DEEP RESEARCH · SK NETWORKS

SK Networks: AI Investment-Company Transition and Shareholder-Value Rebuild

A combined view of the rental-car sale, treasury-share cancellation, spin-offs, and Upstage/En-core/Incross strategy.

0. Bottom line first

My key read is that SK Networks is changing its identity from a distribution and rental-car conglomerate into a business-oriented investment company built around AI, data, and wellness robotics. Shareholder returns and control reinforcement were not separate events; they were part of the same restructuring.

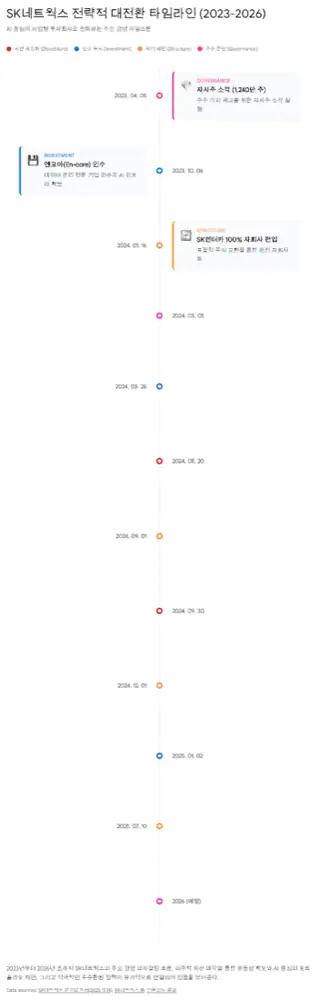

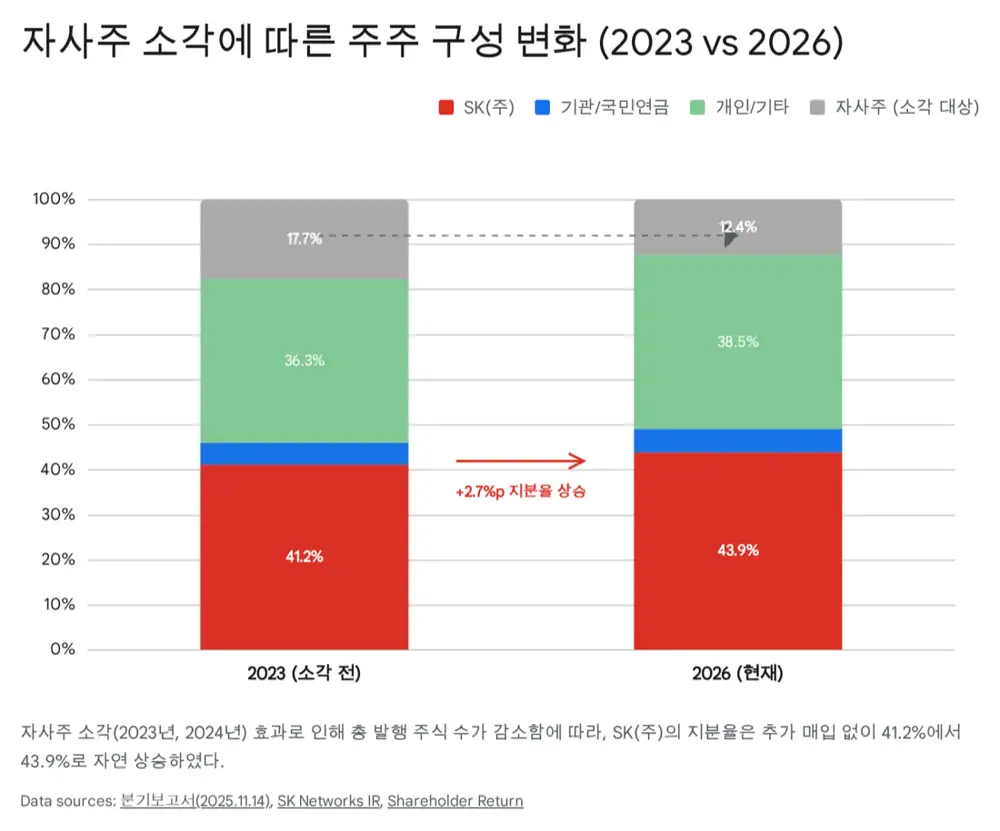

Official fact: The source says SK Inc.'s stake in SK Networks rose from about 41.2% in early 2023 to about 43.9% by late 2025, mainly through treasury-share cancellation rather than direct share purchases. On March 5, 2024, SK Networks canceled 14,500,363 common shares, about 6.1% of shares outstanding at the time, following the cancellation of 12.4M shares in April 2023.

Interpretation: Treasury-share cancellation created a dual effect: per-share value improvement for minority holders and stronger control for the largest shareholder without new cash outlay. This links naturally to Korea's corporate value-up agenda and the argument for easing holding-company discount.

1. Shareholder structure: control strengthened by buyback cancellation

The source reads the January 2026 shareholder structure as a financially engineered outcome designed to stabilize control and improve shareholder value at the same time. The structure minimizes direct cash injection from the major shareholder while raising per-share value for minority investors.

| Shareholder | Type | Stake | Note |

|---|---|---|---|

| SK Inc. | Largest shareholder | 43.9% | Stake rose through treasury-share cancellation |

| Individuals and others | Minority/free float | 24.0% | Free-floating shares |

| National Pension Service | Institutional investor | 5.2% | Major institutional investor |

| Treasury shares | Treasury stock | 12.4% | Potential future cancellation or M&A resource |

| Foreign investors | Overseas investors | 11.3% | Global funds and others |

Official fact: The source presents the table as reconstructed from SK Networks' Q3 2025 management-results report and quarterly filing.

President Choi Sung-hwan and owner-risk cleanup

- The source says Choi Sung-hwan aggressively bought SK Networks shares in the market from 2022 to 2023, becoming the largest individual shareholder.

- Around April 2024, he sold part of his SK Inc. holdings to secure funds for gift-tax payments and adjust his asset portfolio.

- The reduction in former chairman Chey Shin-won's holdings is interpreted as a signal that old owner risk has faded and the leadership transition toward Choi Sung-hwan has largely completed.

2. Business restructuring: rental-car sale and spin-offs

The source interprets the 2024-2025 sales and spin-offs as funding and efficiency measures for the shift toward an AI-centered business investment company. It describes the process as shedding the old general-trading shell and moving toward higher-value portfolio management.

Official fact: In August 2024, SK Networks completed the sale of 100% of SK Rent-a-Car to Affinity Equity Partners for about KRW 820B. The source explains that although rental cars were a stable cash cow, the business depended heavily on vehicle-purchase debt, often with leverage above 500%, pressuring SK Networks' consolidated balance sheet.

Interpretation: The SK Rent-a-Car sale was not just disposal of a non-core asset. It reduced consolidated leverage pressure and secured capital for AI investment. The source says consolidated debt ratio had approached 2,000% before the sale and treats the KRW 820B cash inflow as seed capital for debt repayment and new investment.

SK Speedmate

Focuses on auto maintenance and parts distribution, while pursuing DAT-based AI estimating and the Huckleberry Pro O2O platform.

Glowide

Separates the chemical-materials trading business and shifts away from commodity products toward higher-margin items.

Intermediate holding model

Headquarters focuses on investment and portfolio management while subsidiaries focus on operations.

3. AI value chain: internalizing data, models, and services

As of January 2026, the source argues that SK Networks' value is now driven less by handset distribution or rental cars and more by AI portfolio growth. The key is moving beyond passive AI investing and internalizing a data-tech-service value chain.

| Asset | Source point | Valuation meaning |

|---|---|---|

| Upstage | SK Networks led the early-2024 Series B with about KRW 25.0B. In August 2025, Upstage raised about USD 45M, roughly KRW 60.0B, in a bridge round backed by Amazon, KDB, AMD, and others. | Preparing for a 2026 IPO, with market estimates of KRW 2T-3T valuation and SK Networks' estimated stake around 7.11%. |

| En-core | Data-management specialist acquired in 2023; selected for Emerging AI+X Top 100 for a second straight year in 2025. | Data assetization and internal group synergy base. |

| Incross | In January 2026, SK Networks acquired about 36% from SK Square and became the largest shareholder. Incross operates AI-curated commerce service T deal. | Expands B2C touchpoints and provides ad/commerce data for AI learning. |

| PhnyX Lab and others | Silicon Valley investment start-ups continuously inject advanced technology. | Global network and technology scouting function. |

Interpretation: If Upstage stake value is the SOTP re-rating catalyst, En-core and Incross are more about operating synergy. SK Networks needs data and commerce channels to become an AI business operator rather than just an AI investor.

4. Shareholder returns and market outlook

Because volatility can rise during the shift into a business investment company, SK Networks is pairing the transition with shareholder-return policies to build trust.

- Interim dividend: The interim dividend introduced in 2024 continued in 2025, and the source cites a dividend of around KRW 50 per share.

- Treasury-share policy: The company has adopted a buy-and-cancel principle and keeps the possibility of further buybacks and cancellations open.

- Regulation: Discussions around mandatory treasury-share cancellation could increase shareholder-return pressure on companies with large treasury-share balances.

Official fact: The source says that as of January 2026, sell-side targets were being revised upward. In SOTP valuation, the combined value of assets such as SK Magic, En-core, Upstage, and Incross matters; if Upstage's expected market cap exceeds KRW 2T, SK Networks' stake alone could be worth several hundred billion won.

Risk factors

- Possible handset-distribution margin pressure in the ICT division, especially from abolition of the handset subsidy law.

- Short-term margin damage from early marketing costs in new AI businesses.

- Global economic uncertainty and interest-rate volatility.

- Potential delay in Upstage IPO success and Incross synergy realization.

5. Final view

Interpretation: My conclusion is that SK Networks in 2026 can no longer be viewed only as SK Group's distribution window. Capital from the SK Rent-a-Car sale, governance improvement through treasury-share cancellation and spin-offs, and Choi Sung-hwan's AI value-chain vision are moving in the same direction.

Investors should focus less on short-term earnings and more on AI portfolio growth and cross-subsidiary synergy speed. Upstage's listing, Incross integration, En-core data-business expansion, and additional shareholder returns are the verification points for reducing the holding-company discount.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224165174319

- SK Inc. Shareholder Information: https://www.sk-inc.com/en/ir/stockInformation.aspx

- SK Networks research PDF: https://ssl.pstatic.net/imgstock/upload/research/company/1708385430338.pdf

- SK Networks Shareholder Return: https://www.sknetworks.co.kr/en/ir/stock/shareholder-return

- PRESS9: https://www.press9.kr/news/articleView.html?idxno=70407

- DealSite: https://dealsite.co.kr/articles/90324/089060

- MK: https://www.mk.co.kr/en/business/11035972

- IB Tomato: https://www.ibtomato.com/Mobile/mView.aspx?no=7616

- Business Post: https://www.businesspost.co.kr/BP?command=article_view&num=394748

- G9 Inside: https://g9inside.com/?p=50842

- KED Global: https://www.kedglobal.com/private-equity/newsView/ked202404160013

- Eroun Net: https://www.eroun.net/news/articleView.html?idxno=44103

- Businesskorea: https://www.businesskorea.co.kr/news/articleView.html?idxno=223339

- The Korea Times: https://www.koreatimes.co.kr/business/companies/20240418/how-will-sk-networks-use-617-million-from-sale-of-car-rental-unit

- DealSite TV: https://news.dealsitetv.com/articles/122578

- SK Speedmate: https://corp.speedmate.com/en

- KED Global: https://www.kedglobal.com/corporate-restructuring/newsView/ked202406180001

- SK Networks Newsroom: https://www.sknetworks.co.kr/en/pr/news-room/B9nzyeKnJUYfDMOG

- Businesskorea: https://www.businesskorea.co.kr/news/articleView.html?idxno=225069

- Maginative: https://www.maginative.com/article/sk-networks-invests-19-million-in-upstage/

- PR Newswire: https://www.prnewswire.com/news-releases/upstage-completes-45m-series-b-bridge-to-accelerate-enterprise-grade-genai-and-global-expansion-302534044.html

- Tech in Asia: https://www.techinasia.com/news/south-koreas-upstage-raises-45m-backed-amazon-amd

- Seoul Economic Daily: https://www.sedaily.com/NewsView/2H0D108VIM

- Namu Wiki Upstage: https://namu.wiki/w/%EC%97%85%EC%8A%A4%ED%85%8C%EC%9D%B4%EC%A7%80

- SK Networks homepage: http://www.sknetworks.co.kr

- VentureSquare: https://www.venturesquare.net/en/1030820/

- DealSite TV: https://dealsitetv.com/articles/158024

- DealSite: https://dealsite.co.kr/articles/147982

- News Tomato: https://www4.newstomato.com/ReadNews.aspx?no=1285188