https://www.trendingtopics.eu/ipos-2026-will-anthropic-spacex-and-openai-rock-the-stock-market/