DEEP RESEARCH · COSMECCA KOREA

Cosmecca Korea: OGM Shift and the Indie Brand Supercycle

A 2026 growth scenario through Korea, U.S., and China operations and OGM platform strength

0. Bottom Line First

My read is that Cosmecca Korea is evolving from a simple ODM into an OGM platform that solves global regulation, local trends, production, and quality in one package. As indie brands take over global channels, manufacturing, compliance, and development capability become more valuable.

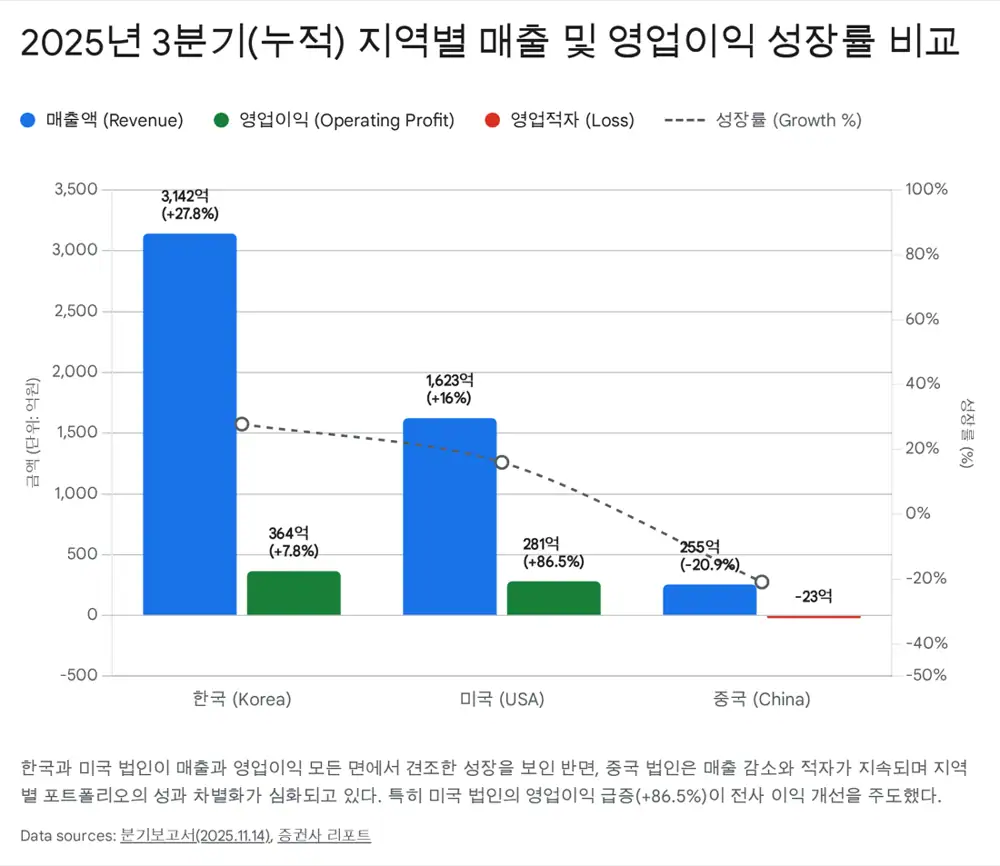

- Cumulative 3Q 2025 consolidated revenue was KRW 462.5bn, up 16.8% year on year.

- 3Q standalone operating profit was KRW 27.2bn, up 78.8% year on year; cumulative operating profit was KRW 62.5bn, up 32.9%.

- Cumulative OPM was 13.5%, with Korea as the growth base, the U.S. as the profit engine, and China as the restructuring case.

- The source expects 2026 consolidated revenue of KRW 719.0bn and operating profit of KRW 101.6bn, and views 11-12x forward PER as undervalued.

1. Industry Shift and the Meaning of OGM

The key change in global cosmetics in the mid-2020s is the breakup of brand power and the revaluation of manufacturing capability. Instead of legacy brands such as L'Oreal, Estee Lauder, and Amorepacific, indie brands rising through TikTok, Instagram Reels, and Amazon are gaining power.

Official fact: Cosmecca Korea presents OGM, or Original Global Standard and Good Manufacturing, as its own model beyond OEM and ODM. OGM covers country-specific channel analysis, regulatory review such as U.S. MoCRA and China NMPA, and local-trend product planning.

Interpretation: For indie brands with little capital and no factories, an OGM partner is survival infrastructure rather than a subcontractor. That can raise the manufacturer's bargaining power.

2. 3Q 2025 Results: Growth with Quality

| Item | 3Q 2024 cumulative | 3Q 2025 cumulative | YoY | Driver |

|---|---|---|---|---|

| Consolidated revenue | KRW 396.0bn | KRW 462.5bn | +16.8% | More global indie-brand orders |

| Korea revenue | KRW 245.9bn | KRW 314.2bn | +27.8% | Export volume from high-growth indie brands such as d'Alba |

| U.S. revenue | KRW 139.9bn | KRW 162.3bn | +16.0% | Englewood Lab OTC suncare and turnkey orders |

| China revenue | KRW 32.2bn | KRW 25.5bn | -20.9% | Weak Chinese consumption and local-brand competition |

| Consolidated operating profit | KRW 47.0bn | KRW 62.5bn | +32.9% | Operating leverage and high-margin mix |

| U.S. operating profit | KRW 15.1bn | KRW 28.1bn | +86.5% | Core profit engine |

| Net income | KRW 37.4bn | KRW 42.4bn | +13.2% | Better non-operating balance and controlled financing costs |

The source attributes margin improvement to more than fixed-cost leverage: a richer mix of functional skincare and suncare, high-margin FDA OTC suncare projects at Englewood Lab, and factory automation/smart-factory efficiency in Korea.

Official fact: As of 3Q 2025, basic and color cosmetics product revenue was KRW 457.3bn, or 98.9% of total revenue. Debt ratio was 96.50%, up from 68.36% at end-2024, while cash and cash equivalents were KRW 58.7bn and short-term financial products were KRW 9.0bn.

3. Regional Roles: Korea Growth, U.S. Profit, China Restructuring

Global Indie Brand Hub

Korea accounts for about 67.9% of total revenue. 3Q 2025 revenue was KRW 129.8bn, up 57.4% year on year.

OTC Suncare Profit Engine

Englewood Lab posted 3Q 2025 revenue of KRW 61.8bn (+50.3% YoY) and operating profit of KRW 13.2bn (+224.9% YoY).

Profit-Focused Restructuring

China posted 3Q 2025 revenue of KRW 8.1bn (-12.8% YoY) and targets BEP in 2026.

Korea's key customers include K-beauty indie brands such as d'Alba and Beauty of Joseon. d'Alba Global recorded cumulative 3Q 2025 revenue of KRW 359.5bn (+59% YoY), and its overseas sales share rose from 45.6% in 2023 to 61.6% in 3Q 2025.

In the U.S., sunscreen is treated as an OTC drug rather than a cosmetic, requiring FDA cGMP. Englewood Lab Korea received a VAI grade from the FDA in 2019, and as MoCRA raises entry barriers, it becomes a core partner for brands entering North America. Turnkey share was about 70.7% in 3Q 2025.

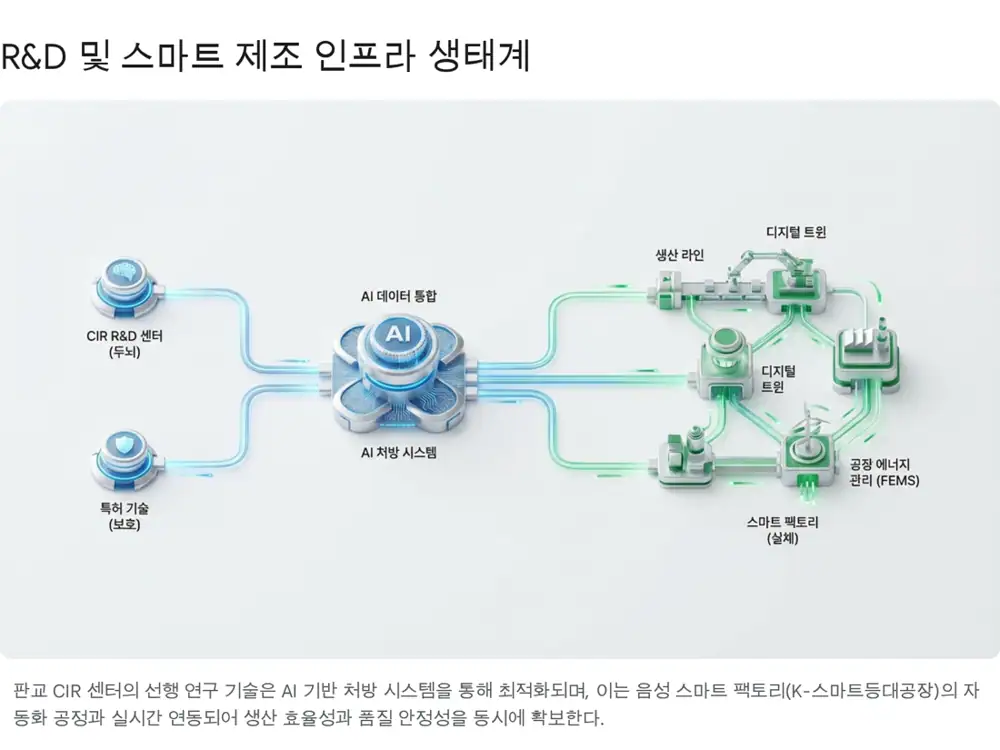

4. Technology and Customer Ecosystem

Official fact: The source says more than 30% of all employees are researchers, R&D spending is 2.7% of sales, or about KRW 12.6bn as of 3Q 2025, and registered patents totaled about 890 in Korea and overseas.

- The 2022 K-smart lighthouse factory project applied AI and digital twin technology to production lines.

- The company obtained MUI halal certification in February 2025 and ISO37301 compliance-management certification in October 2025.

- Technology points include the industry's first triple-functional BB cream, exosome-liposome hybrid systems, and silica technology to maximize sunscreen efficiency.

- AI-based similar-formula search patents and PLM support fast SKU development.

- No single external customer exceeded 10% of sales as of 3Q 2025, supporting the diversification argument.

5. 2026 Outlook and Valuation

The source sees 2026 as the year Cosmecca becomes a global top-tier OGM company. Based on research from firms including NH Investment & Securities, it cites 2026 consolidated revenue of KRW 719.0bn, up about 16% from the 2025 estimate, and operating profit of KRW 101.6bn, up 21%.

| Item | Source outlook | Basis |

|---|---|---|

| 2026 revenue | KRW 719.0bn | U.S. offline channels, Amazon, and indie-brand orders |

| 2026 operating profit | KRW 101.6bn | High-margin suncare, turnkey expansion, China restructuring |

| Forward PER | About 11-12x | Compared with Korea Kolmar/Cosmax at 15-20x and overseas ODM/OEM peers above 20x |

| Target-price range | KRW 92,000-115,000 | Interpreted as roughly 30-60% upside from the then-current price |

The source also includes this additional reference marker, preserved as a working link: http://googleusercontent.com/assisted_ui_content/4.

6. Risks and Final View

- If China restructuring is delayed or domestic consumption remains weak, group margin improvement could be capped. The source argues the impact is limited because China revenue share has already fallen to the 5% range.

- Higher prices for sunscreen ingredients such as Tinosorb and plastic containers can pressure cost of goods.

- Escalating U.S.-China friction could disrupt China operations or raw-material sourcing, making supply-chain diversification and more U.S. local production important.

Cosmecca Korea is moving from hidden K-beauty helper to a production, compliance, and R&D platform for global beauty. I will keep tracking Englewood Lab's turnkey share, suncare orders, China BEP timing, and whether single-customer exposure stays below 10%.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224156610893

- 구글 어시스트 콘텐츠 링크: http://googleusercontent.com/assisted_ui_content/4

- 달바글로벌 투자 분석 보고서: https://drive.google.com/open?id=1tvYU7CRUjyUfacUZaO7re8LVRztybgz3BwbCjkh8-_g

- 비즈니스포스트, 코스메카코리아 뷰티 ODM 3강: https://www.businesspost.co.kr/BP?command=article_view&num=408795

- 조선비즈, 2026년 최대 실적 전망 특징주: https://biz.chosun.com/stock/stock_general/2025/12/05/UFQTQH4LNNGRVOICPSM73V2ERQ/

- 뷰티누리, 잉글우드랩 3분기 매출 627억: https://www.beautynury.com/news/view/109800/cat/10

- 조선비즈, NH증권 코스메카코리아 전망: https://biz.chosun.com/stock/stock_general/2025/12/05/XVD6USQPGNCHVJHC63NRCZPGLA/

- 미래에셋증권 Cosmecca Korea 자료: https://securities.miraeasset.com/bbs/download/2137145.pdf?attachmentId=2137145

- 약업신문, 잉글우드랩 3분기 매출: http://m.yakup.com/news/index.html?mode=view&cat=12&nid=318883

- Fintel, Cosmecca Korea: https://fintel.io/s/kr/241710

- 한화투자증권 코스메카코리아 리포트: https://www.hanwhawm.com/main/common/common_file/fileView.cmd?category=2&depth3_id=anls1&key1=64975&key2=1&bldid=bbs10031