DEEP RESEARCH · Kakao Pay/Digital Asset Act

Kakao Pay: Digital Asset Act Delay and Exchange Ownership-Cap Risk

A review of the 15-20% exchange ownership cap, stablecoin debate, and Alipay overhang

0. Bottom line first

The Kakao Pay thesis now sits between a real operating turnaround, shown by record quarterly operating profit of KRW 15.8 billion in Q3 2025, and regulatory variables around Dunamu, stablecoins, and Alipay supply. I read this less as a single negative headline and more as a regime change in Korean digital finance.

- Financial authorities were reported to be considering a 15-20% cap on major shareholders of virtual-asset exchanges.

- The source describes Dunamu's domestic market share as above 80%.

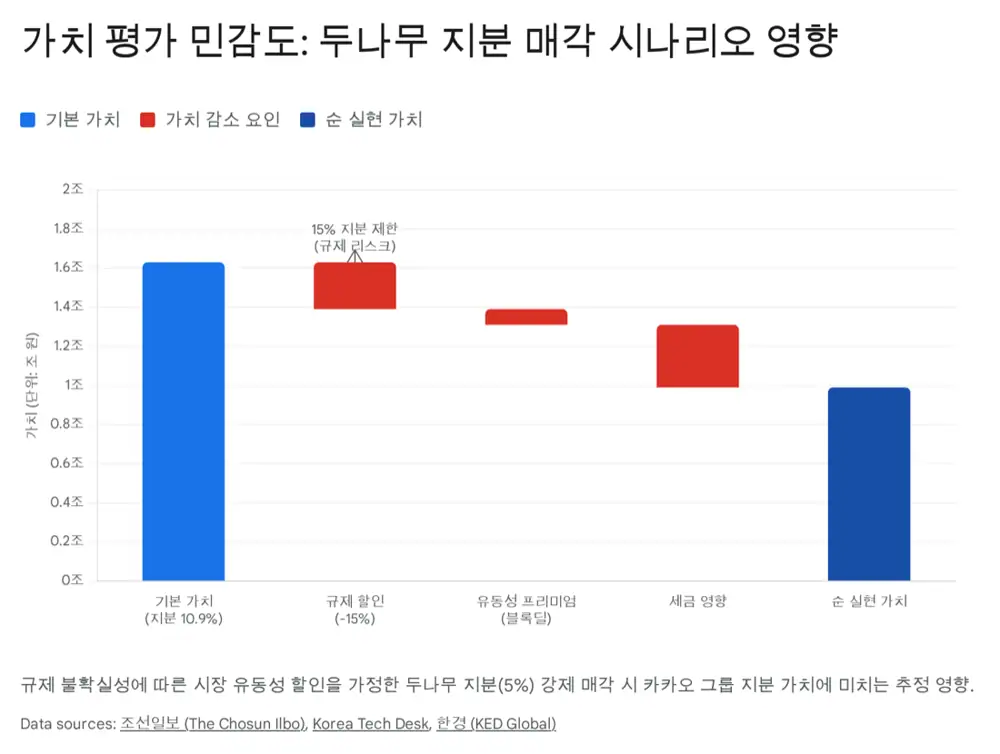

- Kakao Group's Dunamu stake is estimated at about 10.6-10.9%; whether related-party holdings are aggregated is the key question.

- Dunamu chairman Song Chi-hyung's stake is cited at about 25.5%; if a 15% rule applies, more than 10%, or roughly KRW 1.2 trillion, could become a sale burden.

1. Structure of the Regulatory Pivot

Official fact: The source cites a January 23, 2026 Korea Economic Daily report and frames the 15-20% exchange ownership cap and the delayed Digital Asset Basic Act as the central events.

Interpretation: Kakao Pay faces a regulatory squeeze: upside from new businesses is delayed while downside governance regulation accelerates. The longer ICOs, corporate accounts, and stablecoin rules are postponed, the more the expected multiple can be compressed.

2. The Dunamu Stake Dilemma

The Dunamu stake has acted as option value inside Kakao Pay and Kakao Group valuation. But if forced-sale risk rises, the same asset becomes a two-sided issue: liquidity event on one side, loss of growth engine on the other.

Liquidity event

If Dunamu is valued at KRW 12-16 trillion, a stake sale could fund new M&A or shareholder returns.

Loss of growth engine

An involuntary sale could mean a discount to fair value and lower equity-method profit.

Related-party aggregation

Even if one legal entity is below 15%, Kakao's burden rises if group holdings are aggregated.

3. The Stablecoin War

The source interprets banks' lobbying for exclusive rights around interest-bearing stablecoins as a direct threat to Kakao Pay's Super Wallet strategy. Kakao Pay has strong payment UX and platform distribution, but if banks alone capture interest features, user incentives weaken.

Interpretation: Kakao Pay's defensive pivot is to move away from stablecoin interest competition and toward STO plus non-interest payment speed and convenience. KakaoTalk distribution remains an asset banks cannot easily copy.

4. Core Profit and Financial-Income Dependence

In Q3 2025, Kakao Pay turned profitable with record quarterly operating profit of KRW 15.8 billion. The source still separates the quality of core operations from reliance on financial income. The key question is whether payments and financial services alone can justify valuation, and how vulnerable profitability is to lower rates or fund outflows.

5. Scenario View

| Scenario | Probability | Trigger | Impact on Kakao Pay |

|---|---|---|---|

| Hard landing | Medium, 40% | 15% cap enforced; banks monopolize stablecoin interest | Forced Dunamu sale, SOTP damage, weaker Super Wallet strategy |

| Soft compromise | High, 50% | Grace period and fintech interest-sharing allowed | Regulatory uncertainty eases; strategy shifts to STO and non-interest payments |

| Tech victory | Low, 10% | Political check on bank monopoly; U.S.-style no-interest model | Fairer competition; Kakao UX advantage stands out |

6. Strategic Suggestions

- Focus on STO market leadership in case the stablecoin interest path is blocked.

- Resolve the Dunamu stake issue before legislation is finalized. Spin-offs or in-kind distributions may be better than forced selling.

- Monitor Alipay-related stock lending and short-selling data after the January 14 share recall.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157850461

- Source 2: https://blog.naver.com/star_of_self/224153680263

- Source 3: https://koreatechdesk.com/korea-crypto-governance-reform-ownership-cap-digital-asset-act

- Source 4: https://www.chosun.com/english/market-money-en/2026/01/06/RFG7WWHZCBAOLDYYEUCV622E6I/

- Source 5: https://www.kedglobal.com/mergers-acquisitions/newsView/ked202509290009

- Source 6: https://koreatechdesk.com/korea-next-fintech-pivot-naver-dunamu-merger-stablecoin-policy-global-expansion

- Source 7: https://www.mk.co.kr/en/economy/11504950

- Source 8: https://biz.chosun.com/en/en-finance/2025/09/03/AV37V7XVPBAMBISUGY5Z4WI7KY/

- Source 9: https://www.mk.co.kr/en/stock/11409704

- Source 10: https://www.koreatimes.co.kr/economy?page=135

- Source 11: https://www.koreatimes.co.kr/economy/20240813/kakao-pay-handed-over-40-mil-users-data-to-alipay-without-consent-fss

- Source 12: https://coinnews.com/news/kakao-and-naver-deepen-stablecoin-plans-as-korea-advances-digital-asset-rules/