DEEP RESEARCH · S-OIL

S-OIL Strategy Review: Refining Supercycle and the Shaheen Project

How 2026 refining margins, lower OSP, and Shaheen could drive valuation rerating

0. Bottom line first

I read S-OIL's 2026 setup as the point where lower oil prices, refinery shortages, lower OSP, and Shaheen completion converge. The source argues that the current share price does not fully reflect the possibility of a 2026 refining upcycle or the earnings power of the Shaheen project.

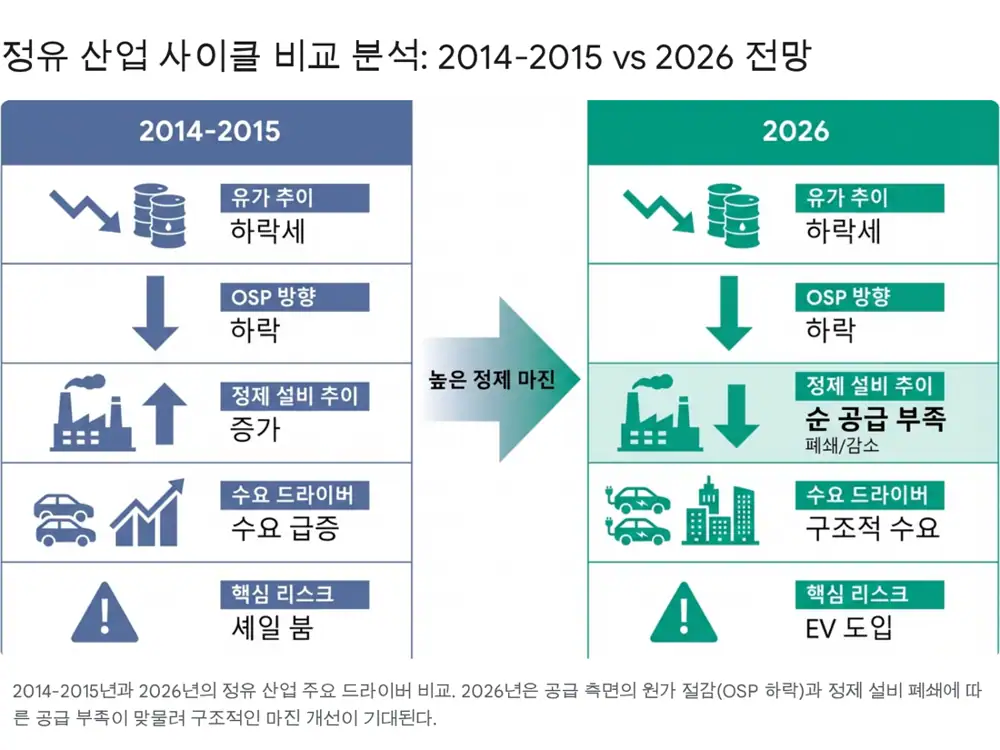

1. The 2014-2015 cycle and the 2026 thesis

The source first dissects the refining boom from late 2014 through 2015. Oil prices fell from around USD 100 per barrel to the USD 40 range, driven by the U.S. shale revolution and OPEC's refusal to cut output. Feedstock costs fell, low prices stimulated miles driven and petroleum-product consumption, and crude prices fell faster than product prices, widening refining margins.

Interpretation: The similarity in 2026 is lower oil prices, but the margin source is different. The 2014-2015 upcycle was demand-pull; the source sees 2026 as a supply-constrained upcycle created by refinery capacity shortages.

| Item | 2014-2015 | 2026 source thesis |

|---|---|---|

| Oil-price background | Shale supply growth and OPEC no-cut policy | More supply from the U.S., Canada, Brazil, Guyana, and possible OPEC+ increases |

| Oil range | From around USD 100 to the USD 40 range | Potential stabilization at USD 60-70 |

| Margin driver | Low oil stimulated demand | Net refinery closures and product tightness |

| Capacity factor | Supply shock centered on crude | About 890 kbd of global refinery capacity closures in 2025-2026, with new additions delayed |

| Demand | Gasoline demand increased | Natural product-demand growth of 0.9-1.0 million b/d could exceed net capacity additions |

Official fact: The source cites closures at major California gasoline refineries, BP Gelsenkirchen in Germany, and PetroChina's Dalian refinery in China, while noting that additions such as Dos Bocas in Mexico and Dangote in Nigeria have faced technical and infrastructure-related ramp-up delays.

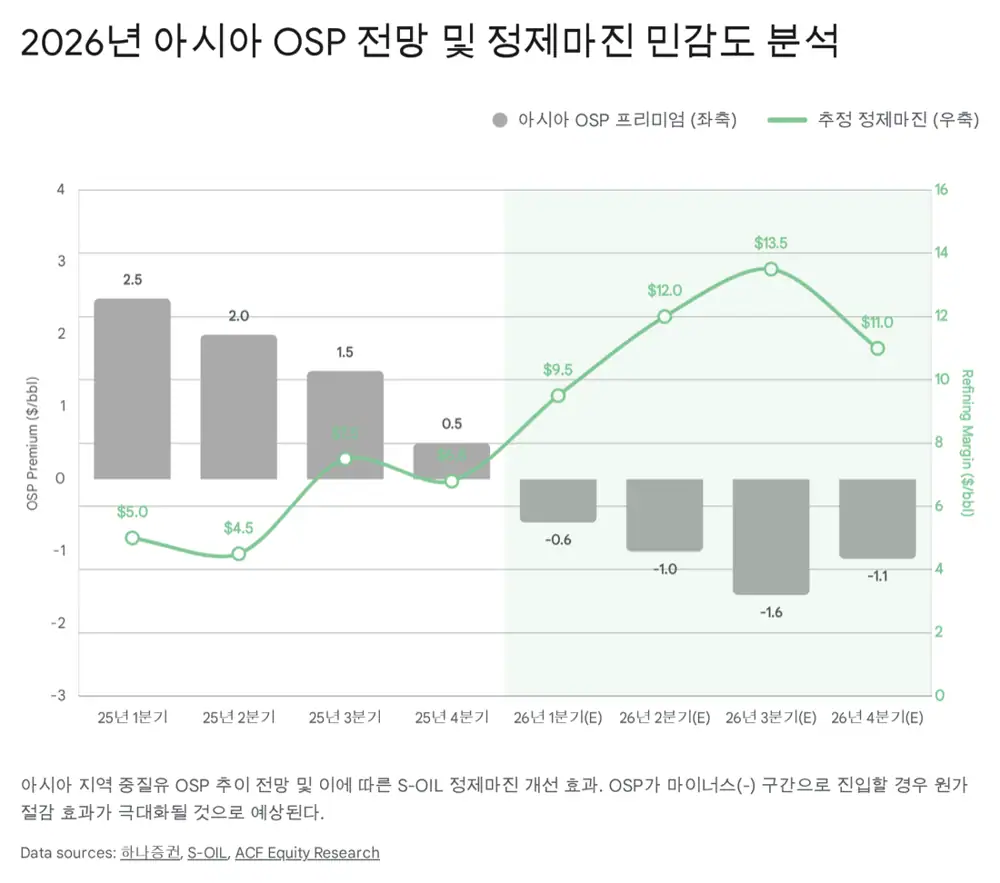

2. Lower OSP: cost leverage for Asian refiners

OSP is the premium or discount Middle Eastern producers add to benchmark crude such as Dubai. Because Saudi Aramco is S-OIL's major shareholder and S-OIL sources crude through long-term Aramco contracts, Asian OSP changes feed directly into cost competitiveness.

Market-share fight

Easing cuts and pushing volume could increase heavy sour crude supply.

TMX pipeline

More Canadian heavy crude exports to Asia could reduce Middle Eastern pricing power.

Extra-heavy recovery

The source mentions possible recovery in Venezuelan production and exports as sanctions ease.

Exports continue

Despite geopolitical uncertainty, Iranian crude exports are described as resilient.

Interpretation: If Asian OSP enters a negative premium zone as cited from Hana Securities, S-OIL could procure crude below the benchmark price. When oil is low and OSP also falls, refining spreads can expand structurally even without a major increase in product prices.

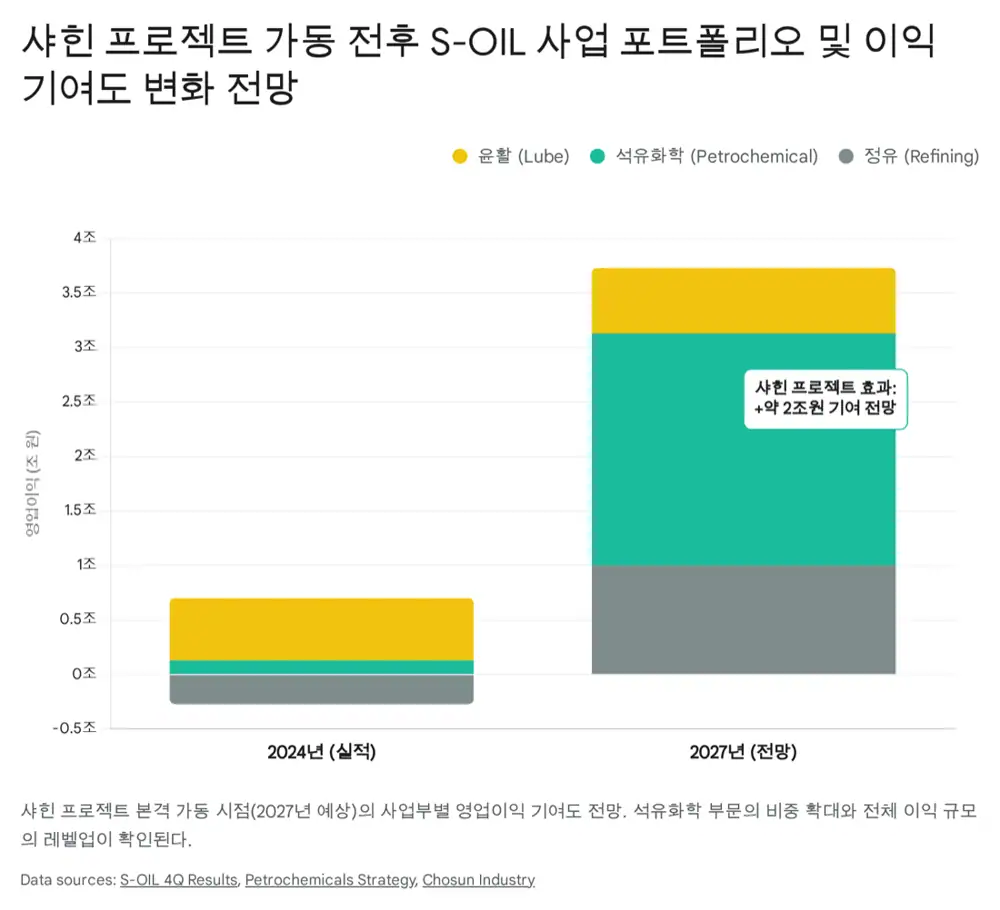

3. Shaheen project: from refiner to integrated chemical player

Official fact: The Shaheen project has total investment of KRW 9.258 trillion. After the final investment decision in November 2022, it has targeted mechanical completion in the first half of 2026. The source says progress reached 93.1% as of January 14, 2025.

| Item | Source detail | Meaning |

|---|---|---|

| Technology | TC2C, Thermal Crude to Chemicals | Direct conversion of crude and low-value heavy oil into chemical feedstock |

| Developers | Saudi Aramco and Lummus Technology | First commercial deployment is the differentiator |

| Chemical yield | From 12% to 25% | Diversifies earnings away from refining |

| Ethylene BEP | Estimated USD 171 per ton | About 30% lower than the NCC average of USD 250 per ton |

| Operating-profit contribution | Up to KRW 2 trillion annually at normal operation | A single project could double earnings power |

Shaheen is planned to produce 1.8 million tons of ethylene, 770,000 tons of propylene, 200,000 tons of butadiene, and 280,000 tons of benzene annually, plus higher-value polymers such as 440,000 tons of HDPE and 880,000 tons of LLDPE. The source expects the financial statements to change qualitatively once annual operation stabilizes in 2027.

Interpretation: The real meaning is lower earnings volatility. Refining is exposed to oil and margins, but Shaheen raises the chemical share and diversifies the portfolio. After completion, CAPEX should also fall; the source cites IBK Investment Securities as expecting 2026 and 2027 CAPEX to decline to 47% and 11% of the 2025 level, respectively.

4. 4Q25 earnings and 2026 guidance

Official fact: S-OIL reported 4Q25 revenue of KRW 8.7926 trillion and operating profit of KRW 424.5 billion. Operating profit rose 85.2% quarter over quarter and 90.9% year over year, beating the KRW 381.3 billion consensus by about 11%.

| Segment | 4Q25 source number | Key read |

|---|---|---|

| Refining | Operating profit KRW 225.3 billion, roughly double the prior quarter's KRW 115.5 billion | Underlying refining-margin recovery offset inventory losses of KRW -87.0 billion and negative lagging effect of KRW -80.0 billion |

| Petrochemicals | Operating loss KRW -7.8 billion | Loss narrowed from KRW -19.9 billion QoQ and KRW -35.6 billion YoY, helped by PX spreads |

| Lube base oil | Operating profit KRW 207.0 billion, QoQ +55%, OPM 27.3% | A high-margin segment that benefits when feedstock prices fall |

S-OIL management guided to a favorable 2026 environment in which global oil demand growth exceeds net capacity additions and lower oil and OSP reduce cost pressure. Hana Securities raised its 2026 operating-profit estimate from KRW 2.0 trillion to KRW 2.3 trillion, 65% above the KRW 1.4 trillion market consensus cited in the source.

The source also presents a 1Q26 operating-profit forecast of KRW 587.7 billion, implying a year-over-year swing to profit and 38% growth from the prior quarter. The backdrop is oil stabilizing near USD 62, an OSP reduction effect of USD -1.9 per barrel quarter over quarter, and improved PX/benzene margins.

5. Valuation and investment strategy

The source gives 2026E PER of 8.36x and PBR of 1.16x. Compared with PBR of 1.5-2.0x in past refining upcycles, it argues the current share price does not fully reflect the 2026 cycle and Shaheen potential.

| Item | Source number | Meaning |

|---|---|---|

| Current share price | About KRW 98,300 as of January 26, 2026 | Starting point for the valuation bridge |

| Target price | KRW 130,000 | Reflects refining margin, OSP, and Shaheen premium |

| 2026 DPS | KRW 2,750 estimate | Up from the 2025E DPS of KRW 1,750 |

| Risks | Oil below USD 50, China slowdown, Shaheen delay | The source views delay risk as limited because progress is around 93% |

Valuation bridge

- Refining margins recover in 1H26 as refinery closures meet driving-season demand.

- Asian OSP enters a negative zone or falls sharply, confirming real cost improvement.

- Shaheen completion and trial operation in 2H26, plus 2027 commercial operation expectations, expand the petrochemical multiple.

The source presents S-OIL as a 2026 Top Pick within energy and chemicals, citing a refining-margin supercycle from global capacity closures and lower OSP, 2026 Shaheen completion momentum, and PX/BTX strength from the end of China's expansion cycle and solid gasoline demand.

Interpretation: My key watchpoint is whether S-OIL can move beyond being a refining-cycle beneficiary and earn recognition as an integrated energy-chemical company with a low-cost chemical portfolio through Shaheen.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224164487141

- Reference 1: S-Oil's 9.258 Trillion Won Shaheen Project to Boost Petrochemical Competitiveness

- Reference 2: S-Oil (010950)

- Reference 3: Down the Slide: The collapse in oil prices since 2014

- Reference 4: What triggered the oil price plunge of 2014-2016

- Reference 5: Outlook 2026: The next oil shock

- Reference 6: Why are Gasoline and Diesel Prices So High?

- Reference 7: How are low prices affecting the oil industry?

- Reference 8: Oil 2025 executive summary

- Reference 9: Oil 2025: Analysis and forecast to 2030

- Reference 10: Refinery status monthly - September

- Reference 11: Oil Market Report - January 2026

- Reference 12: Refinery closures and rising consumption will reduce U.S. petroleum inventories in 2026

- Reference 13: S-Oil logs profit drop but sees favorable Korea market outlook in 2026

- Reference 14: TC2C Thermal Crude to Chemicals Technology

- Reference 15: Aramco affiliate S-OIL to build one of the world's largest petrochemical crackers in South Korea

- Reference 16: S-OIL to Invest $7 billion in Ulsan

- Reference 17: S-Oil's Shaheen Project Boosts Ethylene Competitiveness by 30%

- Reference 18: Petrochemicals: Beyond Restructuring Strategy PDF

- Reference 19: S-Oil IBK report PDF

- Reference 20: 2026 Outlook--China Commodities Watch