DEEP RESEARCH · Elcomtec (037950.KQ)

Elcomtec — an 80% capital reduction designed to manufacture dividend capacity, not heal losses

Partron capital repatriation + a free Mongolian mining call option in an event-driven name

0. Bottom line first

Elcomtec’s Jan 16, 2026 decision to execute an 80% capital reduction (5-for-1 consolidation) looks nothing like a typical ‘heal-the-deficit’ reduction. The balance sheet is pristine — debt ratio 7.7%, current ratio 535%, retained earnings KRW 17.1B — there is no deficit to heal. The real purpose is to shrink paid-in capital so the 1.5× legal-reserve threshold drops, unlocking distributable reserves; the beneficiary will likely be parent Partron (57.3% stake) repatriating cash. On top of that, the Mongolian subsidiary AGM MINING (54.86% stake) sits on the books at zero — effectively a free call option on a gold/copper supercycle.

1. Macro — gold returns, copper joins

The 2026 Fed cutting cycle is lowering real rates → reducing the cost of carry for gold and structurally bidding it up. Geopolitical risk and central-bank de-dollarisation purchases hold the floor. Historically Elcomtec’s beta to gold futures expands above 1.5 in volatile regimes — the market treats it as a leveraged gold proxy.

Copper is being labelled ‘the new oil of decarbonization’ on EV / renewables / data-center electrification demand. Elcomtec’s Mongolian licences sit in Umnugobi, on the same geological belt as the world-class Oyu Tolgoi Cu-Au mine.

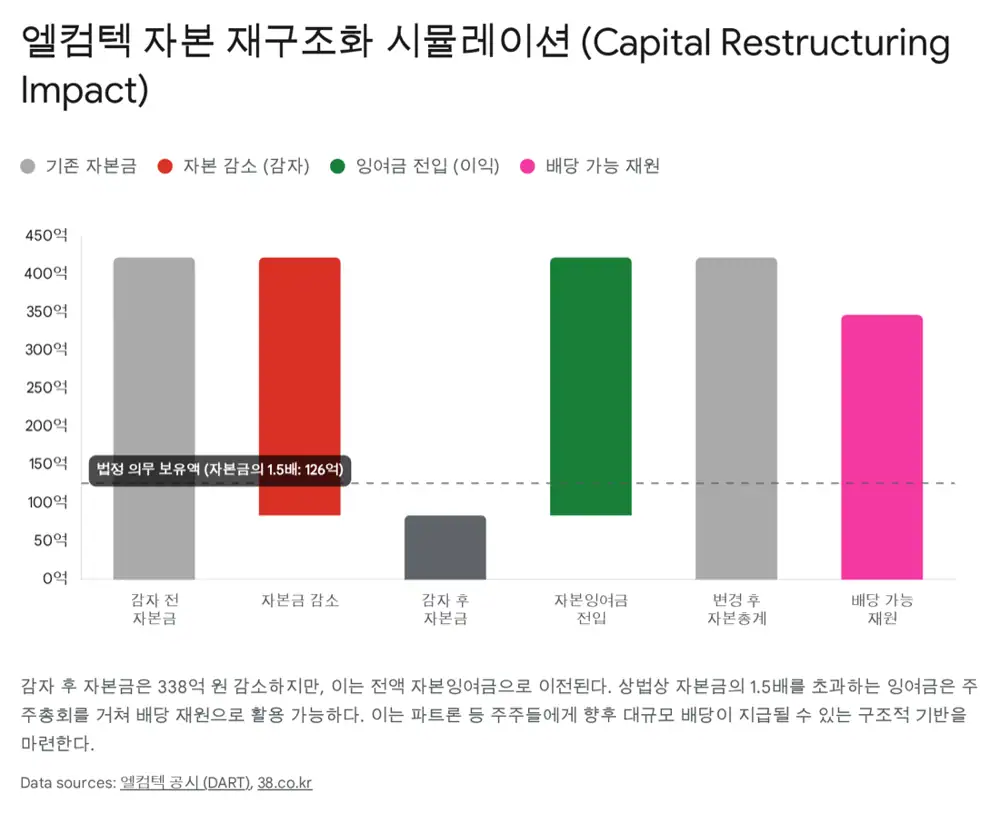

2. The mechanics of the 80% reduction

| Item | Before | After |

|---|---|---|

| Paid-in capital | KRW 42.22B | KRW 8.44B (-33.78B) |

| Shares outstanding | 84,447,519 | 16,889,504 (5-to-1 merge) |

| Legal reserve threshold (1.5× capital) | ~KRW 63.3B | ~KRW 12.6B |

- Method: Five KRW 500-par common shares merged into one (5-for-1).

- EGM: March 18, 2026.

- Trading halt: April 17 – May 7, 2026.

- New share listing: May 8, 2026.

Official fact: Per the 3Q25 filing, retained earnings are KRW 17.1B, debt ratio ~10%, effectively debt-free. With no deficit to recover, a deficit-driven reduction is not possible.

Interpretation: Article 461-2 of Korea’s Commercial Code allows the portion of legal reserves exceeding 1.5× paid-in capital to be transferred into distributable retained earnings. After the reduction the threshold drops from KRW 63.3B to 12.6B; combined with the KRW 33.8B reduction-gain, over KRW 30B of distributable capacity appears overnight.

3. Why Partron wants this — capital repatriation

- Partron owns 57.3%.

- Partron itself faces a slowing smartphone market — needs new growth funding and free cash flow.

- A return-of-capital dividend (vs ordinary profit dividend) often enjoys reduced or zero withholding tax for shareholders — tax-efficient.

The market’s 9% sell-off on the reduction announcement is likely temporary mispricing driven by the ‘reduction = bad news’ heuristic. A material dividend / buyback-and-cancel programme in 2H26 could be the re-rating catalyst.

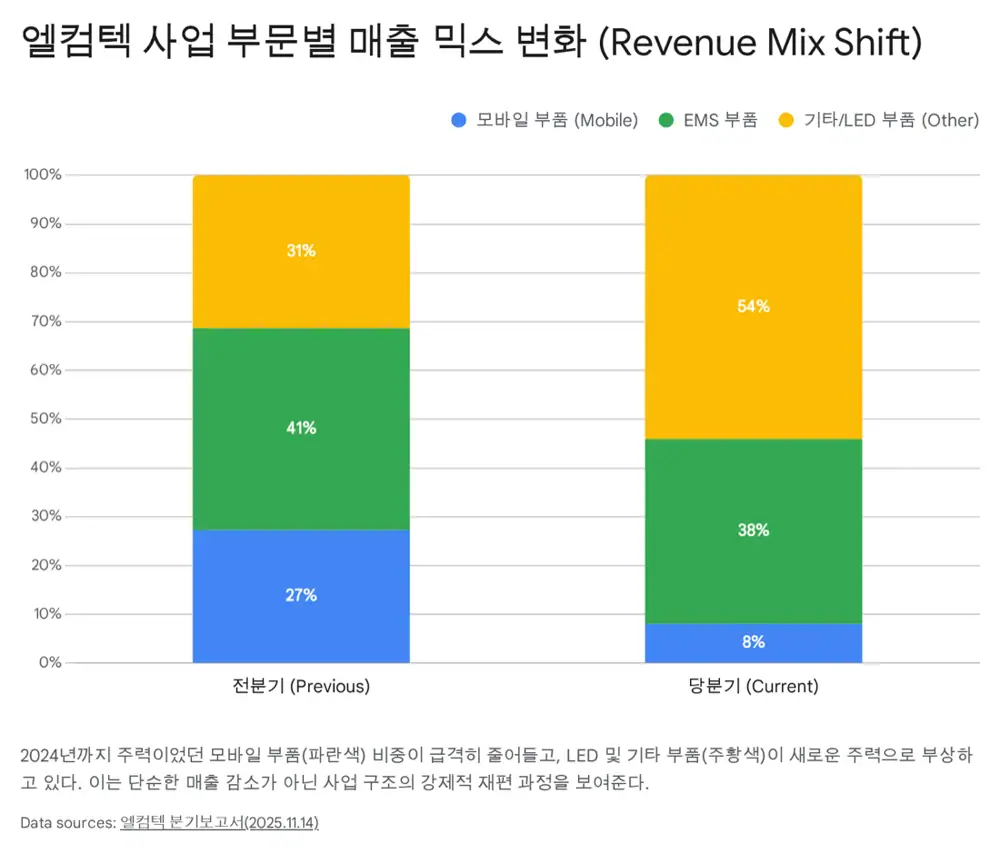

4. Fundamentals — a declining core and a portfolio in flux

| Division (3Q25) | Revenue | YoY / QoQ | Comment |

|---|---|---|---|

| Consolidated YTD revenue | KRW 33.6B | YoY -25.9% | Structural slowdown |

| Mobile camera components | KRW 2.7B | vs prior Q KRW 12.3B (-78%) | High-pixel / folded-zoom shift Elcomtec is not catching; price pressure from DioStech, Sekonix, Sunny Optical |

| Other components (incl. LED) | KRW 18.1B | vs prior Q +27.9% | Proprietary BLU light-guide tech for edge-lit LED — green-regulation tailwind |

| EMS | KRW 12.7B | vs prior Q -32% | IT-device demand and customer destocking |

5. Mongolia — a ‘free call option’

- AGM MINING LLC: Elcomtec owns 54.86%. Three exploration licences in Umnugobi, Mongolia — Toromkhon, Alag Shand, Tamgat.

- Same geological belt as the world-class Oyu Tolgoi Cu-Au mine.

- 3Q25 reality: revenue KRW 0, net loss KRW 0.93B. The parent has fully written off the KRW 11.2B loan via bad-debt provision — book value zero.

Interpretation: Fundamentally the licence carries zero value today, which means the current share price assigns the mine no embedded revenue. Treat it as a perpetual call option that has already been written off. Gold/copper supercycle pushing prices above mining BEP, or a discovery leading to a major-miner buyout, are the only paths where it monetises — but those paths are real lottery upside.

6. Financial safety margin

- Cash & equivalents: ~KRW 12.8B.

- Current ratio: 535%.

- Debt ratio: 7.7% — effectively net-cash.

- Retained earnings: KRW 17.1B — built up via decades of conservative finance.

6.2 Dividend-capacity simulation

Post-reduction capital is KRW 8.4B → 1.5× threshold KRW 12.6B. Reduction gain KRW 33.8B + existing capital surplus → over KRW 30B distributable.

- Assume 50% (~KRW 15B) of that capacity is paid out as a special / cash dividend.

- Post-reduction shares: 16,889,504.

- DPS ≈ KRW 888.

- Vs current market cap (~KRW 69.4B) → ~21% dividend yield. (Full payout unrealistic, but Partron’s funding need makes an aggressive policy plausible.)

7. SOTP valuation — Goldman-style

- Operating value: Conservative core net income KRW 2–3B, manufacturing PER 10–12× → KRW 20–36B. Current market cap exceeds this; on operations alone the stock is rich.

- Net-cash value: Net cash + post-reduction distributable reserves ≈ KRW 30B — about 43% of market cap. Strong downside support.

- Option value: Mongolian licences are lottery exposure; in a commodity rally markets pay an outsized premium. Estimated KRW 10–20B currently embedded in the share price.

8. Risks & strategy

Principal-agent

High dependence on Partron + capital policy may favour the controlling shareholder.

Core swings back to loss

Continued revenue erosion could push fixed costs over the line.

Commodity volatility

Falling gold/copper kills the theme — high-beta downside.

Event-driven entry points

- Trading resumption on May 8, 2026: reference-price optical illusion plus halted-trading supply vacuum often create a temporary dip.

- Confirmed easing cycle: real-rate decline structurally bids up gold.

- Pre-dividend announcement: when a large 2H26 payout becomes a discussed expectation.

Investment view

Neutral → Trading Buy. Target price is driven by ① gold and ② dividend size, not core earnings. Upside scenario = gold new highs + step-change DPS. Downside scenario = core remains in loss + no post-reduction dividend + commodity rollover.

9. Conclusion

Elcomtec is mid-transformation from ‘manufacturer’ to ‘asset/investment company.’ The 80% reduction is the firing pin of that identity change. Investors should stop reacting to lens-shipment swings and instead bet on ① Partron’s capital repatriation playbook and ② macro (gold/copper/rates). It earns a slot only as a niche ‘cash-flow (dividends) + inflation hedge (gold)’ holding — sized small and watched closely from the May 2026 trading restart.

Sources

- Naver blog source: m.blog.naver.com/.../224157809283

- Elcomtec (037950) — KIND disclosure (capital reduction): kind.krx.co.kr

- Commercial Code Art. 461-2 (return-of-capital dividend): law.go.kr

- Partron (091700) — parent company: FnGuide

- Oyu Tolgoi mine (Wikipedia) — geological reference: en.wikipedia.org