DEEP RESEARCH · Asset Allocation

2026 Commodities Outlook: From Gold to Energy

A liquidity-lagged commodity-cycle summary based on material from Daishin Securities analyst Choi Jin-young

0. Bottom Line First

The core message is that it is not yet time to argue for a bubble collapse, and that commodities lag liquidity, especially gold prices, by 18-20 months. The main commodity cycle is therefore expected around the U.S. midterm-election period.

1. Macro View

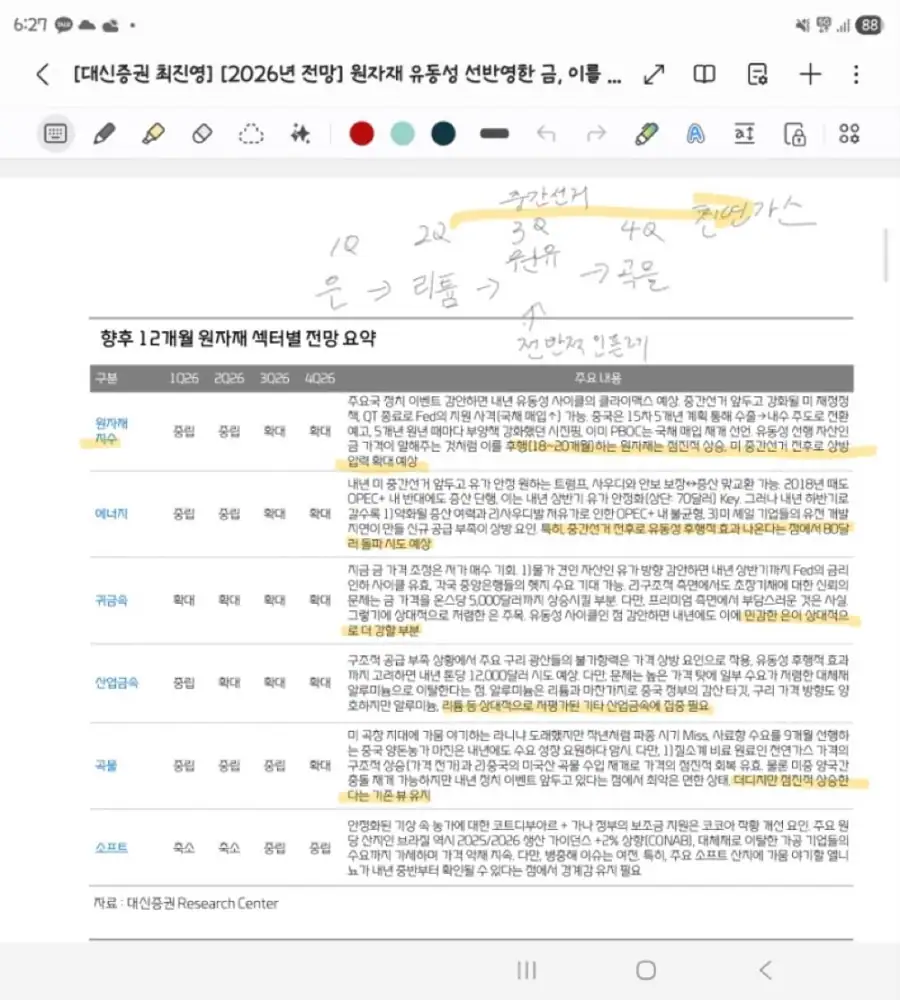

Official fact: The source shares the URL for Daishin Securities commodity analyst Choi Jin-young’s annual outlook, “From Gold to Energy, Commodities Following Liquidity” dated November 11.

Interpretation: The view assumes that both the U.S. and China may strengthen stimulus ahead of political events. On that basis, equities are still viewed as attractive, while commodity-driven stagflation concerns are pushed out toward next year’s U.S. midterm-election period.

2. Sector Preference

Precious Metals + Copper

Gold is viewed as a buy-on-dip opportunity, but the table of contents points to a stronger preference for silver. Copper should be read alongside mine disruptions and aluminum competition.

Energy + Other Industrial Metals

The oil view is that there will be no low oil price in the USD 40 range, while natural gas should be watched for structural growth in the second half of next year.

Grains

The contents mention a U.S.-China truce and China resuming U.S. imports, suggesting the worst may have passed.

3. Checklist from the Material’s Table of Contents

- Part 1 Macro: Trump needing stimulus, China returning to domestic-demand stimulus, and gold prices as a preview of commodity-index gains.

- Part 2 Energy: Saudi Arabia’s production-increase stance and downside defenses, possible re-emergence of Russia-Ukraine war-end discussions, and second-half structural growth in natural gas.

- Part 3 Precious metals: Gold is good, but the view prefers silver more.

- Part 4 Industrial metals: Other industrial metals may become stronger than copper; aluminum production restrictions and lithium production cuts are key topics.

- Part 5 Agriculture: China resuming U.S. imports and the possibility that the worst has passed for grains.