DEEP RESEARCH · JC CHEMICAL

JC Chemical Deep Dive: Integrated Bioenergy and the SAF Feedstock Cycle

Testing whether biodiesel, PTU, and palm plantations can drive a 2026 turnaround

0. Bottom line first

I see JC Chemical's core as an integrated bioenergy value chain spanning feedstock, manufacturing, and sales. The 3Q25 net loss was driven largely by non-operating items such as FX losses; the 2026 thesis is full-year PTU revenue contribution, CPO price leverage, and preparation for SAF mandates.

~784k kL

Biofuel production capacity at the Onsan and Ulsan New Port plants.

81.2% / 18.8%

9M25 revenue split between biofuels and palm plantation.

0.46x P/B

The source argues the share price does not fully reflect asset value or growth potential.

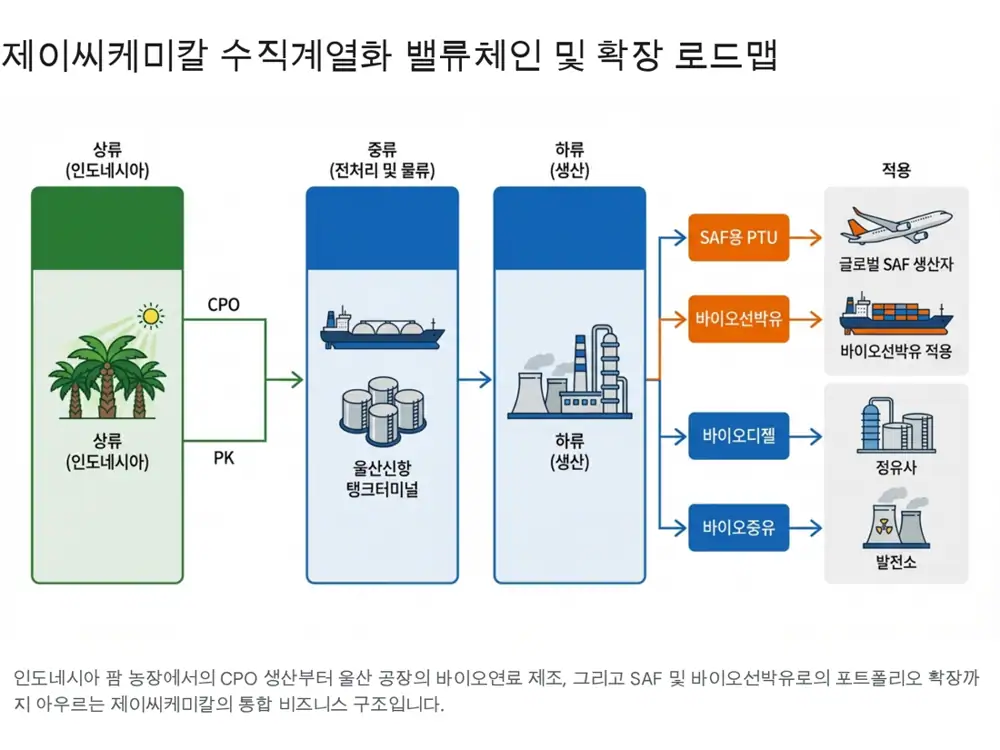

Official fact: JC Chemical has manufactured and sold biodiesel (BD100), bio-heavy oil, and related renewable fuels since its 2006 founding. The source describes it as the only Korean biofuel company with both upstream palm feedstock and downstream manufacturing/sales.

Interpretation: The investment question is whether the market starts valuing the company as an SAF feedstock supplier rather than just a biodiesel producer. The risks are equally clear: palm oil prices, FX, and the pace of policy mandates matter a lot.

1. Company structure: refining technology plus palm assets

JC Chemical produces biodiesel, bio-heavy oil, and PTU from its Onsan and Ulsan New Port plants. The source says the company secured high yields with a continuous process designed in-house in 2007 and has refining technology to remove impurities and control free fatty acids in lower-cost feedstocks such as used cooking oil and animal fats.

2. Segments: biofuels and palm plantation

Biofuels accounted for 81.2% of 9M25 revenue. Key products are biodiesel blended into transport diesel and bio-heavy oil replacing bunker-C fuel at power plants. Since 4Q24, the company has supplied PTU to global refiners and energy companies after converting Ulsan New Port equipment, according to the source.

Palm plantation accounted for 18.8% of revenue. Plantations in East Kalimantan and subsidiaries such as PT. Niagamas Gemilang produce CPO and palm kernel. After completing the CPO mill in 2016, the company doubled FFB processing capacity from 30 tons to 60 tons per hour at the end of 2022, and acquired 99.99% of PT. Puncak Panglima Perkasa in February 2024.

| Axis | Core content | Investment meaning |

|---|---|---|

| Biofuels | BD100, bio-heavy oil, PTU, bio-marine fuel | Potential beneficiary of RFS and SAF mandates |

| Refining technology | Pretreatment of UCO and animal fats | Margin defense when feedstock prices move |

| Palm plantation | East Kalimantan CPO and PK production | Profit leverage when CPO prices rise |

| Global bases | Singapore and Malaysia subsidiaries | Feedstock sourcing and PTU/SAF supply-chain expansion |

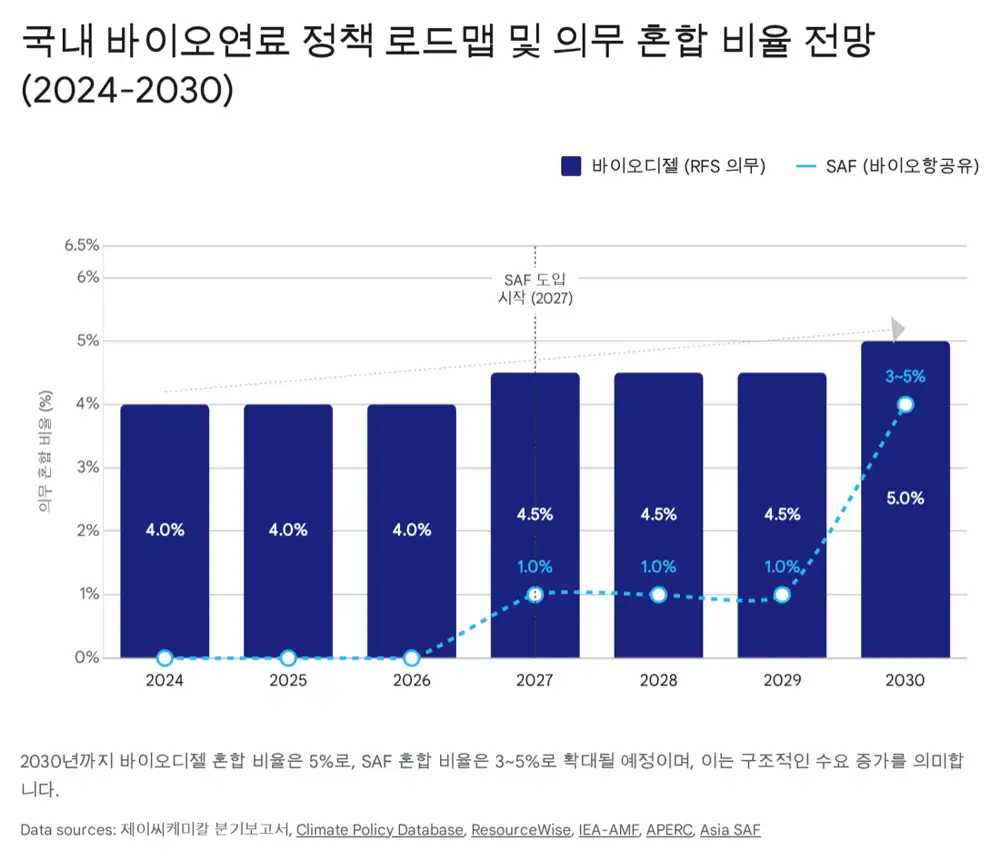

3. Policy demand: RFS, SAF, and Indonesia B40/B50

Korea's biodiesel market is determined by the RFS blending mandate. The required blend ratio rose from 3.5% in 2021 to 4.0% from 2024, with the current roadmap pointing to 5.0% by 2030. The source also mentions scenarios discussing up to 8.0% if next-generation biodiesel such as HVO is introduced.

Korea consumed about 127 million barrels of transport diesel in 2024. According to the source, each 0.5 percentage-point increase in the blend ratio creates roughly 100,000-150,000 kL of new annual biodiesel demand.

SAF is the larger option. The source says Korea will mandate 1% SAF blending for all international flights departing Korean airports from 2027, with the ratio expected to rise to 3-5% by 2030 and above 10% by 2035.

4.0% → 5.0%

4.0% in 2024 and 5.0% by 2030 under the roadmap.

1% in 2027

The international-flight mandate is the policy base for PTU demand.

B40/B50

B40 began in 2025; B50 could absorb an additional 3-5 million tons of CPO, according to the source's cited estimates.

Interpretation: SAF production technology is not the main bottleneck; feedstock is. The re-rating point is JC Chemical's ability to pretreat UCO and palm byproducts into PTU usable for SAF.

4. Earnings: 2025 growing pains and 2026 turnaround

9M25 consolidated revenue was KRW 281.3 billion, operating profit was KRW 8.1 billion, and net loss was KRW 1.4 billion. The surface numbers look weak, but the palm plantation segment increased its profit contribution.

| Item | 9M24 | 9M25 | Change | Note |

|---|---|---|---|---|

| Total revenue | KRW 367,320M | KRW 281,304M | -23.4% | Lower ASP and volume adjustment |

| Total operating profit | KRW 10,689M | KRW 8,097M | -24.2% | Biofuel margin squeeze |

| Biofuel operating profit | KRW 2,408M | KRW 2,121M | -11.9% | Spread compression |

| Palm plantation operating profit | KRW 4,200M | KRW 5,977M | +42.3% | CPO price strength and yield improvement |

| Total net income | KRW 5,647M | -KRW 1,426M | Turned loss-making | FX losses and other non-operating costs |

The source interprets the net loss as being driven more by non-operating expenses, especially FX translation losses on USD liabilities for Indonesian operations and feedstock imports, than by core operating deterioration. Because the loss is accounting-based, it can reverse if FX stabilizes.

5. Balance sheet and capital allocation

At end-3Q25, total liabilities were KRW 214.6 billion, equity was KRW 153.9 billion, and the debt ratio was about 139.4%. Current assets were KRW 155.4 billion, current liabilities KRW 163.8 billion, and the current ratio about 94.8%. Cash and equivalents were about KRW 46.5 billion, and inventory was KRW 60.2 billion.

Capital allocation is growth-focused. The source highlights PTU equipment conversion and expansion at Ulsan New Port, the February 2024 acquisition of PT. PPP, and full ownership of EasyGreenB to improve execution speed. The dividend may defend or modestly adjust around the prior DPS level of roughly KRW 150, but the main point is growth after 2026.

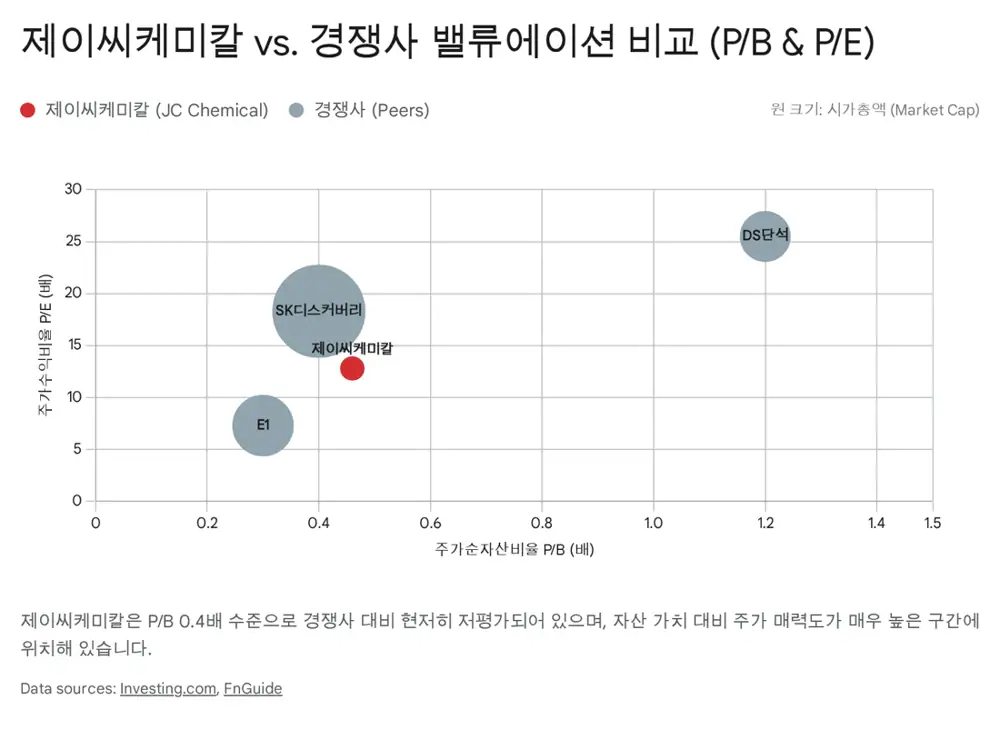

6. Valuation and checkpoints

The source cites JC Chemical's P/B at about 0.46x and argues that the book value of the Indonesian palm plantation land may be below market value. DS Dansuk trades above 1.2x P/B on SAF momentum, while JC Chemical has a similar biofuel and SAF feedstock portfolio plus its own upstream palm plantation.

Key monitoring points

- How quickly PTU exports expand from 2026 and whether new customers are secured.

- The pace of Indonesia's B50 implementation and persistence of CPO price strength.

- Timing of FX stabilization and interest-cost relief feeding into non-operating income.

The source presents a strong medium-term buy approach. I would narrow that into a more cautious thesis: watch for confirmation of SAF feedstock revenue before assuming a full re-rating.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157849807

- 데일리인베스트: 제이씨케미칼 분석: http://www.dailyinvest.kr/news/articleView.html?idxno=69853

- KRX KIND: 제이씨케미칼 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250312001795&rcpno=20250312001076&orgid=F&tran=Y&langTpCd=0

- Climate Policy Database: Renewable Fuel Standard: https://climatepolicydatabase.org/policies/renewable-fuel-standard-2015-2030

- APERC: Biofuels and SAF in Korea PDF: https://aperc.or.jp/presentations/apec_energy_transition_symposium_series/file/phase2_01/S2-3_Dr_Hyunyoung_Oh.pdf

- ResourceWise: South Korea SAF roadmap: https://www.resourcewise.com/blog/south-korea-charts-its-saf-future-with-promising-new-mandate-roadmap

- ASAFA: Korea SAF mandate: https://www.asiasaf.org/post/korea-unveils-saf-mandate-to-drive-aviation-decarbonisation

- SAF Investor: JC Chemical Malaysia facility: https://www.safinvestor.com/news/148938/malaysia-3/

- SAF Investor: DS Dansuk feedstock: https://www.safinvestor.com/news/146758/ds-dansuk/

- Fastmarkets: Palm oil 2026 outlook: https://www.fastmarkets.com/insights/palm-oil-price-forecast-and-production-outlook-2026/

- Biofuels International: Indonesia B50: https://biofuels-news.com/news/indonesia-plans-full-rollout-of-b50-in-the-new-year/

- Business Indonesia: B40 mandate: https://business-indonesia.org/news/indonesia-to-maintain-b40-biodiesel-mandate-as-palm-oil-prices-rise

- UKR AgroConsult: B50 demand impact: https://ukragroconsult.com/en/news/indonesias-b50-biofuel-mandate-could-boost-palm-oil-demand-by-3m-tonnes/

- Trading Economics: Palm oil: https://tradingeconomics.com/commodity/palm-oil

- UKR AgroConsult: palm oil supply-demand: https://ukragroconsult.com/en/news/palm-oil-supply-and-demand-is-shrinking-price-expectations-are-rising/

- Trading Economics Korea: palm oil: https://ko.tradingeconomics.com/commodity/palm-oil

- ESMA: JC 2025 risk report PDF: https://www.esma.europa.eu/sites/default/files/2025-09/JC_2025_48__JC_Autumn_2025_risk_report.pdf

- 인포스탁데일리: 글로벌 바이오연료 수혜: https://www.infostockdaily.co.kr/news/articleView.html?idxno=201357

- Investing.com: JC Chemical financials: https://www.investing.com/equities/jc-chemical-corp-ltd-financial-summary