DEEP RESEARCH · LG ELECTRONICS B2B

LG Electronics B2B Pivot: Profit Inversion and AI-Infrastructure Rerating

An analysis of how vehicle components, HVAC, webOS, and subscriptions can change the household-appliance frame.

0. Bottom line first

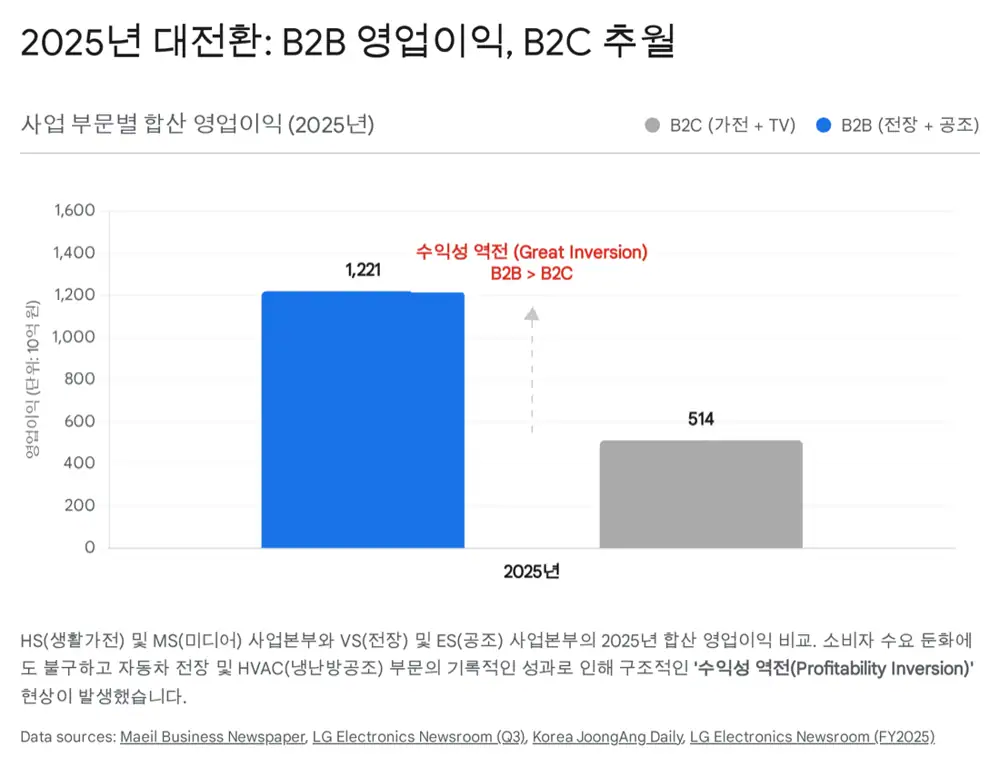

I read 2025 as the year LG Electronics began to be judged less as a cyclical appliance maker and more as a B2B industrial-infrastructure company. The evidence is the profit inversion: VS and ES profits surpassed HS and MS by a wide margin.

B2B profit leadership

The source estimates VS+ES operating profit at about KRW 1.221 trillion versus about KRW 514 billion for HS+MS.

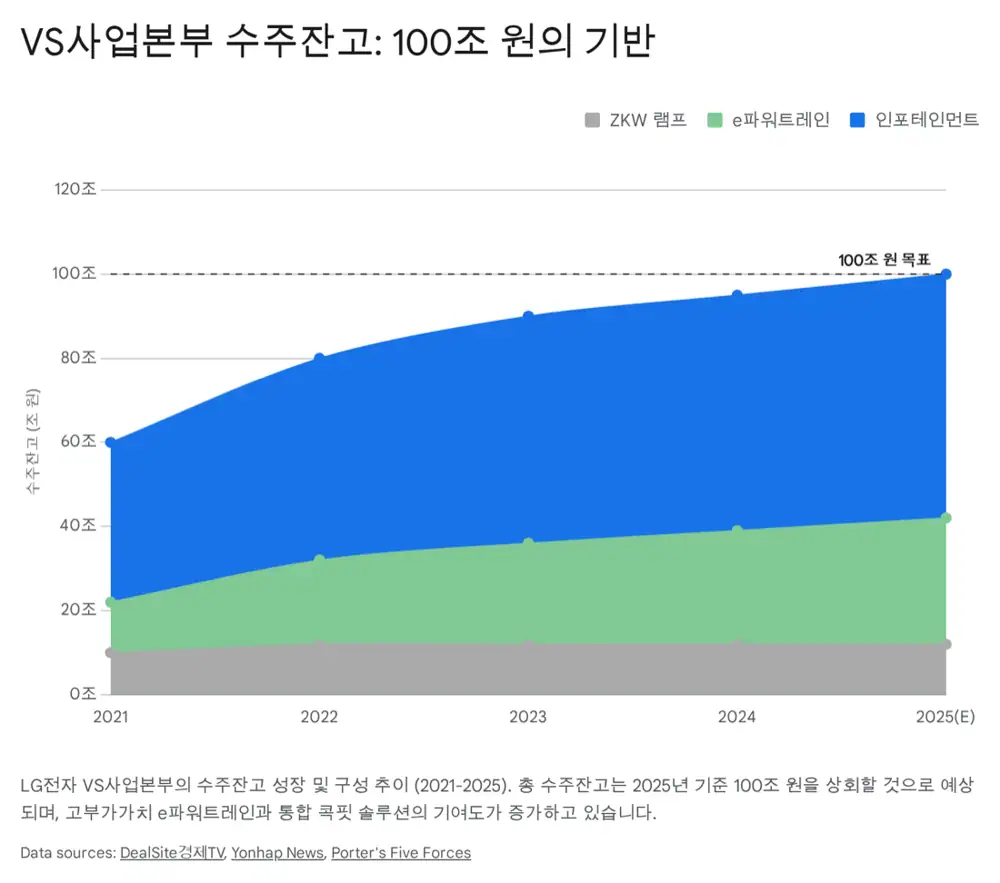

KRW 100 trillion auto backlog

VS backlog is described as clearly above KRW 100 trillion at end-2025, equal to about 7-8 years of work.

Data-center thermal management

ES is positioned around chillers and immersion cooling for the power and heat bottleneck in AI data centers.

1. 2025 earnings: weak surface, changing structure

Official fact: The source states that 2025 consolidated revenue was KRW 89.2025 trillion, a second consecutive record year. Operating profit was KRW 2.478 trillion, down 27.5% year over year, and 4Q 2025 posted a KRW 109.4 billion operating loss, the first quarterly loss in nine years.

Interpretation: The headline profit decline looks negative, but the source frames it as transition pain from estimated severance costs of KRW 300-400 billion, logistics and tariff costs, and TV marketing pressure. The more important question is where profit quality has moved.

| Item | 2025 source figure | Meaning |

|---|---|---|

| Consolidated revenue | KRW 89.2025 trillion | Second consecutive record revenue year |

| Operating profit | KRW 2.478 trillion | Down 27.5% year over year |

| 4Q operating loss | KRW 109.4 billion | First quarterly loss in nine years |

| VS+ES operating profit | About KRW 1.221 trillion | VS about KRW 547 billion + ES about KRW 674 billion |

| HS+MS operating profit | About KRW 514 billion | B2B profit more than doubled B2C profit |

2. Triple 7 and platformization: from manufacturing to recurring revenue

Official fact: The source says LG Electronics has set a “Triple 7” target for 2030: 7% CAGR, 7% operating margin, and 7x EV/EBITDA. Subscription revenue grew from KRW 1.1341 trillion in 2024 to about KRW 2 trillion in 2025, up more than 75%, while webOS platform revenue surpassed KRW 1 trillion.

Interpretation: Subscriptions and webOS are what can break the low-multiple manufacturing frame. When appliances and TVs add care, content, and advertising revenue, the valuation argument changes alongside the B2B pivot.

3. VS division: quality inside the KRW 100 trillion backlog

Official fact: The source states that the VS division achieved record revenue and operating profit in 2025 and that its 3Q operating margin exceeded 5%. It also says the end-2025 order backlog clearly exceeded KRW 100 trillion, equal to 7-8 years of secured work.

| Segment | Estimated share | Growth driver |

|---|---|---|

| Infotainment IVI | About 60-70% | Global No. 1 in telematics, P-OLED digital cockpit demand, higher-margin software integration |

| e-Powertrain | About 20-25% | LG Magna JV, EV motors/inverters/converters, large North American and European OEM awards |

| Automotive lighting ZKW | About 15% | High-value headlamps for BMW, Mercedes-Benz, and other premium OEMs |

For the SDV transition, the source frames LG as a Tier-0.5 technical partner rather than just a Tier-1 supplier. The main components are AlphaWare, webOS for Auto, and cross-domain controllers.

- AlphaWare: SDV software solution that separates hardware and software for OTA updates and post-sale monetization.

- webOS for Auto: extension of the TV operating system into vehicles, turning cars into content platforms.

- xDC: integrated control hardware using platforms such as Snapdragon Ride to combine IVI and ADAS functions.

4. ES division: targeting the AI data-center cooling bottleneck

Official fact: The source states that about 40% of data-center power consumption is used for cooling. LG targets AI chip heat through oil-free magnetic-bearing chillers, immersion cooling, and direct-to-chip thermal-management solutions.

Oil-free magnetic bearing

A high-end chiller technology that removes bearing friction to improve energy efficiency.

Immersion cooling

Partnerships with SK Enmove for coolant and GRC for tanks target the next-generation cooling market.

Big-tech orders

The source references a multi-billion-dollar annual cooling-infrastructure supply deal with Microsoft and a Jakarta AI data-center win.

| Item | LG Electronics | Global peers | Advantage |

|---|---|---|---|

| Core tech | Inverter scroll, magnetic-bearing chiller | Turbo and screw chillers | Appliance-derived motor and compressor-control know-how |

| AI response | Immersion cooling/DTC vertical integration | Legacy air-cooling infrastructure | Challenger advantage from less legacy baggage |

| Manufacturing base | Korea, China, India, and other Asian bases | U.S. and Europe centered | Cost and access advantages in Asian data-center markets |

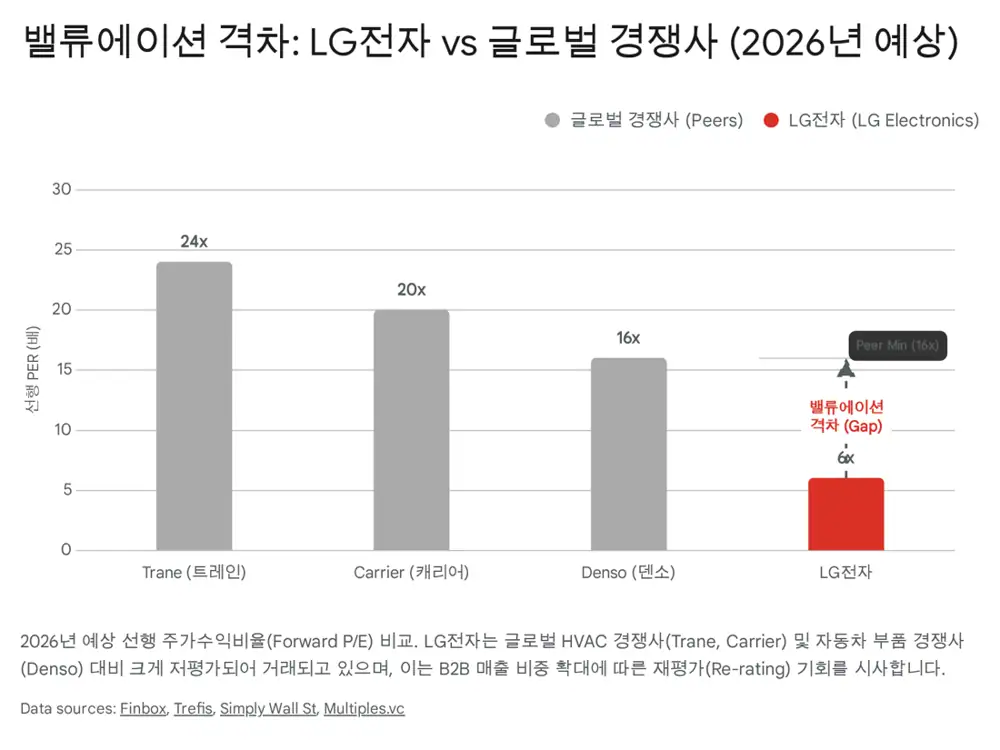

| Valuation | P/E 5-7x | Trane/Carrier P/E 20-25x | Rerating room if competing in the same market |

5. One LG, risks, and rerating

The source describes LG Electronics’ edge not as a standalone company but as a vertically integrated “One LG” ecosystem that includes LG Innotek and LG CNS. LG Innotek provides camera modules, LiDAR components, and precision motors for autonomous-driving and ADAS sensing and actuation, while LG CNS adds DCIM and AI-optimization software for data-center turnkey solutions.

Official fact: The source compares LG Electronics at a 2026 expected P/E of 5-7x with Trane and Carrier at 20-25x, and Denso and Magna at 10-15x. It lists U.S. protectionism and tariffs, a prolonged EV demand slowdown, and low-price Chinese competition as key risks.

Interpretation: I see the core question not as simply “is it cheap?” but “what will the market classify it as?” If investors keep seeing LG only as an appliance company, the discount can persist. If profit leadership hardens in VS, ES, and platforms, some industrial and platform multiple can start to show up.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224157347784

- Source 2: https://www.mk.co.kr/en/business/11939282

- Source 3: https://www.lgcorp.com/media/release/28020

- Source 4: https://www.lg.com/global/newsroom/news/corporate/lg-electronics-releases-preliminary-earnings-for-fourth-quarter-and-full-year-2025/

- Source 5: https://live.lge.co.kr/2601-lg-2025sales/

- Source 6: https://www.greenpostkorea.co.kr/news/articleView.html?idxno=305804

- Source 7: https://www.mk.co.kr/en/business/11928063

- Source 8: https://koreajoongangdaily.joins.com/news/2025-10-13/business/industry/LG-Electronics-operating-profit-down-yearonyear-but-better-than-expectations/2418910

- Source 9: https://www.lg.com/au/about-lg/press-and-media/lg-ceo-william-cho-highligts-consistent-progress-towards-future-/

- Source 10: https://www.lg.com/global/mobility/media-center/press-release/20250108-company-lg-ceo-press-2025-strategy-ces2025

- Source 11: https://www.alphaspread.com/security/krx/066570/investor-relations/earnings-call/q3-2025

- Source 12: https://www.lg.com/th/about-lg/press-media/lg_electronics_3Q_2025_earnings_release_en/

- Source 13: https://news.dealsitetv.com/articles/122981

- Source 14: https://www.yna.co.kr/view/AKR20230629017400003

- Source 15: https://portersfiveforce.com/blogs/growth-strategy/lge

- Source 16: https://www.lg.com/global/newsroom/news/corporate/lg-releases-preliminary-earnings-for-third-quarter-2025/

- Source 17: https://www.lg.com/global/newsroom/news/vehicle-component-solutions/lg-to-present-insights-into-software-defined-vehicles-at-autotech-detroit/

- Source 18: https://www.lg.com/global/mobility/media-center/event/driving-vision-for-the-future-2030

- Source 19: https://www.lg.com/global/newsroom/insights/executive-corner/executive-corner-webos-powering-our-next-growth-chapter/

- Source 20: https://straitsresearch.com/report/software-defined-vehicle-market

- Source 21: https://www.ajupress.com/view/20260119160428212

- Source 22: https://www.kedglobal.com/electronics/newsView/ked202411200005

- Source 23: https://www.lg.com/global/business/hvac/commercial-solutions/chiller/oil-free-magnetic-bearing-centrifugal-chiller/

- Source 24: https://www.lgcorp.com/media/release/29509

- Source 25: https://enkiai.com/ai-market-intelligence/lgs-2025-ai-data-center-cooling-dominance-revealed

- Source 26: https://introl.com/blog/lg-microsoft-cooling-partnership-ai-data-centers-january-2026

- Source 27: https://www.koreaherald.com/article/10526932

- Source 28: https://www.lg.com/global/business/insights/hvac/news/lg-expands-ai-infrastructure-footprint-across-asia/

- Source 29: https://www.trefis.com/stock/jci/articles/581658/trane-technologies-vs-johnson-controls-international-which-is-the-stronger-buy-today/2025-11-06

- Source 30: https://finbox.com/KOSE:A066570/explorer/pe_ltm/

- Source 31: https://drive.google.com/open?id=1GeVVSntVqkXXC4Bgt0BhIN2A5k5s40rEyWZhrdswcUY

- Source 32: https://drive.google.com/open?id=1a9UtFUTnmetJyYAqxumwP7ZZStYnEZennBQScoWT06Q

- Source 33: https://www.lgcorp.com/media/release/29539

- Source 34: https://securities.miraeasset.com/bbs/download/2141888.pdf?attachmentId=2141888

- Source 35: https://multiples.vc/public-comps/lg-valuation-multiples