DEEP RESEARCH · ATON

ATON: The fintech-security moat and the unrelated diversification dilemma

A review of mSafeBox, PASS, MLS regulation, exchangeable bonds, and the controlling shareholder pledge risk.

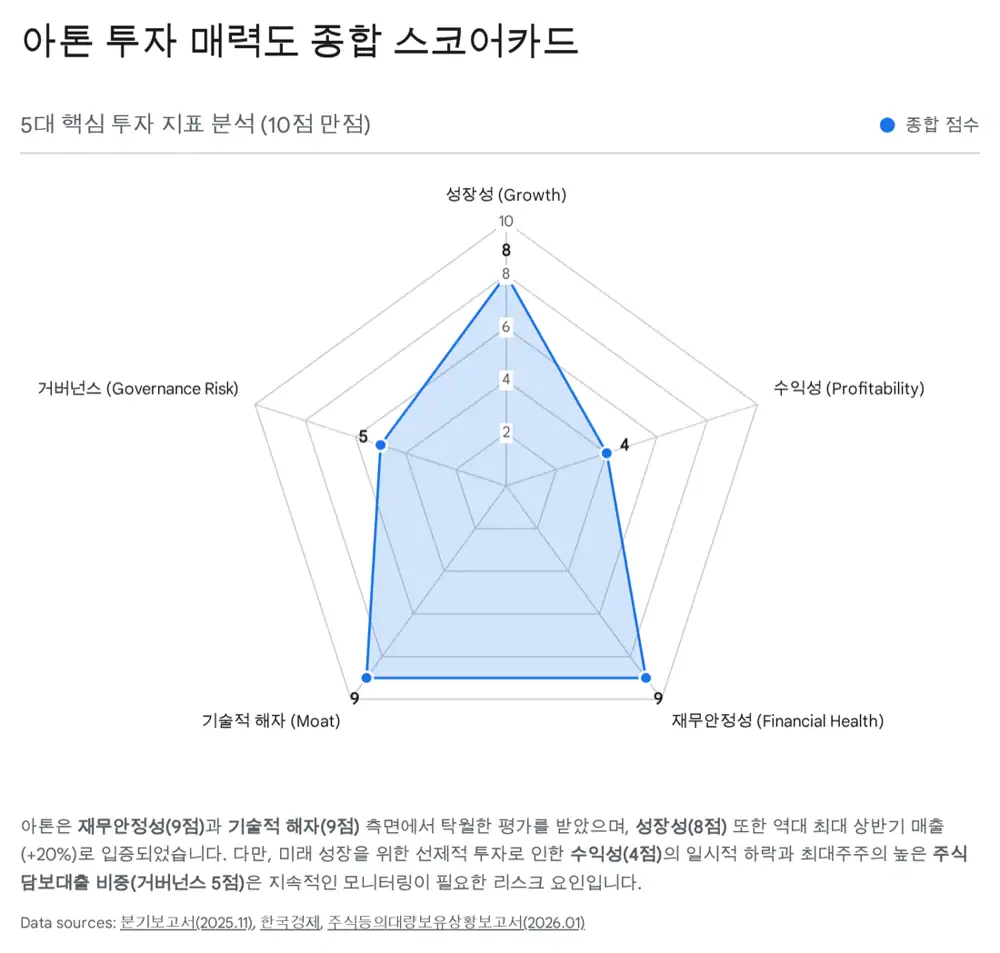

0. Bottom line first

My reading of ATON is straightforward. The core fintech-security solutions and PASS-based authentication platform are supported by regulatory change and financial-sector lock-in, but unrelated diversification and the controlling shareholder's high share-pledge ratio cap the valuation upside.

Regulation and switching cost

Security products such as mSafeBox, mOTP, and mPKI are embedded in tier-one bank mobile apps, making replacement costly and slow to validate.

PASS and next-generation finance

PASS certificates, CBDC, STO, AICC, and AI security monitoring can become recurring revenue and new infrastructure demand drivers.

Pledges and overhang

Kim Jong-seo has pledged 2,791,915 shares, or 48.4% of his holdings, and the KRW 5 billion fourth exchangeable bond can become future selling pressure.

Official fact: As of 3Q 2025, consolidated assets were KRW 140.9 billion, liabilities were KRW 32.6 billion, and equity was KRW 108.3 billion. After treasury-share cancellation, total issued shares declined to 24,482,092 as of January 19, 2026.

Interpretation: The balance sheet is strong, but without profit recovery and pledge reduction, regulatory tailwinds alone may not sustain a valuation re-rating.

1. Company Overview: Turning security media into software

ATON was founded in October 1999 to develop system software and has grown alongside Korea's financial IT market. It first supplied PC-based home trading systems to brokerages, then launched Korea's first mobile securities trading service in 2000 as the market shifted to mobile.

As smartphones moved finance onto mobile apps, ATON pivoted from a systems-integration vendor into a fintech-security specialist. I define its current identity as a company leading the dematerialization of security media: replacing physical OTP devices and security cards with software-based secure elements.

Official fact: ATON listed on KOSDAQ in October 2019. As of April 2025, Korea Enterprise Data rated ATON BBB, described as sound, and CR-2 for cash flow, also described as sound.

Interpretation: BBB still implies sensitivity to downturns or operating-environment deterioration, but CR-2 points to decent operating cash generation. In fintech security, maintenance revenue after initial deployment appears to support that cash flow.

| Item | Detail | Investment read |

|---|---|---|

| Founded | October 1999 | Long financial-IT reference base |

| Early business | HTS and Korea's first MTS in 2000 | Experience in the mobile transition of finance |

| Listing | KOSDAQ in October 2019 | Capital-market validation of technical credibility |

| Credit | BBB and CR-2 | Evidence of maintenance-style security cash flow |

| Subsidiaries | Seven unlisted subsidiaries at end-3Q 2025 | Manufacturing and mobility diversification must be monitored |

2. Business Model: Growth and discount from three pillars

ATON's portfolio has three pillars: fintech security solutions, fintech platforms, and smart finance plus other businesses. This structure provides both stability and optionality, but the other businesses can also blur the core-company valuation.

2.1 Fintech security solutions

The security-solution segment contributes roughly 30-36% of revenue and is close to ATON's core reason to exist. The key is software secure elements and white-box cryptography, which blends the encryption key into the algorithm so that memory dumping or reverse engineering does not easily reveal it.

- ATON mSafeBox: a software vault for securely storing and managing important information inside a smartphone.

- ATON mOTP: one-time passwords generated inside a smartphone app without a separate OTP device.

- ATON mPKI: a private-certificate solution replacing legacy public certificates with biometric authentication or PINs.

- Quantum SafeGuard: a next-generation solution applying post-quantum cryptography to respond to quantum-computing hacking threats.

Official fact: ATON solutions are embedded in major tier-one Korean banking apps, including KB Kookmin Bank, Shinhan Bank, and NH NongHyup Bank.

Interpretation: Financial-sector IT systems are conservative and costly to revalidate. Once a security solution is installed, replacement is difficult, creating a barrier that competitors such as RaonSecure and Dream Security cannot easily cross.

2.2 PASS platform

The fintech-platform business contributes about 16% of revenue. ATON operates electronic-signature services inside PASS, the identity-authentication app of SKT, KT, and LGU+. ATON handles planning, development, and operation of PASS certificates, while the telecom companies provide the user base. Certificate issuance and use generate fees that are shared between the telecoms and ATON.

Official fact: PASS certificates surpassed 50 million issuances as of 2023. The app is evolving into a daily-life platform by adding mobile driver's licenses, MyData services, and other features.

Interpretation: The platform direction is attractive, but it must compete with certificate ecosystems from Kakao, Naver, and Toss. ATON is responding by adding services such as stock-investment information and insurance recommendations inside PASS to raise ARPU.

2.3 Unrelated diversification

The hardest part of ATON is the other segment built through subsidiaries. At the end of 3Q 2025, ATON had seven unlisted subsidiaries, and HBE plus its lower-tier subsidiary DSE operate in electronic-equipment design and manufacturing. HBE's total assets were about KRW 20.8 billion as of 3Q 2025.

ATON Mobility provides used-car information services and development work, while Trackchain operates in digital assets. These businesses appear to be in an investment-before-profit stage. For now, I read them as more likely to dilute consolidated margins than to prove a new cash cow.

3. Financials and Funding: Strong balance sheet, weaker profitability

| Metric | Figure | Read-through |

|---|---|---|

| Total assets | KRW 140.9 billion | 3Q 2025 consolidated basis |

| Total liabilities | KRW 32.6 billion | Low debt burden |

| Total equity | KRW 108.3 billion | Base of financial stability |

| Debt-to-equity | About 30.1% | Top-tier stability |

| Current ratio | About 448% | Excellent short-term payment capacity |

| 1H 2025 revenue | KRW 36.7 billion, +20% YoY | Top-line growth |

| 1H 2025 operating profit | KRW 3.7 billion, -49% YoY | Profitability weakened by new-business costs |

ATON's financial stability is very strong. The point investors should not miss is profitability. Consolidated operating profit in 1H 2025 was KRW 3.7 billion, down 49% year on year. Spending on digital assets, AICC, R&D, and marketing can be framed as structural cost for future growth, but from my perspective the timing of return on investment has become less certain.

3.1 Meaning of the fourth exchangeable bond

Official fact: On November 28, 2025, ATON completed issuance of KRW 5 billion in fourth unregistered, unsecured private exchangeable bonds. The exchange target is ATON treasury stock.

- Issue amount: KRW 5 billion

- Exchange target: ATON treasury shares

- Interest rate: The source says the exact coupon and maturity yield are not specified, but given ATON's BBB credit rating and common EB issuance trends, it is likely to have been issued at a rate close to 0%.

- Use of proceeds: Operating funds and new-business investment capital, especially for AI security monitoring and overseas expansion.

Interpretation: Unlike CBs or BWs, EBs deliver treasury shares rather than newly issued shares, so total-share dilution is limited. The drawback is that treasury shares that could have been cancelled may re-enter the market, leaving an overhang risk.

Official fact: Total issued shares were 24,850,529 as of September 30, 2025, and declined to 24,482,092 as of January 19, 2026 after treasury-share cancellation.

4. Governance Risk: Pressure created by pledged shares

The area where I take the most conservative stance is the controlling shareholder's share management. According to the large-shareholding report filed on January 19, 2026, CEO Kim Jong-seo has pledged 2,791,915 of his 5,768,160 shares to financial institutions, or 48.4% of his holdings.

| Counterparty | Pledged shares | Borrowing | Maintenance ratio | Risk |

|---|---|---|---|---|

| Korea Securities Finance | 2.26 million shares | KRW 6.5 billion | 110% | Additional collateral burden if the stock falls sharply |

| Woori Investment & Securities | 531,915 shares | KRW 2.5 billion | 150% | Sensitive to volatility, possible forced-sale trigger |

| Total | 2,791,915 shares | About KRW 9 billion | 48.4% of holdings | Management pressure to defend the share price |

The combined stake of the largest shareholder and related parties is 31.16%, enough for control. However, the high pledge ratio creates both forced-sale risk in a selloff and pressure to support the share price in the short term.

Interpretation: Shareholder returns such as treasury-share cancellation can be positive, but share-price management without fundamental improvement can damage long-term value. I treat pledge reduction by the controlling shareholder as a core risk indicator.

5. Regulation and Growth: MLS, CBDC, STO, overseas expansion

The Korean government is moving away from a uniform physical network-separation regime maintained for the past decade and is pursuing multi-level security, or MLS, where security levels differ by data importance.

- MLS and Zero Trust: Under MLS, lower-importance business networks may use logical separation rather than physical separation, making mSafeBox-like secure media a potential Zero Trust component.

- CBDC and STO: Participation in the Bank of Korea's CBDC pilot, Project Han River, and token-securities infrastructure projects suggests ATON can pre-position itself as a security partner in blockchain-based financial infrastructure.

- Global expansion: ATON has supplied solutions to six countries, including Vietnam, Indonesia, and Japan. Southeast Asia has rapid mobile-banking adoption but weaker security infrastructure, creating demand for app-update-based software security.

6. Competition and Investment Strategy

In Korea's fintech-security market, competitors include RaonSecure, Dream Security, and SGA Solutions. The source frames RaonSecure as strong in biometrics, Dream Security in PKI and quantum cryptography, and SGA Solutions in server security.

Secure Element

ATON has built a distinct area around virtualized security media, with an economic benefit for banks by reducing physical security-device issuance costs.

Authentication, PKI, server security

Many competitors specialize in PC-based security or specific authentication methods, so competitive intensity differs by domain.

Telecoms and big tech

The PASS business depends heavily on telecom partners and must compete for share against Kakao and Naver certificates.

In sum, ATON can be viewed as a hidden champion in Korean fintech security. The technical entry barriers and balance sheet are strong. From an institutional-investor viewpoint, however, three issues need confirmation.

- Whether the controlling shareholder reduces excessive pledged-share borrowing: the core management-risk trigger.

- Visibility of unrelated-subsidiary earnings: whether manufacturing and other businesses increase consolidated volatility or become cash generators.

- Speed of profit recovery: the J-curve timing for new-business investment to convert into profit likely requires a longer horizon beyond 2026.

Interpretation: I read the current share price as balancing expectations for concrete MLS policy benefits against overhang risk. My key monitoring indicators are the timing of detailed MLS policy, EPS improvement after treasury-share cancellation, and reduction of controlling-shareholder pledges.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157581724

- AI Matters: https://aimatters.co.kr/news-report/ai-news/21081/

- Korea Economic Daily: https://www.hankyung.com/article/202508141707O

- Digital Daily: https://www.ddaily.co.kr/m/page/view/2024091917353184880

- Chosun Biz: https://biz.chosun.com/it-science/ict/2024/06/08/OVRZBWEAPRDOJH66WKSQWQXF5M/