DEEP RESEARCH · TY Holdings

TY Holdings restructuring analysis: what remains after the Ecobit sale

A breakdown of the Ecobit proceeds waterfall, KKR settlement, Taeyoung E&C workout, and remaining PF risk

0. Bottom line first

My view is that TY Holdings reduced chain-default risk through the Ecobit sale, but lost its core cash generator and became more dependent on Taeyoung E&C normalization, SBS, and leisure assets.

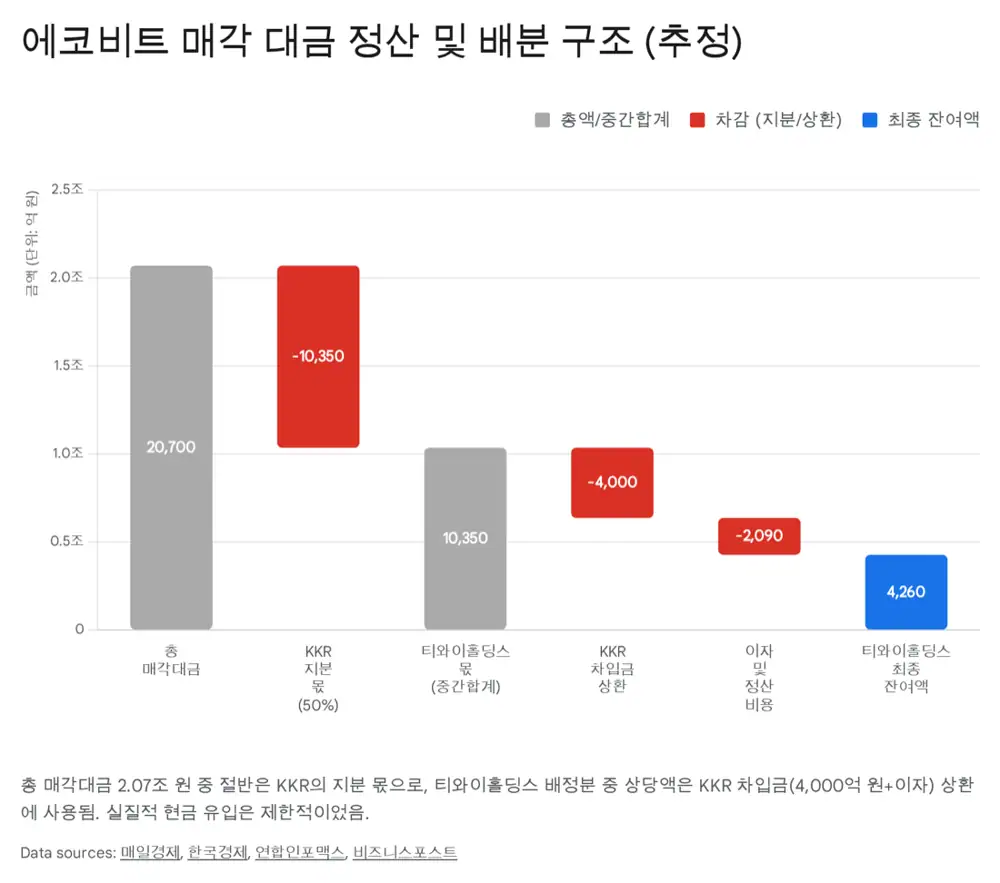

Official fact: The source says 100% of Ecobit was sold to an IMM consortium for KRW 2.07tn, with TY Holdings and KKR each previously owning 50%.

Interpretation: The deal size was large, but KKR's equity share, KRW 400bn private bond principal, roughly 13% interest, and settlement waterfall came out first. Cash left at TY Holdings was limited. This was a survival transaction for workout compliance, not growth capital.

KRW 2.07tn

The sale price for 100% of Ecobit.

9.2x EV/EBITDA

The source calculates this on 2023 EBITDA of KRW 225bn.

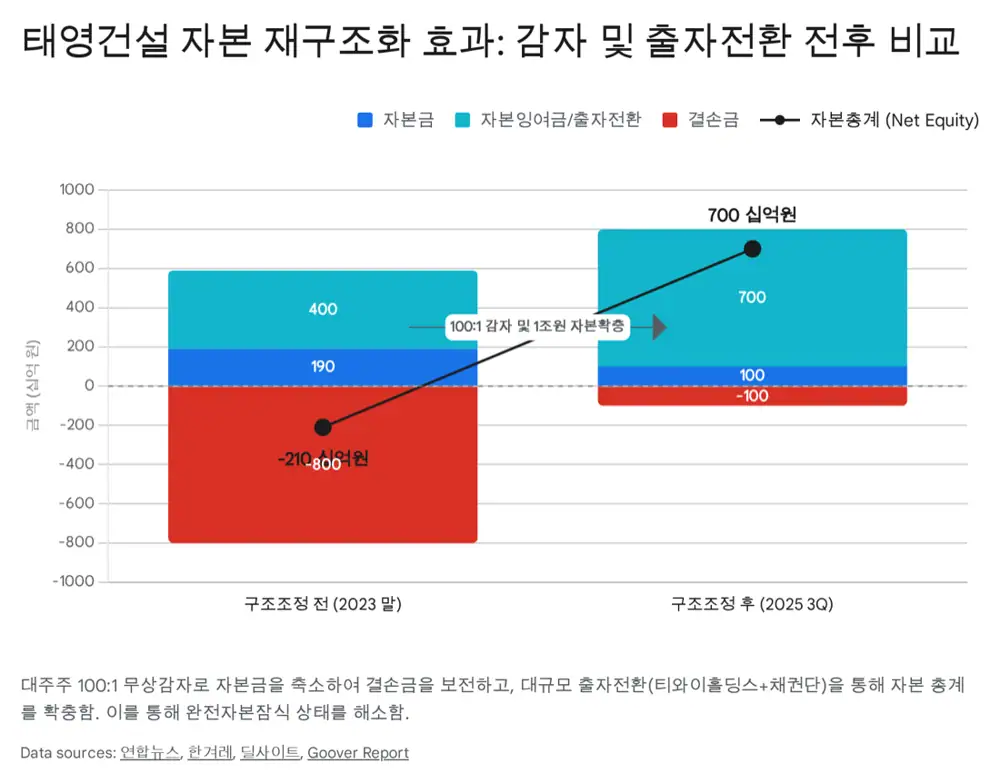

100:1 reduction

Major shareholder shares were reduced 100:1; minority shares were reduced 2:1.

1. Company profile and 3Q25 financial position

TY Holdings was established on September 1, 2020 through the spin-off of the former Taeyoung E&C. It managed construction, environment, broadcasting, and leisure businesses, but its portfolio shrank sharply during restructuring after the sale of Taeyoung Industry and Ecobit.

| Item | 3Q25 source number | Meaning |

|---|---|---|

| Total assets | KRW 1.6606tn, -7.8% from prior year-end | Impact of core asset sales |

| Total liabilities | KRW 748.8bn, -6.1% | Debt repayment using sale proceeds |

| Total equity | KRW 911.8bn, -9.2% | Widening accumulated deficit |

| Revenue | KRW 55.6bn, YoY -4.8% | Smaller scale after Ecobit exit |

| Operating loss | KRW -3.3bn | Improved from KRW -69.4bn a year earlier |

| Net loss | KRW -51.6bn | Financial-cost burden including KRW 27.0bn interest expense |

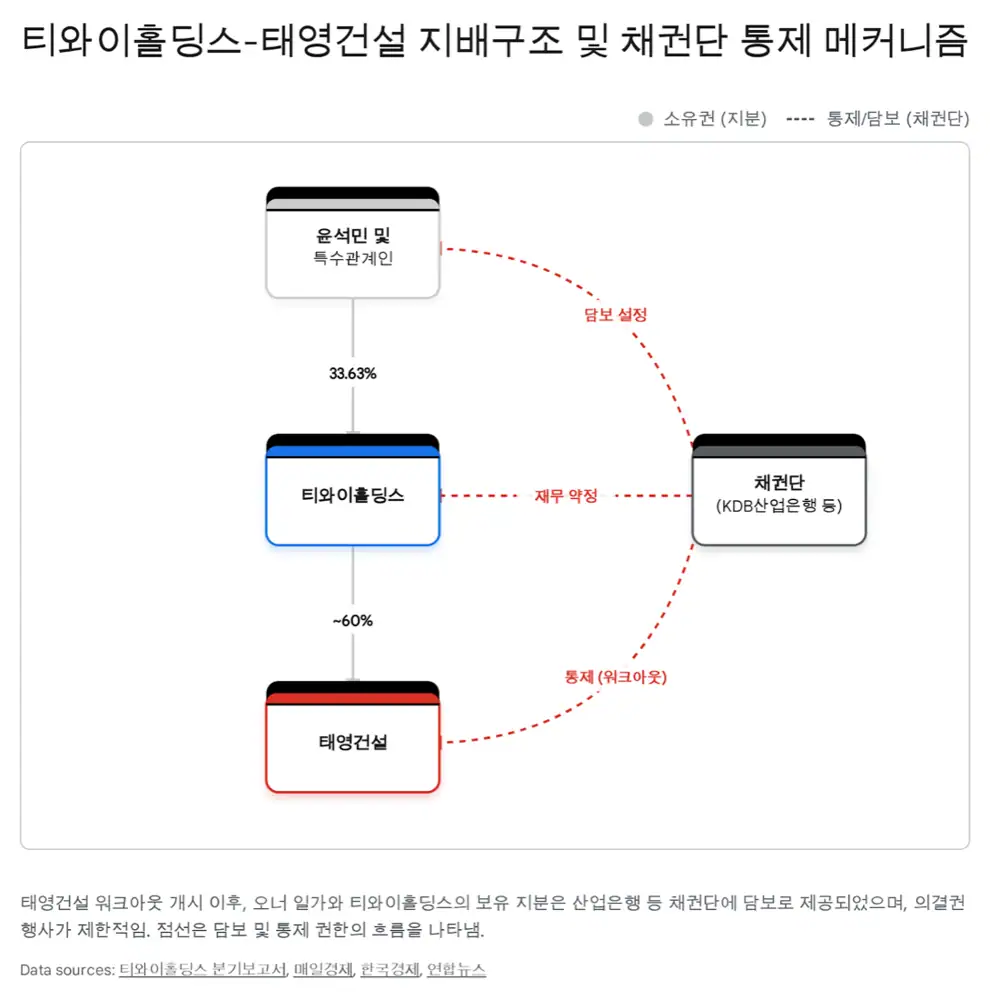

Official fact: The source states that Chairman Yoon Suk-min held 25.44% as of 3Q25 and estimates related-party ownership at about 33.63% including the Seoyam Yoon Se-young Foundation's 5.43% and founder-related stakes. Major stakes were pledged to creditors, and Taeyoung E&C voting rights were delegated to creditors during workout.

2. Ecobit sale: the waterfall matters more than the headline price

Ecobit is a major Korean environmental company spanning landfill, incineration, and water treatment. The source cites 2023 revenue of KRW 699.6bn and EBITDA of KRW 225.0bn, implying about 9.2x EV/EBITDA at the KRW 2.07tn sale price. This was below earlier market talk of KRW 2.5-3.0tn or 11-13x, reflecting the higher-rate M&A market and Taeyoung's distressed-seller position.

Interpretation: For KKR, collateral and senior settlement terms worked as intended. For TY Holdings, the company sold a prime environmental asset but did not materially rebuild holding-company strength.

3. Taeyoung E&C workout: capital reduction and debt-equity swap

Taeyoung E&C applied for workout on December 28, 2023. The workout began in January 2024, and the company signed an MOU with creditors on May 30, 2024. The lead creditor bank is KDB.

| Self-rescue measure | Source execution status | Meaning |

|---|---|---|

| Taeyoung Industry | Sale completed | Initial liquidity secured |

| Ecobit | Sale completed | Core workout condition fulfilled |

| BlueOne country clubs | Yongin and Sangju CC securitization and sale | Leisure assets converted into cash |

| Pyeongtaek Silo | Stake pledged | Creditor protection |

| Capital restructuring | Major shareholders 100:1, minority 2:1 reduction | Existing shareholders absorbed responsibility |

| Debt-equity swap | TY Holdings about KRW 400bn, creditors about KRW 300bn | Capital impairment relief and leverage improvement |

After the capital reduction and debt-equity swap, TY Holdings' Taeyoung E&C stake rose from about 27.8% to around 60%, but that stake was pledged to creditors, limiting actual control.

4. Remaining PF risk: contingent liabilities by number

The source uses 3Q25 report notes to frame PF funding-support and debt-assumption agreements related to Taeyoung E&C as the key risk.

| Project | Source commitment size | Risk point |

|---|---|---|

| Gimhae Daedong advanced industrial complex | KRW 280.0bn | Large regional funding-support commitment |

| Magok CP4 | KRW 359.2bn | Large Seoul office/commercial development |

| Changwon self-sufficient administrative town | KRW 183.6bn | Need to track regional sales rate and main PF transition |

| Gumi Flower Garden | KRW 90.0bn | Sensitive to regional housing market |

| Others | Ecocity KRW 51.1bn, Mukdong youth housing KRW 36.5bn, Sangbong youth housing KRW 20.0bn | Multiple completion and funding-support commitments |

Interpretation: Risk has eased in some large projects such as Magok CP4 through completion or main PF transition, but weak regional project sales could bring TY Holdings' additional cash burden back into focus.

5. TY Holdings after the sale: what supports the holding company?

Ecobit exit

The environmental segment that contributed roughly KRW 700-800bn revenue and more than KRW 200bn EBITDA per year is gone.

SBS dependence

Broadcast advertising cyclicality and production-cost pressure matter more now.

BlueOne

Remaining leisure assets are economically sensitive and hard to treat as stable cash flow.

On the positive side, the source says Taeyoung E&C resumed trading seven months after receiving an unqualified audit opinion and resolving capital impairment. It also secured more than KRW 800bn of new orders in 2025, mainly in public works and civil engineering. With leverage lowered into the 200% range, the source cautiously discusses possible early workout graduation in late 2025 or early 2026.

The investment point is not the Ecobit sale itself, but the gap left after it. Taeyoung E&C PF projects, SBS turnaround, and collateral enforcement risk need to be checked every quarter.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224159750193

- Hankyung IMM Ecobit acquisition: https://www.hankyung.com/article/2024082667941

- Edaily MarketIn Ecobit closing: https://marketin.edaily.co.kr/News/Read?newsId=02374726639118192

- NewsTomato TY Ecobit sale: https://www.newstomato.com/ReadNews.aspx?no=1238821

- Hankyung Ecobit proceeds: https://www.hankyung.com/amp/202412134053r

- Yonhap Infomax KKR proceeds: https://news.einfomax.co.kr/news/articleView.html?idxno=4336165

- Yonhap Taeyoung stake: https://www.yna.co.kr/view/AKR20240416118151002

- Hani workout capital reduction: https://www.hani.co.kr/arti/economy/economy_general/1136853.html

- Yonhap Infomax IMM Ecobit completion: https://news.einfomax.co.kr/news/articleView.html?idxno=4336161

- Invest Chosun Ecobit deal: https://www.investchosun.com/site/data/html_dir/2024/12/13/2024121380032.html

- Ecobit annual report PDF: http://www.ecorbit.com/assets/file/[%EC%97%90%EC%BD%94%EB%B9%84%ED%8A%B8]%EC%82%AC%EC%97%85%EB%B3%B4%EA%B3%A0%EC%84%9C(2023.03.31).pdf

- Daum waste market competition: https://v.daum.net/v/GXYpah1iy9

- Invest Chosun KKR collateral: https://www.investchosun.com/site/data/html_dir/2024/01/08/2024010880186.html

- Hankyung Taeyoung funding: https://www.hankyung.com/article/2024082667831

- DealSite Ecobit completion: https://dealsite.co.kr/articles/133350/075033

- Edaily MarketIn K-Eco bolt-on: https://marketin.edaily.co.kr/News/Read?newsId=04260726642399832

- Research Nester waste management market: https://www.researchnester.com/kr/reports/waste-management-market/6028

- The Economy SBS discussion: https://kr.economy.ac/news/2024/01/2024011686

- DealSite TV capital expansion: https://dealsitetv.com/articles/114876

- Korea Economic TV YouTube: https://www.youtube.com/watch?v=R2kuCQLIWC4

- DealSite TV construction ranking: https://news.dealsitetv.com/articles/157572

- Maeil Business Taeyoung owner issue: https://www.mk.co.kr/news/economy/10913869

- DealSite workout plan: https://dealsite.co.kr/articles/121280/068032

- Business Post Ecobit stake sale: https://www.businesspost.co.kr/BP?command=article_view&num=363557

- Hankyung Ecobit remaining cash: https://www.hankyung.com/article/2024121689041

- KPMG waste recycling report: https://assets.kpmg.com/content/dam/kpmgsites/kr/pdf/2025/eri/issue_monitor/kpmg-%EC%82%BC%EC%A0%95KPMG-%EB%8B%A4%EC%8B%9C-%EB%B6%88%EC%96%B4%EC%98%AC-%ED%8F%90%EA%B8%B0%EB%AC%BC-%EC%97%B4%ED%92%8D-%ED%8F%90%ED%94%8C%EB%9D%BC%EC%8A%A4%ED%8B%B1-%EC%9E%AC%ED%99%9C%EC%9A%A9%EC%9D%84-%EC%A4%91%EC%8B%AC%EC%9C%BC%EB%A1%9C-202502.pdf.coredownload.inline.pdf

- Mordor industrial waste management market: https://www.mordorintelligence.kr/industry-reports/industrial-waste-management-market