DEEP RESEARCH · KPF

KPF: From Fasteners to an Energy and Robotics Solutions Platform

A re-rating case built around TMC marine and power cables, SBB Tech precision reducers, and shareholder-return actions.

0. Bottom line first

My read is that KPF’s central change is whether the market can stop treating it as a bolt-and-nut manufacturer and start treating it as an operating holding company with fastener cash flow, TMC energy cables, and SBB Tech precision-control exposure. The source frames 2025 as the first year of valuation re-rating.

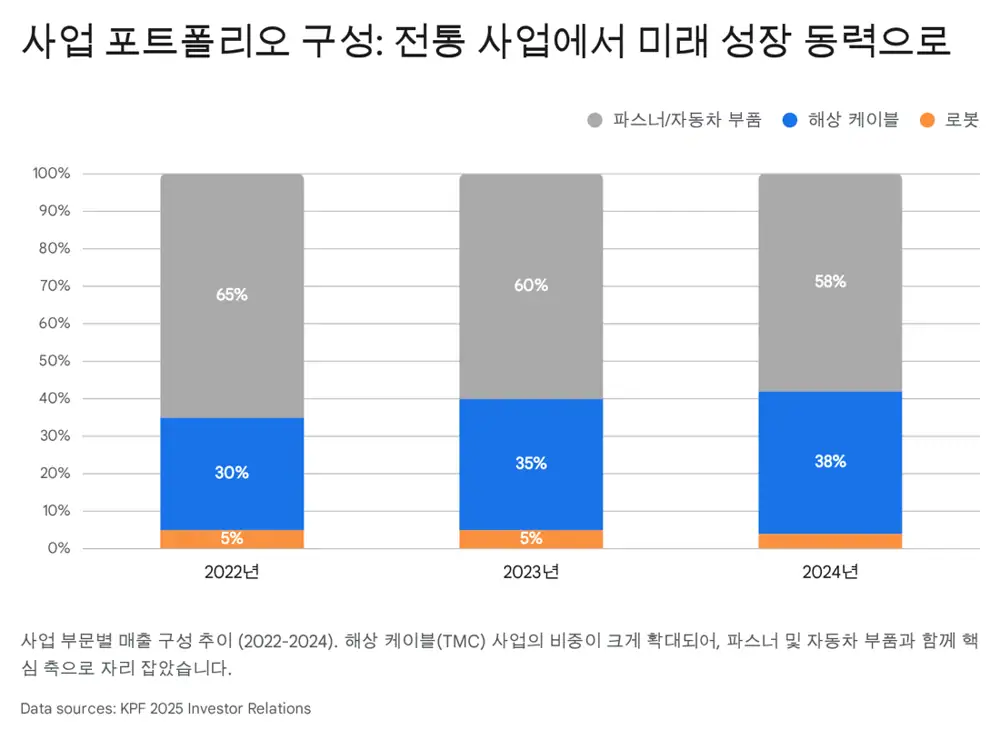

Official fact: The source defines KPF, now 62 years old, around three pillars: fasteners/auto parts as the cash cow, TMC as the growth engine, and SBB Tech as the future star. It reports 3Q25 consolidated revenue of KRW 174.1bn(-4.7% YoY), operating profit of KRW 8.6bn(+7.5% YoY), and net income of KRW 7.2bn(+727.7% YoY).

Interpretation: The more important point is that profit rose while sales declined. Low-margin fasteners were reduced, mix improved through special fasteners and high-value marine cable, and subsidiaries contributed to earnings. In-kind TMC dividends plus treasury-share and treasury-CB cancellation show a concrete attempt to narrow the holding-company discount.

1. Macro: shipbuilding, grids, and robotics are opening together

The post roots KPF’s re-rating stage in decarbonization, supply-chain reshoring, and smart manufacturing.

Shipbuilding supercycle

The source describes the longest boom since the 2008 financial crisis. Major Korean shipbuilders have more than 3.5 years of backlog, and marine cables account for about 3-5% of shipbuilding cost.

North American grid

IIJA, IRA, and AI data-center power demand are creating transmission and distribution investment needs. TMC Texas is the Buy America response.

Precision reducer localization

Precision reducers represent more than about 30% of robot cost, and the market has been dominated by Japanese HDS and a few others. SBB Tech is positioned for localization demand.

2. Core business: special fasteners and electrification parts

The fastener business centers on special industrial fasteners used in nuclear plants, wind towers, skyscrapers, and large bridges. The source cites the Çanakkale Bridge in Türkiye, Lotte World Tower, and the U.K.’s Hinkley Point C nuclear project as reference projects.

Official fact: The production structure is split between Chungju headquarters and Vietnam subsidiary KPF VINA. Chungju focuses on high-value special products and R&D, while Vietnam mass-produces standard products where cost competitiveness matters.

Interpretation: Fasteners may look generic, but high-tensile bolts require know-how in material mix, heat treatment, surface treatment, and forging. I view this core business as the cash generator that funds TMC and SBB exposure.

The automotive-parts business produces wheel bearings, cam lobes, gears, and other drivetrain parts. Despite internal-combustion concerns, the source says KPF is shifting toward EV and HEV parts, including higher exposure to third-generation wheel-bearing forged parts through long-term partnerships with SKF, Schaeffler, and other global bearing makers.

3. Growth engine 1: TMC and energy cables

TMC, acquired in 2021, is the most important growth engine in the source’s KPF valuation story. It is described as the global No. 1 in marine and offshore cables, with both the shipbuilding supercycle and energy-infrastructure investment as tailwinds.

- High-spec marine cables: LNG carriers and ammonia-fueled vessels require more power and communication cable because their gas-control and automation systems are complex. TMC is described as having high-entry-barrier products such as LNG-carrier cable tolerating -163°C and fire-resistant cable that maintains power for a period during fire.

- Certifications and customer lock-in: Marine cables require DNV, ABS, LR, and other class approvals. The source says TMC has major certifications and relationships of more than 20 years with HD Hyundai, Samsung Heavy Industries, and Hanwha Ocean.

- TMC Texas: The source lays out a December 2024 Texas entity, 1Q25 warehouse operation, core manufacturing setup in 1H25, and full operation target in 2H25.

- North American expansion: Target markets are aging-grid replacement, AI data-center power infrastructure, and optical communication. The source also mentions possible integrated solutions with Corning.

4. Growth engine 2: SBB Tech and precision control

SBB Tech is presented as the first Korean company to localize harmonic reducers, the “joint” of robots. KPF is the largest shareholder and therefore shares in robotics growth exposure.

Official fact: The post says Japan’s Harmonic Drive Systems controls more than 70% of the global harmonic-reducer market. SBB Tech is described as using proprietary tooth-profile design and heat-treatment know-how to achieve competitive performance and pricing, absorbing Korean robot makers’ de-Japanization demand.

| Expansion market | Source content | Watch point |

|---|---|---|

| Robotics | Small and light harmonic reducers for collaborative and humanoid robots | Mass-production customers after the robot-market chasm |

| Defense | K9 self-propelled howitzers, RCWS, and other precision weapons systems | K-defense exports and domestic component sourcing |

| Semiconductor | Roughly KRW 1.47bn contract for wafer-process equipment bearings to TSMC | Global reference for ultra-precision machining |

5. 3Q25: earnings quality matters more than sales

| Metric | 3Q25 consolidated | YoY |

|---|---|---|

| Revenue | KRW 174.1bn | -4.7% |

| Operating profit | KRW 8.6bn | +7.5% |

| Net income | KRW 7.2bn | +727.7% |

The source attributes the revenue decline to front-end inventory adjustments and reduced low-profit fastener products. Operating-profit growth is explained by mix improvement from high-value marine cables and special fasteners. The net-income surge is attributed to FX gains, lower finance costs, and equity-method gains from subsidiaries.

Financial health is described as stable at the end of 3Q25, with manageable debt and liquidity ratios. Debt from the TMC acquisition has been repaid with operating cash flow, and cancellation of KRW 4.5bn of treasury convertible bonds made the balance sheet leaner.

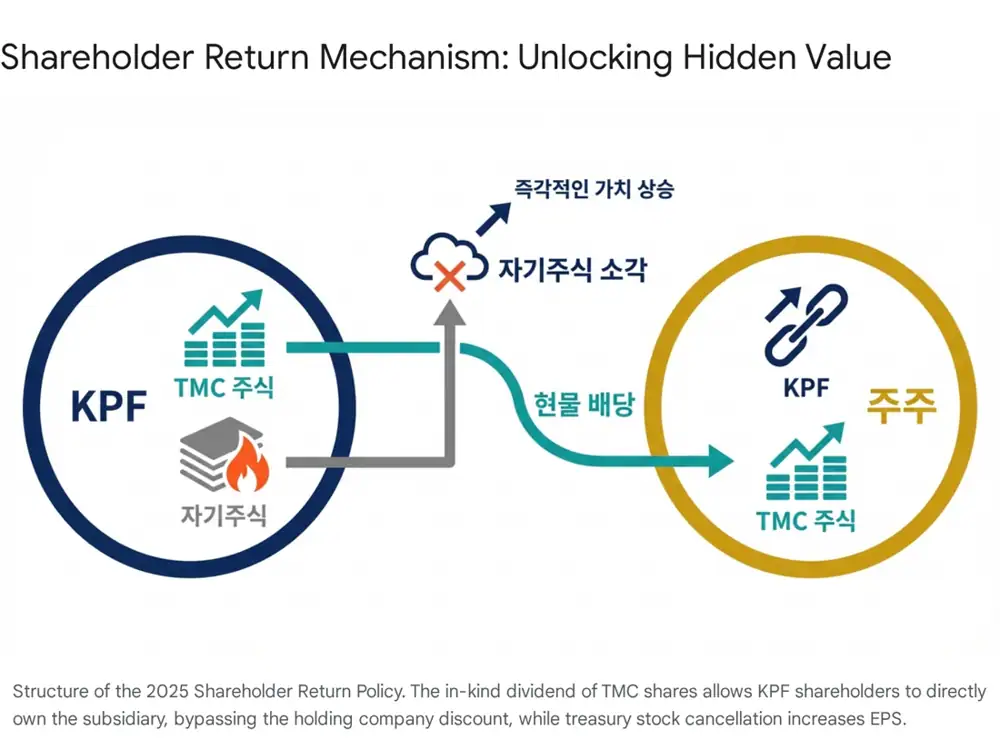

6. Shareholder return: TMC in-kind dividend and cancellation

The most important governance event in the source is an in-kind dividend of TMC shares. KPF is expected to distribute about 400,000 TMC shares to existing shareholders, with an estimated allocation ratio of roughly one TMC share per 31 KPF common shares.

- Strategic meaning: If TMC later pursues an IPO, this structure shares potential old-share sale gains directly with KPF shareholders instead of keeping them only at the company level. It is a tool to reduce the holding-company discount and double-counting issue.

- Tax structure: The source describes this as a capital-reduction-style dividend funded by transferring capital surplus to retained earnings, potentially improving after-tax proceeds under current Korean tax rules.

- Cancellation: On Dec. 1, 2025, KPF completed cancellation of 666,206 treasury shares, about 3.2% of shares outstanding, and KRW 4.5bn of treasury convertible bonds.

Interpretation: Treasury-share cancellation directly lifts EPS and BPS, while treasury-CB cancellation removes potential conversion overhang. Together, these actions support the source’s “sincerity of shareholder return” argument.

7. Outlook and valuation framework

| Year | Source forecast | Core assumption |

|---|---|---|

| 2024E | Revenue about KRW 782bn, OPM 5.0% | Early stage of shipbuilding upcycle entering earnings |

| 2025E | Revenue KRW 850bn, OPM 6.2% | Initial TMC Texas operation and higher high-value marine cable mix |

| 2026E | Revenue KRW 1.05tn, OPM 8.5% | TMC Texas full ramp-up and cable revenue from 2023-2024 high-price vessel orders |

| 2027E | Revenue KRW 1.2tn, OPM 9.5% | Higher profit contribution from SBB Tech robotics and defense |

The source argues that SOTP is the most reasonable method. It values the core fastener/auto-parts business at around KRW 200bn by applying an 8x traditional-manufacturing PER to KRW 20-30bn of annual operating profit. TMC, using a conservative 15x PER versus 20-30x 2026E PER for peers such as LS Marine Solution and Taihan Cable & Solution, is argued to be worth at least KRW 300bn in equity value. SBB Tech should be marked to listed-market value with a robotics control premium.

8. Checklist

- TMC Texas utilization and customer wins in North American grid and data centers

- Revenue recognition pace for high-value marine cables and shipyard backlog conversion

- SBB Tech volume expansion to TSMC and durability of defense revenue

- Actual schedule, tax effect, and IPO roadmap of the TMC in-kind dividend

- Additional shareholder-return policy after treasury-share and treasury-CB cancellation

I read KPF not as a plain cyclical manufacturer but as a deep-value/deep-tech intersection owning core infrastructure for the energy and robotics era. The test is whether TMC’s North American revenue and SBB Tech’s semiconductor and defense references turn into quarterly numbers.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224156141780