DEEP RESEARCH · ITCEN PNS (A232830)

ITCEN PNS — Becoming Korea’s Secure Cloud & Infra Platform

Triple momentum: +1,461% revenue jump from subsidiary consolidation, biometric/PQC mandates, overhang clearance

0. Bottom line first

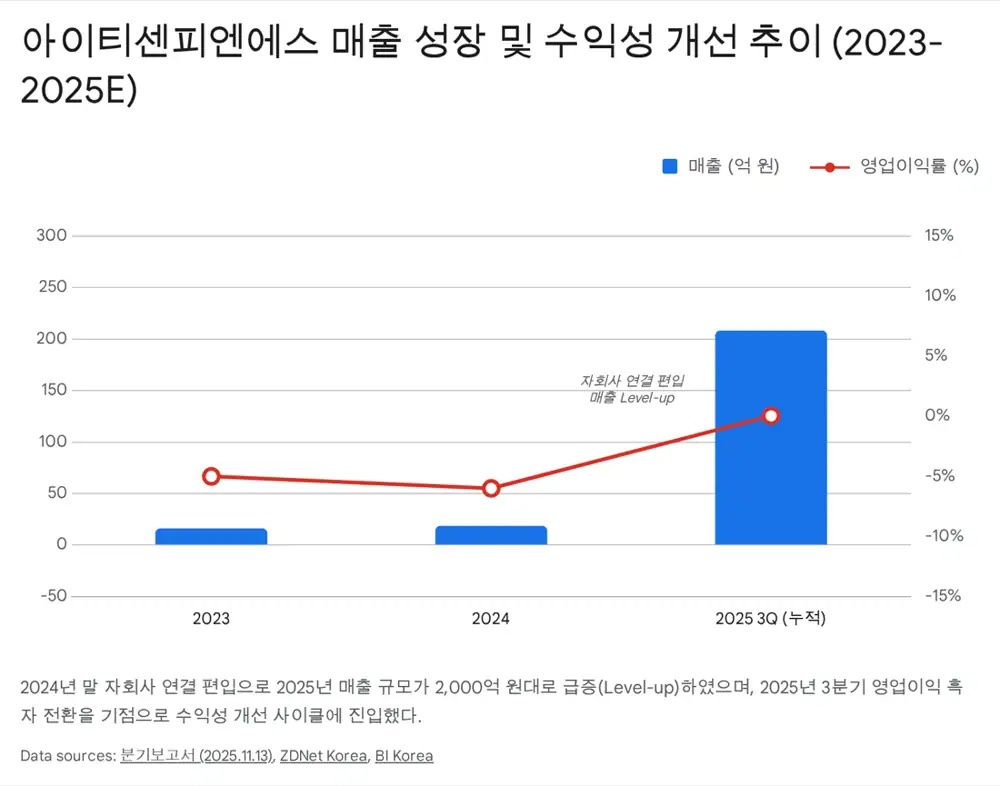

2025 was the inflection point for ITCEN PNS: ① consolidation of subsidiaries C-Platform and 2KM Systems drove quarterly revenue from sub-KRW-100B levels to KRW 208.3B (YoY +1,461.9%) with operating profit flipping to a KRW 80M black; ② the controlling shareholder ITCEN CTS fully converted its KRW 10B 3rd-series private CB, removing the overhang and lifting ownership from 24.41% to 46.47%; and ③ the 2025–2026 stack of mandates — financial-sector biometric authentication, Zero Trust guidelines, PQC migration — maps directly onto the company’s core tech.

1. Identity re-definition — from SecuCen to ITCEN PNS

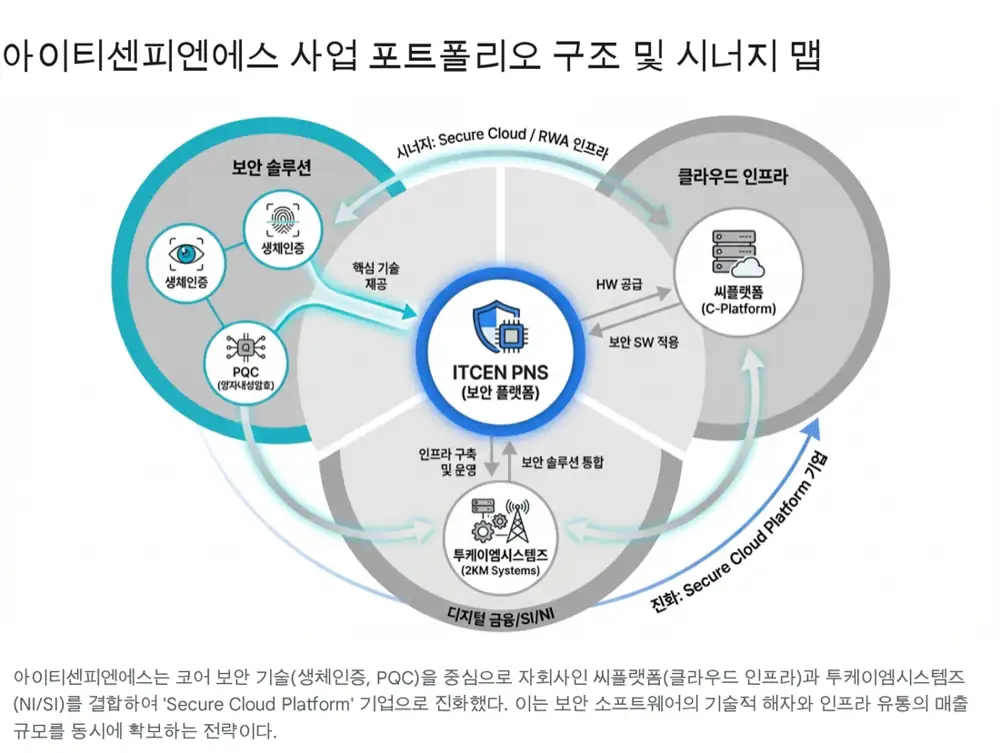

At the March 2025 AGM the company renamed itself SecuCen → ITCEN PNS, where PNS stands for Platform & Network Security. The name declares that the company is no longer just a security ISV but the group’s digital-platform-plus-security-infrastructure arm.

Official fact: In Nov 2024 the company absorbed C-Platform (group cloud distributor) and 2KM Systems (network integrator) as subsidiaries, completing a vertical stack of ‘hardware → middleware → security software’.

Interpretation: SecuCen was a strong mobile/bio security ISV but lacked scale. The rebrand is the first step toward re-rating as a mid-cap IT platform rather than a small security vendor.

2. Governance — CB conversion ends the overhang

- Nov 12, 2025 — controlling shareholder ITCEN CTS (formerly Comtec Systems) fully converted its KRW 10B 3rd-series private CB.

- Newly issued shares: ~4.82M, all absorbed by the controlling shareholder.

- Ownership rose from 24.41% to 46.47%.

- Liability → equity reclassification lowered the debt ratio and lifted total equity.

CB conversions usually raise dilution concerns, but here the controlling shareholder swallowed the whole tranche — eliminating market supply and signalling ‘undervaluation + commitment to responsible management.’ Chosun Biz, ZDNet Korea, CEO Score Daily, Busan Ilbo.

3. Business model — the Triple Growth Engine

3.1 Core security solutions

DocuTrust III / EdgeBio

Signed a ‘bio e-signature tech-support pact’ with the Korea Financial Telecommunications & Clearings Institute — biometric data is split-stored across the institute’s data center and bank servers. Standard installed at Samsung Life, Samsung F&M, Hyundai M&F, Meritz F&M, KB Insurance.

AppIron

Tamper protection, code obfuscation, virtual keypad and mobile antivirus in a single suite. 3Q25 maintenance revenue KRW 1.15B (vs KRW 0.99B) — recurring base strengthening.

Post-Quantum Cryptography

June 2025 — PQC deployed on Hana Bank’s Seoul ↔ New York / London transmission lines and on a domestic smart-office. First real-world banking deployment in Korea against the ‘Harvest Now, Decrypt Later’ threat. E-Science

3.2 IT infrastructure / cloud (C-Platform / 2KM Systems)

- C-Platform: Korean distributor for IBM, Lenovo, HPE and Red Hat. Surging enterprise-AI demand has driven HPC equipment revenue higher — standalone product revenue jumped to KRW 76.9B (vs KRW 0.11B).

- 2KM Systems: Network-integration partner of Juniper Networks and others — provides the physical layer of identity-based network access control needed for Zero Trust.

3.3 Digital finance — EdgeQwallet (MPC-based wallet)

ITCEN PNS owns the security/wallet stack for Busan Digital Asset Exchange (BDAN), led by parent ITCEN. MPC (Multi-Party Computation) splits private keys across nodes — no single point of failure. CEO Score Daily — 1Q sales and PQC wallet

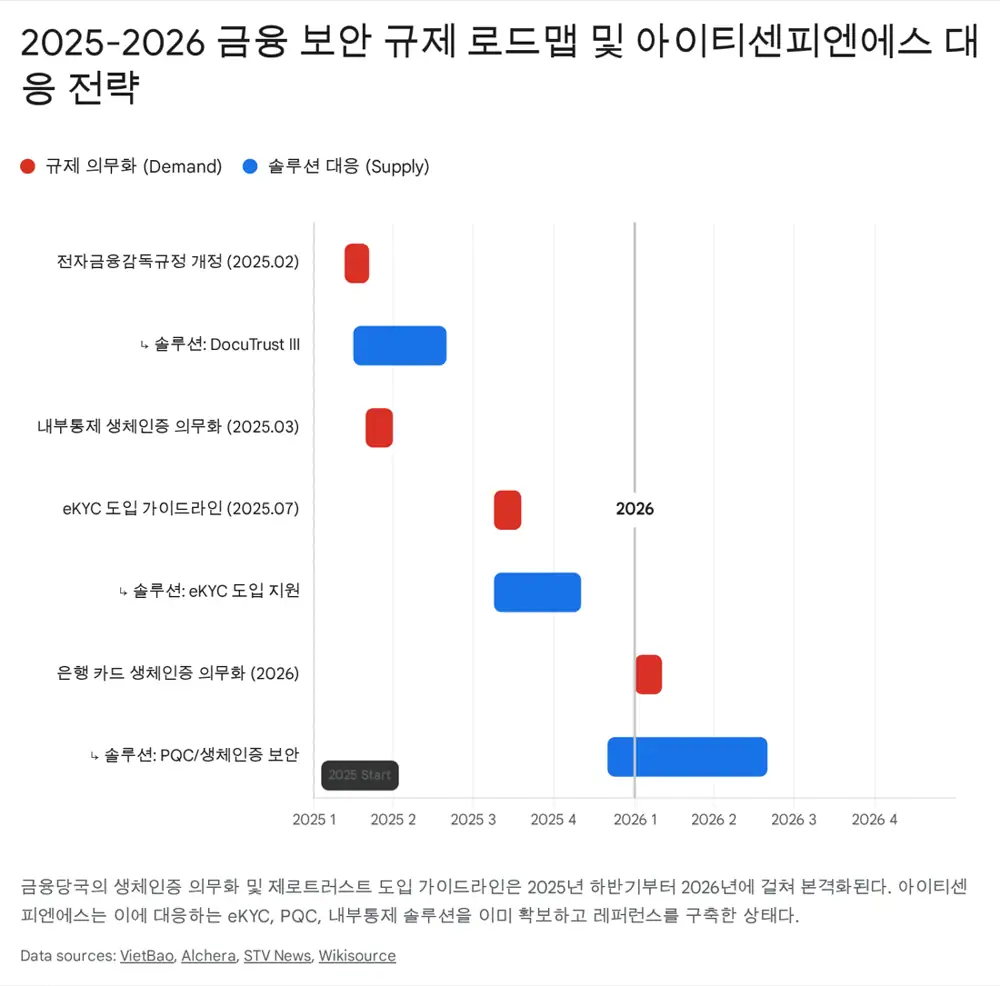

4. Market environment — Triple Regulations supercycle

4.1 Biometric authentication mandate

- FSC/FSS revised the electronic-finance supervisory rules — biometric authentication is mandatory for internal-control systems at financial institutions. Supervisory rule 2025-4

- 2025: Tier-1 banks accelerate IAM with biometrics → EdgeBio direct beneficiary.

- Jan 2026 onwards: Customer-facing transactions like card issuance and high-value transfers also require biometric checks → addressable market expands from B2E into B2C. Vietbao (2026.01), STV News

4.2 Zero Trust — the price of relaxed network segregation

Korea is loosening physical network-isolation rules in exchange for mandatory Zero Trust adoption. ‘Never trust, always verify’ shifts the perimeter from network to identity and data. ITCEN PNS owns the full stack: identity (EdgeBio) + device integrity (AppIron) + data encryption (PQC / EdgeDB) + network control (2KM Systems). Byline Network, BoanNews — Zero Trust 2025 report

4.3 PQC market opens

NIST PQC standards drive a global crypto-migration. The Hana Bank pilot puts ITCEN PNS 1–2 years ahead of peers in domestic banking. ZDNet — with We4MB on banking security

5. Financials — the quantum jump

| Item (3Q25 cumulative) | Amount | YoY / note |

|---|---|---|

| Consolidated revenue | KRW 208.3B | +1,461.9% (vs ~KRW 13.3B) — full-period subsidiary contribution |

| Consolidated operating profit | KRW 80M | Turned to profit (OPM 0.04% — distribution mix dilutes margin) |

| Consolidated net loss | KRW -2.9B | Non-cash items: CB valuation, PPA amortisation |

| Standalone revenue | KRW 17.3B | +30% YoY — core business solid |

| Standalone product revenue | KRW 7.69B | Up from KRW 0.11B — large turn-key wins |

| Standalone maintenance | KRW 1.15B | Up from KRW 0.99B — recurring growth |

BI Korea — record results, FnGuide snapshot

Margin recovery path (J-curve)

- Mix: Distribution drives the top line; security software drives margin. 2026 mandates expand SW share → corporate OPM recovers quickly.

- Insourcing: Less external dev, more in-house engineering → unit cost down.

6. Risks

- Persistent low margin: C-Platform-led distribution is large but thin. Mitigation: ITCEN PNS is pivoting to value-added distribution (VAD).

- Mandate slippage: Biometric / STO timelines could slip — but Samsung Life and other private references already provide base growth.

- Residual overhang: Monitor remaining CB/BW (per latest filings, the major KRW 10B CB has been retired).

7. Conclusion — readying for 2026 take-off

Earnings turn + overhang gone

Visible support for the share price.

Biometric & PQC mandates

SW J-curve drives corporate margin.

Standard wallet for RWA/STO

EdgeQwallet positioned to be the de-facto wallet vendor.

ITCEN PNS is being redefined from ‘small security stock’ into ‘digital finance infrastructure platform’ — short-term levers are visible (earnings, governance) while PQC and RWA megatrends open the long-term upside. Asymmetric setup.

Sources

- Naver blog source: m.blog.naver.com/.../224157582505

- BI Korea — record 3Q revenue: bikorea.net

- FnGuide A232830 snapshot: comp.fnguide.com

- Vietbao — 2026 card-issuance biometric mandate: vietbao.vn

- STV News — biometric mandate by March: stvnews.kr

- Chosun Biz — KRW 10B CB conversion completed: biz.chosun.com

- CEO Score Daily — overhang cleared: ceoscoredaily.com

- ZDNet — controlling shareholder CB conversion: zdnet.co.kr

- Busan Ilbo — overhang completely resolved: busan.com

- E-Science — PQC at Hana Bank: e-science.co.kr

- ZDNet — with We4MB on banking security: zdnet.co.kr

- CEO Score Daily — 1Q earnings & PQC wallet: ceoscoredaily.com

- Electronic Finance Supervisory Rule 2025-4: ko.wikisource.org

- Byline Network — Zero Trust: byline.network

- BoanNews — Zero Trust architecture 2025: boannews.com