DEEP RESEARCH · Boeing

Boeing: From Turbulence Toward Structural Normalization

The 2026 turnaround case built on 737 MAX output, 787 normalization, Spirit reintegration, and defense-loss control

0. Bottom Line First

The Boeing thesis is not simply that the stock has fallen too much. It is about production normalization and free-cash-flow recovery. The remaining risks are quality trust, FAA certification, debt, and fixed-price defense losses.

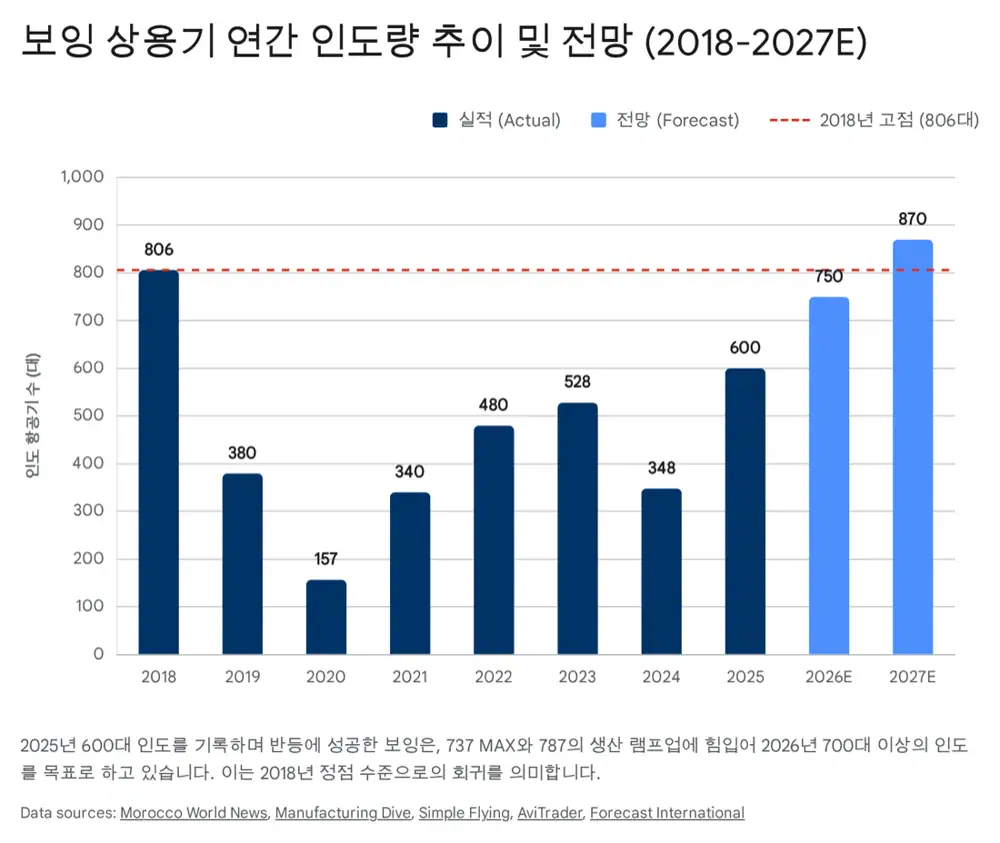

- 2025 commercial aircraft deliveries are presented as 600 units, up 72% from 2024.

- The key 2026 assumptions are 737 MAX monthly production recovering to 47 units, 787 production normalizing to 10 units per month, and FCF turning positive.

- The Spirit AeroSystems reintegration is framed as a way to internalize quality control and vertically integrate the supply chain.

- 777X delays, MAX 7 and MAX 10 certification, defense-program losses, and China delivery resumption are major variables.

1. Three Pillars of Recovery

Commercial Deliveries

737 MAX and 787 production normalization are the starting points for inventory monetization and FCF recovery.

Quality and Supply-Chain Control

The Spirit deal is a short-term burden but is presented as a medium- to long-term tool for fuselage quality control and duplicate-cost removal.

Cash Flow and Credit

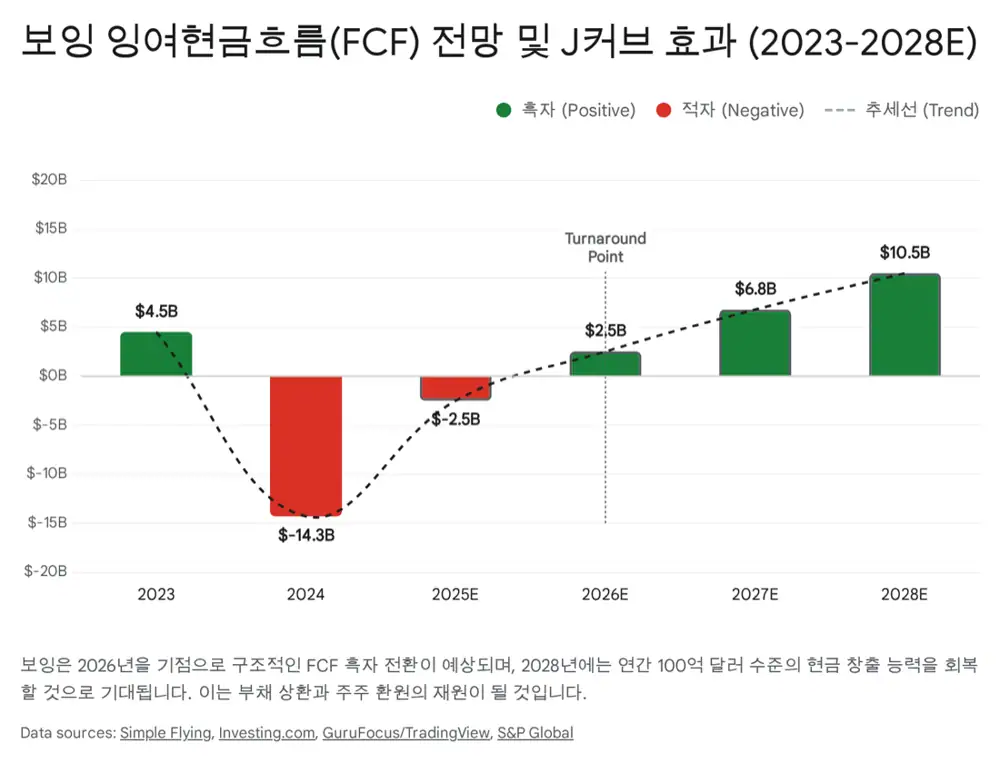

The setup is to reduce debt pressure and defend investment-grade status through capital raising and production recovery.

2. Commercial Aircraft and Certification Risk

Official fact: The source cites materials on 737 MAX 10 and MAX 7 certification, 777X delays, China-bound MAX delivery resumption, and Airbus-Boeing supply competition.

Interpretation: Demand is strong, but supply is the bottleneck. Boeing’s stock can therefore be more sensitive to actual deliveries, production rate, and restored confidence from the FAA and customers than to headline orders alone.

3. Defense and Financials: The Shadow Side of Recovery

- The defense segment’s recurring fixed-price contract losses reduce the credibility of the turnaround.

- Large programs such as KC-46, T-7A, and VC-25B require tighter cost control and improved contract structures.

- A possible increase in defense spending under the Trump administration may help the order environment, but profitability still requires separate verification.

- Credit-rating agencies will care about FCF improvement and the debt-reduction path.

4. Checkpoints and Risks

| Checkpoint | Why it matters |

|---|---|

| Monthly 737 production rate | The most direct leading indicator for FCF recovery |

| 787 delivery pace | Confirms cash generation from a higher-margin widebody program |

| MAX 7, MAX 10, and 777X certification | Determines new-model portfolio and customer delivery schedules |

| Spirit integration | Shows whether quality and cost-structure improvements are real |

| Defense losses | Tests whether defense losses offset commercial-aircraft recovery |

Sources

- https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157677934

- https://www.moroccoworldnews.com/2026/01/275695/boeing-ends-2025-with-600-aircraft-deliveries-and-1173-net-orders/

- https://www.manufacturingdive.com/news/boeing-deliveries-q4-full-year-2025-commercial-airbus/809504/

- https://simpleflying.com/6-reasons-boeing-dominate-2026/

- https://www.investing.com/analysis/why-2026-is-set-to-be-a-turnaround-year-for-boeing-and-its-stock-200673380

- https://investors.boeing.com/investors/news/press-release-details/2025/Boeing-Completes-Acquisition-of-Spirit-AeroSystems/default.aspx

- https://finviz.com/news/283924/boeing-vs-lockheed-martin-which-aerospace-defense-giant-has-the-edge

- https://www.cfr.org/articles/trumps-15-trillion-defense-budget-should-not-come-surprise

- https://en.wikipedia.org/wiki/Competition_between_Airbus_and_Boeing

- https://www.enginecowl.com/boeing-q3-2025/

- https://seekingalpha.com/news/4510189-boeing-delays-777x-to-2027-takes-4_9-billion-charge-as-costs-mount

- https://avitrader.com/2026/01/21/1800-aircraft-deliveries-expected-in-2026-says-iba/

- https://simpleflying.com/why-all-3-us-legacy-carriers-orders-boeing-737-max-10/

- https://simpleflying.com/boeing-airbus-set-win-2026/

- https://theaircurrent.com/aircraft-development/boeing-advances-737-max-10-into-next-phase-of-faa-flight-testing/

- https://aerospaceglobalnews.com/news/will-the-boeing-737-max-10-and-7-be-certified-in-2026/

- https://simpleflying.com/boeing-expecting-positive-cash-flow-2026-increased-deliveries/

- https://www.ch-aviation.com/news/149786-lufthansa-to-take-first-b777x-delivery-in-2026-boeing

- https://en.wikipedia.org/wiki/Boeing_777X

- https://breakingdefense.com/2025/01/boeing-to-log-1-7b-in-defense-program-losses-in-fourth-quarter/

- https://www.defensenews.com/industry/2024/01/09/cautionary-tale-how-boeing-won-a-us-air-force-program-and-lost-7b/

- https://www.nasdaq.com/articles/just-time-2026-boeing-wins-128-billion-2-big-defense-contracts

- https://www.tenderalpha.com/blog/post/fundamental-analysis/boeing-improving-free-cash-flow-generation-to-allow-debt-payback

- https://www.iata.org/en/publications/economics/reports/global-outlook-for-air-transport-december-2025/

- https://www.iata.org/en/pressroom/2025-releases/2025-12-09-01/

- https://airinsight.com/airbus-and-boeing-looking-ahead-2026-2030/

- https://www.congress.gov/crs-product/IN12455

- https://breakingdefense.com/2024/12/defense-industry-could-see-big-shakeup-under-trump-2025-preview/

- https://www.mining.com/web/boeing-suspends-buying-titanium-from-russia-assures-of-sufficient-supply/

- https://www.questmetals.com/blog/the-impact-of-the-russia-ukraine-conflict-on-the-aerospace-supply-chain

- https://theaircurrent.com/china/boeing-wins-key-caac-clearance-on-737-max-deliveries-to-china/

- https://aerospaceglobalnews.com/news/boeing-china-737-max-deliveries-resume/

- https://leehamnews.com/2025/10/23/impact-will-boeings-china-deliveries-under-trumps-latest-tariff-tiff-will-be-minimal/

- https://investors.boeing.com/investors/news/press-release-details/2025/Boeing-Reports-Third-Quarter-Results/default.aspx

- https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3470261

- https://intellectia.ai/news/stock/boeings-737-max-production-increases-to-42-deliveries-hit-record-high

- https://aerospaceglobalnews.com/news/what-to-expect-boeing-2026/

- https://www.eplaneai.com/news/boeing-forecasts-increased-737-and-787-deliveries-in-2026

- https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3422051

- https://www.defenseone.com/business/2025/01/boeings-defense-unit-eat-17-billion-fourth-quarter/402472/

- https://www.iam751.org/2024StrikeProposal/

- https://unionlabel.org/2024/11/26/industry-leading-boeing-contract-delivers-historic-wage-increases-for-frontline-workers/

- https://www.spiritaero.com/pages/release/spirit-aerosystems-announces-acquisition-by-boeing-in-8.3-billion-transaction/

- https://markets.financialcontent.com/bigspringherald/article/predictstreet-2026-1-9-boeings-path-to-redemption-a-2026-comprehensive-deep-dive-nyse-ba

- https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3470260

- https://www.tradingview.com/news/gurufocus:e141ad77e094b:0-boeing-s-10-billion-comeback-cfo-unveils-bold-2026-cash-plan-that-just-shocked-wall-street/

- https://investors.boeing.com/investors/news/press-release-details/2024/Boeing-Announces-Pricing-of-Upsized-Concurrent-Offerings-of-Common-Stock-and-Depositary-Shares/default.aspx

- https://trendspider.com/blog/boeing-to-raise-24-3b-via-share-offering/

- https://www.investing.com/news/stock-market-news/boeings-baa3-rating-affirmed-by-moodys-outlook-now-stable-93CH-4406427