DEEP RESEARCH · COSMECCA KOREA

Cosmecca Korea: OGM Transition and the Indie-Brand Supercycle

A review of Korea, US, and China performance, Englewood Lab's OTC moat, and the 2026 KRW 1tn market-cap thesis.

0. Bottom line first

The core point is that Cosmecca Korea is not just an ODM. It is an OGM platform that helps indie brands solve planning, development, production, quality, and regulatory issues when entering global markets.

Official fact: Q3 2025 cumulative consolidated revenue was KRW 462.5bn, up 16.8% year over year, and Q3 standalone-quarter operating profit was KRW 27.2bn, up 78.8%. Q3 cumulative operating profit was KRW 62.5bn and OPM was 13.5%.

Interpretation: I think the 2026 thesis of KRW 700bn revenue and KRW 100bn operating profit works if Korean indie-brand exports, Englewood Lab's OTC sunscreen orders, and China restructuring benefits align at the same time.

1. Industry change and OGM positioning

The source frames the mid-2020s global cosmetics shift as the dismantling of brand power and the rediscovery of manufacturing capability. Indie brands rising through TikTok, Instagram Reels, and Amazon often lack their own manufacturing facilities, so ODM/OGM partners that handle fast planning and global regulatory response become more valuable.

Official fact: Cosmecca Korea presents OGM, Original Global Standard and Good Manufacturing, beyond traditional OEM/ODM. The source explains it as a total solution covering country-specific distribution analysis, regulatory review such as US MoCRA and China NMPA, and product planning suited to local trends.

- The 2018 acquisition of Englewood Lab secured a North American production base.

- The 2022 K-Smart Lighthouse Factory selection by the Ministry of SMEs and Startups supported production-process digital transformation.

- The Pangyo CIR Center is presented as a global R&D hub connecting Korea, US, and China production bases.

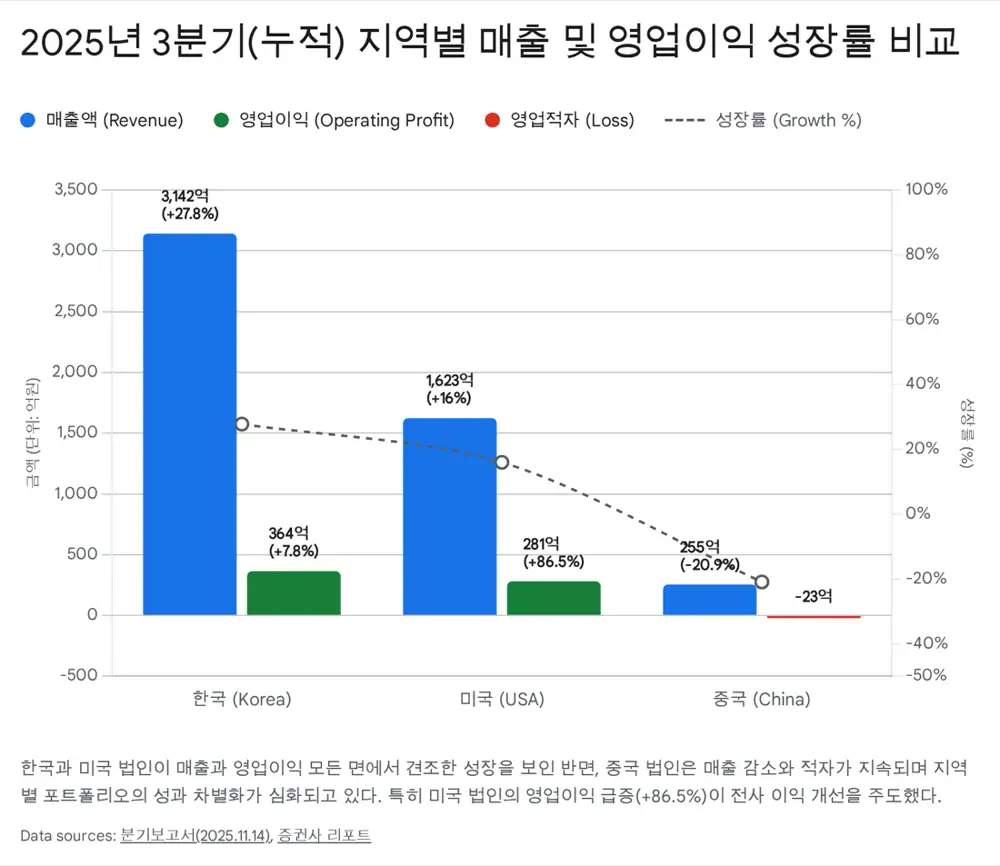

2. Q3 2025 performance

| Category | 2024 Q3 cumulative | 2025 Q3 cumulative | YoY | Core driver |

|---|---|---|---|---|

| Consolidated revenue | KRW 396.0bn | KRW 462.5bn | +16.8% | More global indie-brand orders |

| Korea revenue | KRW 245.9bn | KRW 314.2bn | +27.8% | Export volume surge from d'Alba and other indie brands |

| US revenue | KRW 139.9bn | KRW 162.3bn | +16.0% | Englewood Lab OTC sunscreen and turnkey orders |

| China revenue | KRW 32.2bn | KRW 25.5bn | -20.9% | Weak domestic consumption and local competition |

| Consolidated operating profit | KRW 47.0bn | KRW 62.5bn | +32.9% | Operating leverage and higher-margin product mix |

| Korea operating profit | KRW 33.8bn | KRW 36.4bn | +7.8% | Stable profit generation |

| US operating profit | KRW 15.1bn | KRW 28.1bn | +86.5% | Core engine of group profit growth |

| China operating profit/loss | KRW -0.4bn | KRW -2.3bn | Loss continues | Restructuring cost and lower utilization |

| Net income | KRW 37.4bn | KRW 42.4bn | +13.2% | Non-operating improvement and controlled finance costs |

Official fact: As of Q3 2025, basic and color cosmetics product revenue was KRW 457.3bn, 98.9% of total revenue. The source attributes profitability improvement to higher functional skincare and sun-care mix, Englewood Lab's high-margin OTC projects, and smart-factory conversion.

3. Financial soundness and regional strategy

Official fact: The debt ratio at the end of Q3 2025 was 96.50%, up from 68.36% at the end of 2024. The source interprets this as raw-material procurement for rising orders, higher payables, and strategic use of short-term borrowings rather than simple deterioration.

Official fact: Cash and cash equivalents were KRW 58.7bn and short-term financial instruments were KRW 9.0bn. Borrowings are presented as KRW 130.8bn short term and KRW 30.7bn long term.

Growth in Korea

Korea accounts for about 67.9% of company revenue. Q3 2025 Korea revenue is presented as KRW 129.8bn, up 57.4% year over year.

Profit in the US

Englewood Lab posted Q3 2025 revenue of KRW 61.8bn and operating profit of KRW 13.2bn, up 50.3% and 224.9% respectively.

Restructuring in China

Q3 2025 China revenue was KRW 8.1bn, down 12.8%. Production concentration around the Pinghu plant and local-brand targeting aim at 2026 BEP.

4. US OTC moat and R&D capability

In the US, sunscreen is treated as an OTC drug rather than a cosmetic, requiring FDA cGMP standards. The source says Englewood Lab Korea received an FDA VAI grade in 2019 and that MoCRA has raised entry barriers further.

- Turnkey mix: about 70.7% as of Q3 2025. Turnkey work covering container sourcing, filling, and packaging has higher margins than simple filling.

- Certifications: MUI halal certification in February 2025 and ISO37301 compliance-management certification in October are mentioned.

- R&D staff: more than about 30% of all employees are research staff.

- R&D investment: 2.7% of revenue in Q3 2025, about KRW 12.6bn.

- Patents: about 890 registered domestic and overseas patents at the end of Q3 2025.

Official fact: The source presents the first triple-functional BB cream, exosome-liposome hybrid system, silica manufacturing technology for stronger sunscreen efficiency, an AI-based similar-formula search system, and PLM as technology strengths.

5. Indie-brand ecosystem and the d'Alba case

d'Alba is presented as the clearest example of how Cosmecca Korea's OGM capability grows together with customer growth. d'Alba Global uses Italian white truffle as brand identity and outsources production under an asset-light strategy.

Official fact: The source says d'Alba Global recorded Q3 2025 cumulative revenue of KRW 359.5bn, up 59% year over year. d'Alba's overseas revenue mix rose from 45.6% in 2023 to 61.6% in Q3 2025.

Interpretation: If Cosmecca Korea develops and produces core d'Alba products such as mist serum, d'Alba can focus on marketing and branding while Cosmecca participates in the export-volume increase. The fact that no single external customer exceeded 10% of revenue in Q3 2025 also points to customer diversification.

6. 2026 outlook and valuation

The source presents the possibility that Cosmecca Korea exceeds KRW 700bn in revenue and KRW 100bn in operating profit in 2026. Based on major institutional analysis, it expects 2026 consolidated revenue of KRW 719.0bn and operating profit of KRW 101.6bn, about +16% and +21% versus 2025 estimates.

- US growth: expansion into offline channels such as Sephora and Ulta Beauty, plus Amazon's online strength, could lift Englewood Lab's order backlog.

- Sun care: OTC-compliant inorganic, organic, and hybrid sunscreen orders are presented as high-margin categories.

- China recovery: the key is whether restructuring completed through 2025 leads to 2026 BEP and profit contribution.

The source also contains an auxiliary material link, preserved here: http://googleusercontent.com/assisted_ui_content/4

| Valuation item | Source content |

|---|---|

| Current 12-month forward PER | About 11-12x |

| Domestic peer multiple | Kolmar Korea and Cosmax typically 15-20x |

| Overseas ODM/OEM average | PER above 20x |

| Broker target prices | KRW 92,000-115,000 |

| Upside | About 30-60% versus current price |

| Market-cap thesis | KRW 1tn in visible range |

7. Risks

- China market: delayed restructuring or prolonged domestic-consumption weakness could slow margin improvement. The source sees the group impact as limited because China's revenue mix has already fallen to the 5% range.

- Raw materials: higher prices for UV-filter ingredients such as Tinosorb and plastic containers can pressure costs. The source says bulk purchasing and OGM contract structures can hedge this.

- Geopolitics: US-China tension can affect China operations and sourcing; supply-chain diversification and higher US local production are the response.

8. My conclusion

Cosmecca Korea is a platform that absorbs global K-beauty indie-brand growth through manufacturing, regulation, and R&D. For 2026, I would focus on Englewood Lab turnkey and OTC sunscreen orders, Korean indie-brand order growth, China BEP conversion, and whether an 11-12x PER can be re-rated as a global OGM platform.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224156248248

- Source 2: http://googleusercontent.com/assisted_ui_content/4

- Source 3: https://drive.google.com/open?id=1tvYU7CRUjyUfacUZaO7re8LVRztybgz3BwbCjkh8-_g

- Source 4: https://www.businesspost.co.kr/BP?command=article_view&num=408795

- Source 5: https://biz.chosun.com/stock/stock_general/2025/12/05/UFQTQH4LNNGRVOICPSM73V2ERQ/

- Source 6: https://www.beautynury.com/news/view/109800/cat/10

- Source 7: https://biz.chosun.com/stock/stock_general/2025/12/05/XVD6USQPGNCHVJHC63NRCZPGLA/

- Source 8: https://securities.miraeasset.com/bbs/download/2137145.pdf?attachmentId=2137145

- Source 9: http://m.yakup.com/news/index.html?mode=view&cat=12&nid=318883

- Source 10: https://fintel.io/s/kr/241710

- Source 11: https://www.hanwhawm.com/main/common/common_file/fileView.cmd?category=2&depth3_id=anls1&key1=64975&key2=1&bldid=bbs10031