DEEP RESEARCH · AIRBUS

Airbus Deep Dive: From Supply-Chain Fog to a Cash-Flow Supercycle

How A321XLR, production recovery, Spirit assets, and services can expand margins in 2026

0. Bottom line first

My 2026 view on Airbus is simple: the orders are already there; deliveries and cash conversion are now the real test. The source cites 793 commercial aircraft deliveries in 2025, an 8,754-aircraft backlog, and the A321XLR's unique middle-market position as support for an execution premium versus Boeing.

793

Airbus 2025 actual deliveries, 193 aircraft ahead of Boeing's 600.

8,754

Roughly 11 years of work at current delivery levels, according to the source.

EUR 4.5B+

The source expects 2026 free cash flow above EUR 4.5 billion, excluding customer financing.

Official fact: The source compares 2025 deliveries of 793 aircraft for Airbus and 600 for Boeing, and lists 2026 expected deliveries of roughly 900 for Airbus and 750 for Boeing.

Interpretation: The market's execution-risk discount can narrow as supply bottlenecks clear. Still, the GTF engine issue, tariff risk, and execution of the space restructuring remain key watch items.

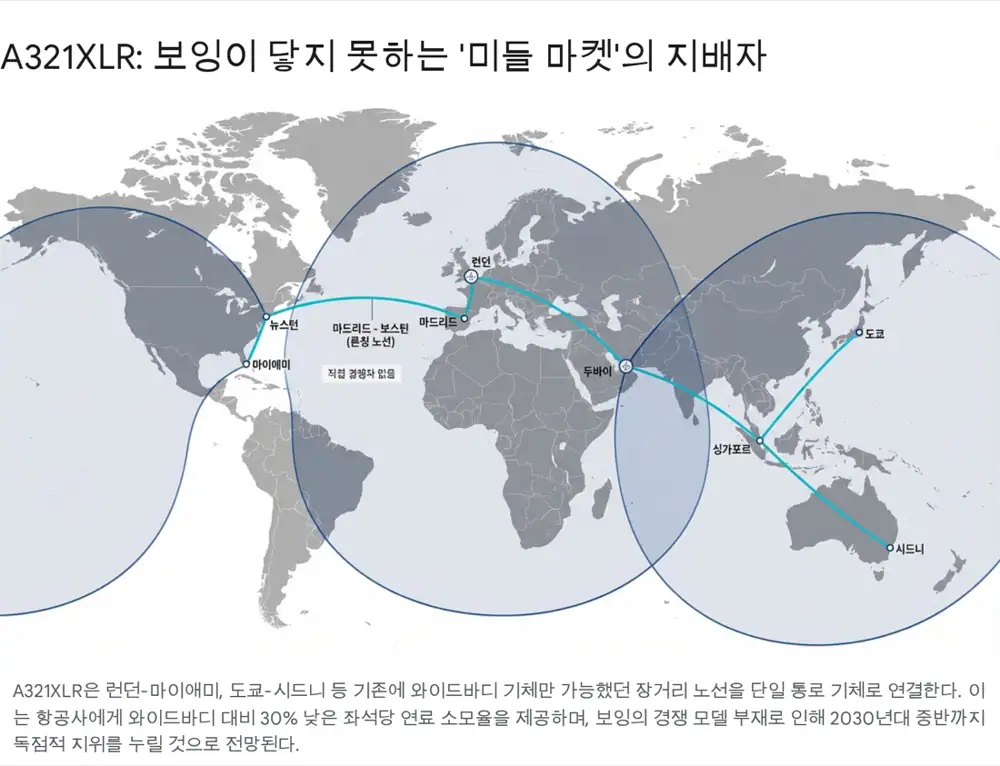

1. Product moat: the market A321XLR opened

The A321XLR can fly up to 4,700 nautical miles, or about 8,700 km. The point is that routes such as London-Miami, Tokyo-Sydney, and Madrid-Boston can be served with narrowbody economics.

Boeing abandoned the NMA project and remains tied up with 737 MAX 10 certification, so the source argues Airbus may have pricing power in this high-margin middle-market segment for the next five to seven years. Commercial service began with Iberia in late 2024, with broader deliveries to American Airlines, Qantas, and others in 2025-2026.

2. Supply chain: Spirit acquisition and bottleneck relief

The 2025 acquisition of Spirit AeroSystems assets is framed as vertical integration that reduces supply-chain risk. Airbus secured facilities including Kinston in the U.S. and St. Nazaire in France for A350 fuselage sections, and Belfast for A220 wings.

Official fact: The source says Airbus received USD 559 million in compensation while selectively acquiring core assets, and that the assets are important for reaching A350 rate 12 after 2026 and A220 rate 14.

Pratt & Whitney's GTF powdered-metal issue was a major source of A320neo delivery delay. A roughly 360-day turnaround time remains a burden, but the source says the issue appears to be past peak; normalizing engine supply in 2026 could reduce glider inventory and improve cash flow.

| Program | Target / issue | Investment read |

|---|---|---|

| A320neo family | Rate 75 per month by 2027 | Core profit engine; Tianjin and Mobile line expansion |

| A220 | Rate 14 by 2026; BEP expected late 2026 | Belfast integration can lower component cost |

| A350 | Rate 12 per month by 2028 | Widebody replacement demand and 777X delays help |

| GTF engine | About 360-day turnaround time | Glider reduction is key for near-term cash flow |

3. Future technology and materials

Airbus is developing its ZEROe hydrogen aircraft for a 2035 commercialization target, now centered on hydrogen fuel-cell electric propulsion. The source says integrated ground testing is scheduled for 2026-2027.

For titanium parts, Airbus is introducing wire arc additive manufacturing, or w-DED, to reduce material waste and raise production speed versus forging. After dependence on Russian titanium created supply imbalance, 2024 buffer stock temporarily reduced 2025 demand; the source expects demand to rebound with production increases in 2026.

2035 target

Fuel-cell electric propulsion is the route chosen to improve feasibility.

Titanium innovation

A technology hedge against material waste and supply instability.

2026 rebound

Higher production rates can pull titanium demand back up.

4. End-market demand: Asia growth and services

According to the Airbus Global Market Forecast 2025-2044 as summarized in the source, air traffic is expected to grow 3.6% annually over the next 20 years, with India domestic routes at 8.9% and Asia-Middle East at 5.3%. Large orders from IndiGo and Air India show the A320neo family becoming a standard platform for Asian LCCs.

In 2026-2028, replacement demand for aging B777-200ERs and A330ceos should rise, while Boeing 777X certification delay can benefit the A350-1000. Delivery delays also extend the life of existing fleets and increase parts and maintenance demand. The source says Airbus expects the services market to double to USD 311 billion by 2044.

5. 2026 financial impact: execution gap in numbers

| Item | 2025 actual deliveries | 2026 expected deliveries | Backlog | Note |

|---|---|---|---|---|

| Airbus | 793 | ~900 | 8,754 | A321XLR ramp and A350 rate increase |

| Boeing | 600 | ~750 | 6,713 | 737 MAX recovery but gap remains |

| Gap | +193 | +150 expected | +2,041 | Airbus lead continues |

The source interprets the data as Airbus delivering about 32% more aircraft than Boeing. If 2024-2025 were years of cleaning up supply-chain disruption and space losses, 2026 is framed as a year when volume, price, and cost reduction can work together.

6. Defence, space, and capital allocation

The space unit's roughly EUR 1.5 billion provision and 2,500-person job-cut plan are short-term burdens. Cuts are described across Europe: 689 in Germany, 540 in France, 477 in the U.K., and 303 in Spain. The source expects low-return satellite projects to be reduced and focus to shift toward Eurofighter and military drones, with a 1-2 percentage-point EBIT margin benefit in 2026.

Financially, net cash was about EUR 7 billion as of 3Q25. 2026 FCF is expected above EUR 4.5 billion excluding customer financing. For FY2024, Airbus proposed a EUR 2.00 ordinary dividend and EUR 1.00 special dividend, or EUR 3.00 total cash return. The payout ratio is presented as being kept near the upper end of the 30-50% range.

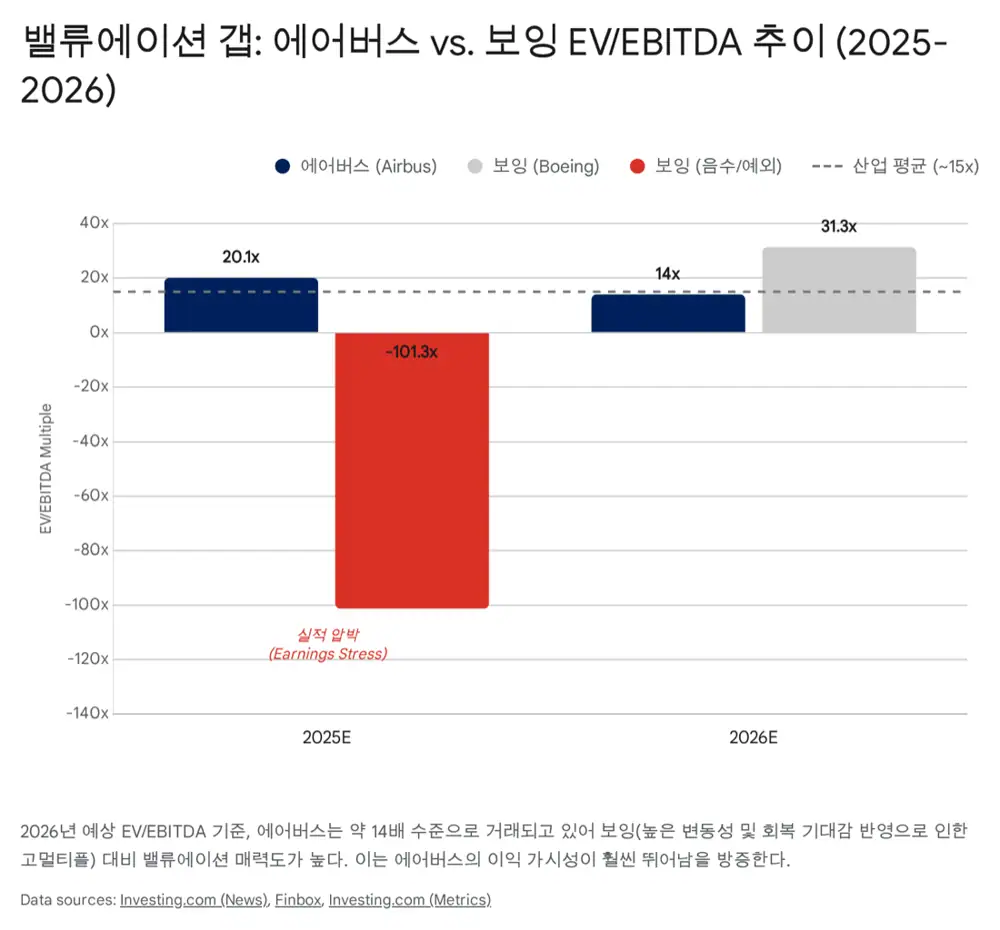

7. Valuation and checkpoints

The source says Airbus trades at roughly 14x expected 2026 EV/EBITDA. Boeing, by contrast, has weak or negative profitability, making its valuation difficult or optically above 30x. The argument is that Airbus deserves a visibility premium because it has demonstrable earnings power.

Major global banks such as UBS and RBC are cited as raising Airbus targets to EUR 230-240, implying about 15-20% upside from the source's reference point. Further rerating depends on delivering roughly 900 aircraft in 2026 and proving margin improvement; residual GTF effects, small supply-chain cracks, and possible Trump administration tariffs remain risks to monitor.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157678858

- Forecast International: December 2025 orders and deliveries: https://flightplan.forecastinternational.com/2026/01/15/airbus-and-boeing-report-december-2025-commercial-aircraft-orders-and-deliveries/

- Airbus: Spirit AeroSystems sites acquisition: https://www.airbus.com/en/newsroom/press-releases/2025-12-airbus-completes-acquisition-of-spirit-aerosystems-sites

- Airbus: A321XLR certification campaign: https://fly.airbus.com/A321XLR-certification

- Flight Plan: Defence and Space restructuring: https://flightplan.forecastinternational.com/2024/10/18/airbus-defence-and-space-restructures-cutting-2500-jobs/

- Simple Flying: A321XLR cost: https://simpleflying.com/airbus-a321xlr-how-much-it-costs/

- ePlaneAI: A321XLR one year in service: https://www.eplaneai.com/news/a321xlr-marks-one-year-in-service-as-longest-range-narrowbody

- One Mile at a Time: American A321XLR routes: https://onemileatatime.com/guides/american-airbus-a321xlr-flights/

- MTU Aero Report: A321XLR chapter: https://aeroreport.de/en/good-to-know/airbus-a321xlr-a-new-chapter-for-aviation

- Aerospace Global News: Airbus 2026 expectations: https://aerospaceglobalnews.com/news/airbus-2026-targets-expectations/

- Airbus: ZEROe hydrogen aircraft: https://www.airbus.com/en/innovation/energy-transition/hydrogen/zeroe-our-hydrogen-powered-aircraft

- Airbus: 2025 Summit hydrogen technologies: https://www.airbus.com/en/newsroom/press-releases/2025-03-airbus-showcases-hydrogen-aircraft-technologies-during-its-2025

- Airbus: titanium 3D printing: https://www.airbus.com/en/newsroom/stories/2026-01-how-airbus-is-pioneering-aircraft-manufacturing-with-titanium-3d-printing

- Travel Tourister: JetBlue GTF engine crisis: https://www.traveltourister.com/news/jetblue-pratt-whitney-360-day-engine-maintenance-crisis-15-aircraft-grounded-caribbean-flights-aruba-incident-exposes-11-billion-gtf-disaster-january-2026/

- Argus: Airbus titanium demand: https://www.argusmedia.com/en/news-and-insights/latest-market-news/2615979-airbus-ti-demand-to-dip-in-2025-rebound-in-2026

- Airbus: A320 production ramp: https://www.airbus.com/en/newsroom/stories/2025-10-ramping-up-a320-family-production

- Simple Flying: A320 production expansion: https://simpleflying.com/why-airbus-expanding-a320-production-worldwide/

- Global Banking & Finance: A220 delays: https://www.globalbankingandfinance.com/airbus-a220-nine/

- Airbus Global Market Forecast 2025-2044: https://www.airbus.com/en/products-services/commercial-aircraft/global-market-forecast

- Airbus GMF 2025 press release: https://www.airbus.com/en/newsroom/press-releases/2025-06-airbus-global-market-forecast-2025-people-and-commerce-driving-air

- Simple Flying: A350-1000 vs 777-9: https://simpleflying.com/airbus-a350-1000-boeing-777-9-battle/

- Airbus: services market projection: https://www.airbus.com/en/newsroom/press-releases/2025-10-airbus-projects-resilient-growth-of-services-market-in-the-next-20

- AeroMorning: 2025 Airbus vs Boeing estimates: https://aeromorning.com/en/2025-airbus-vs-boeing-deliveries-orders-estimations/

- Webull Malaysia: BofA delivery target note: https://www.webull.com.my/news-detail/14156344947606528

- Manufacturing Dive: Boeing delivered 600 aircraft: https://www.manufacturingdive.com/news/boeing-deliveries-q4-full-year-2025-commercial-airbus/809504/

- ePlaneAI: Boeing orders and deliveries: https://www.eplaneai.com/news/boeing-surpasses-airbus-orders-in-2025-as-deliveries-total-600

- The Air Current: A220-500 profitability: https://theaircurrent.com/aircraft-production/airbus-a220-500-launch-paced-by-program-profitability/

- ch-aviation: Quebec A220 write-off: https://www.ch-aviation.com/news/159321-quebec-writes-off-us285mn-in-a220-programme

- Aerospace Global News: space unit job cuts: https://aerospaceglobalnews.com/news/airbus-to-cut-more-than-2000-jobs-amid-restructuring-of-space-unit/

- Aerospace Testing International: Defence and Space restructuring: https://www.aerospacetestinginternational.com/news/airbus-defence-and-space-restructures-following-cuts.html

- Airbus: 9M 2025 results: https://www.airbus.com/en/newsroom/press-releases/2025-10-airbus-reports-nine-month-9m-2025-results

- Airbus: FY 2024 results: https://www.airbus.com/en/newsroom/press-releases/2025-02-airbus-reports-full-year-fy-2024-results

- Airbus: limited share buyback: https://www.airbus.com/en/newsroom/press-releases/2025-09-airbus-commences-limited-share-buyback-to-support-future-employee

- Investing.com: Morgan Stanley target: https://www.investing.com/news/stock-market-news/airbus-stock-target-raised-at-morgan-stanley-on-production-progress-4329629

- Finbox: Boeing forward EV/EBITDA: https://finbox.com/NYSE:BA/explorer/ev_to_ebitda_fwd/

- Investing.com: UBS EUR240 target: https://www.investing.com/news/analyst-ratings/airbus-stock-price-target-raised-to-eur240-by-ubs-on-delivery-outlook-93CH-4439141

- Outlook Business: tariff risk: https://www.outlookbusiness.com/news/boeing-airbus-aircraft-prices-to-surge-due-to-new-tariffs-heres-why