DEEP RESEARCH · HUMEDIX

Humedix: Aesthetic Consumables Economics and the Re-rating Path

A 2026-2028 view of fillers, toxin, skin boosters, and API expansion

0. Bottom Line First

My core read on Humedix is the consumables economics that follow the installed base of aesthetic devices. If the device is the printer, Humedix's fillers and skin boosters are closer to the ink.

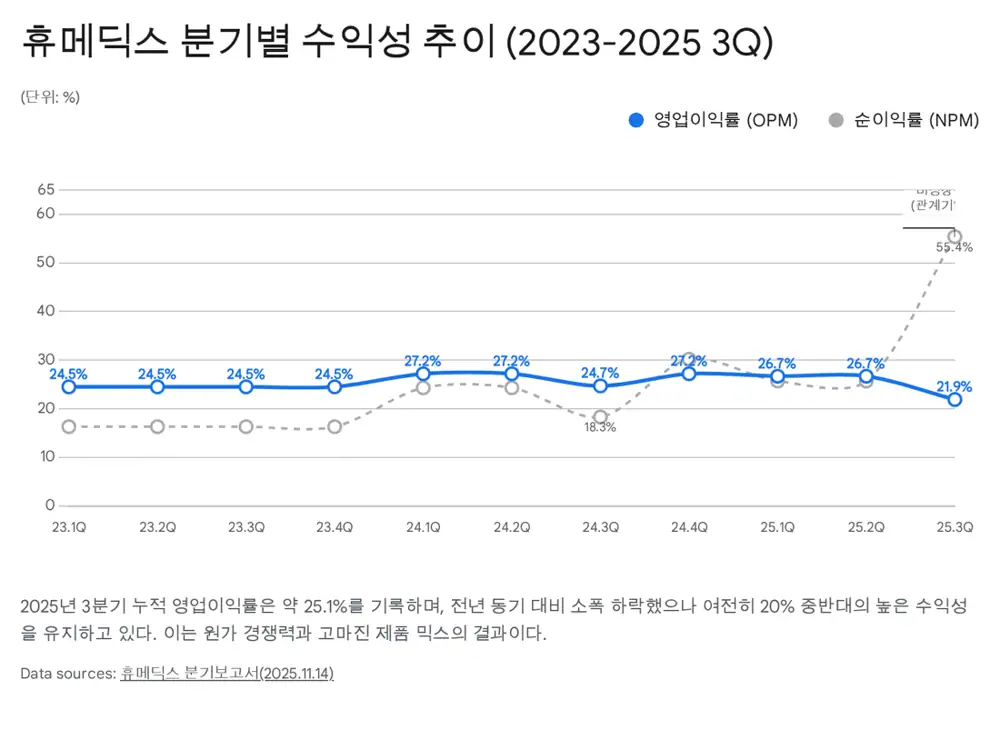

- For cumulative 3Q 2025, revenue was KRW 124.0bn and operating profit was KRW 31.2bn, implying an operating margin of about 25.1%.

- The core portfolio is HDRM cross-linking technology, Elravie/Revolline fillers, exclusive domestic sales of Liztox, PDRN/PN skin boosters, and localized heparin sodium API.

- Exports to Brazil grew 110% year on year in 2025, and the 2026 watchpoints are expansion from Brazil and Russia into the Middle East, Southeast Asia, and Latin America.

- The source argues that the stock trades at under 10x 2026E PER, versus a sector average of 15-20x, with a consensus-like target around KRW 73,000 and more than 50% upside from the then-current price.

1. Business Model and Technical Moat

Official fact: The source frames Humedix as more than a hyaluronic-acid filler maker: it is a total aesthetic solution company spanning toxin, PDRN/PN skin boosters, and heparin sodium.

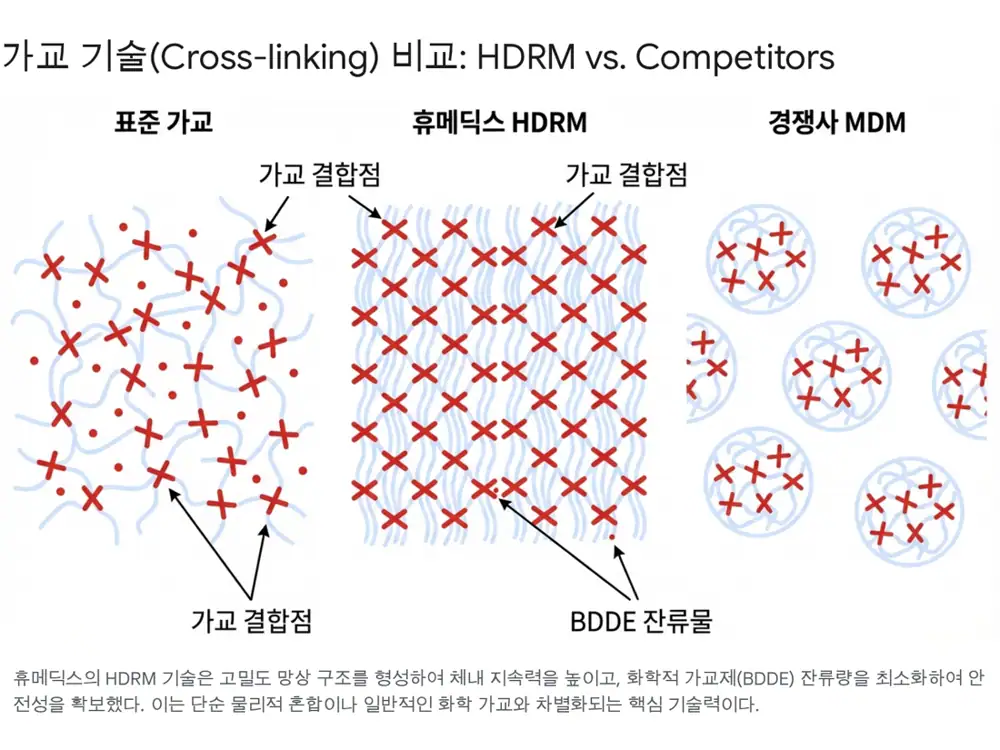

In fillers, product quality is driven less by marketing than by cross-linking quality. The source says Humedix's HDRM process links HA molecules into a dense, evenly spaced network, blocking hyaluronidase penetration and extending post-procedure volume duration by more than 20-30% versus simpler mixed structures.

Longer Lasting

The network structure is presented as making enzymatic degradation physically harder.

BDDE Control

Multi-stage washing and cross-linking control are cited as lowering free BDDE to non-detectable levels.

Customized Properties

High elasticity for nose/chin and softer viscosity/cohesivity for lips or under-eyes can be produced from one platform.

Interpretation: The moat is not only a filler SKU. It is the ability to offer body-area-specific products and bundle fillers, toxin, and skin boosters through one hospital channel.

2. Portfolio: Triangle plus API

The largest strength is cross-selling rather than dependence on one filler. Humedix has exclusive domestic sales rights for Liztox, a botulinum toxin produced by Huons BioPharma, a subsidiary of parent Huons Global, making procurement easier for clinics that use fillers and toxin together.

For skin boosters, Humedix has built Revitalex and Elravie Re2O from in-house PDRN extraction technology. Its PN+HA composite filler Valpien completed a clinical confirmation study in December 2025, targets a product-approval filing in 1H 2026, and is expected in the source to contribute meaningfully from 2027.

Official fact: The source also highlights Korea's first localization and MFDS approval of heparin sodium, previously fully dependent on Chinese imports.

3. Financial Quality and Export Momentum

| Item | Source figure | Meaning |

|---|---|---|

| 3Q 2025 cumulative revenue | KRW 124.0bn | Revenue held up despite domestic softness and competition |

| 3Q 2025 cumulative operating profit | KRW 31.2bn | About 25% OPM for a manufacturing biotech company |

| Operating cash flow | KRW 29.6bn | Adjusted operating cash generation of KRW 34.0bn exceeded operating profit |

| Trade receivables | KRW 28.4bn | Up from KRW 20.4bn at end-2024, interpreted as export growth |

| Exports to Brazil | +110% YoY | Evidence for the OBM direct-export strategy |

Operating margin moved from the low 20% range in 2023 to the 26% range in 2024. Although domestic filler and toxin softness caused a temporary margin drop in 2Q 2025, cumulative 3Q 2025 margin recovered to the 25% range. The source attributes this to higher utilization at the second Jecheon plant and a larger OBM export mix.

4. Risks and Governance

Official fact: The source identifies indirect exports through wholesalers as a major regulatory risk in Korean aesthetics, because MFDS has previously treated overseas shipments through domestic traders as domestic sales for national lot-release purposes.

Interpretation: Humedix is described as having shifted quickly toward approved direct exports, including NMPA-approved Elravie Deep Line in China, while Brazil and Russia are handled through formal local partners. That makes the source's regulatory-risk discount look lower than for some peers.

- China: approval for lidocaine-included filler and local partner strategy are cited.

- Brazil: ANVISA approval and local partner marketing support the 110% 2025 export growth claim.

- Russia/CIS and Middle East: Russian approvals and 2026 new Middle East permits, including Syria, are expected to diversify exports.

- Governance: the largest shareholder is Huons Global with a 36.08% stake. As of 3Q 2025, related-party sales were about KRW 36.2bn and purchases about KRW 12.1bn.

- Overhang: the source says outstanding CBs are absent or immaterial, and stock-option balances are not large enough to be a major supply burden.

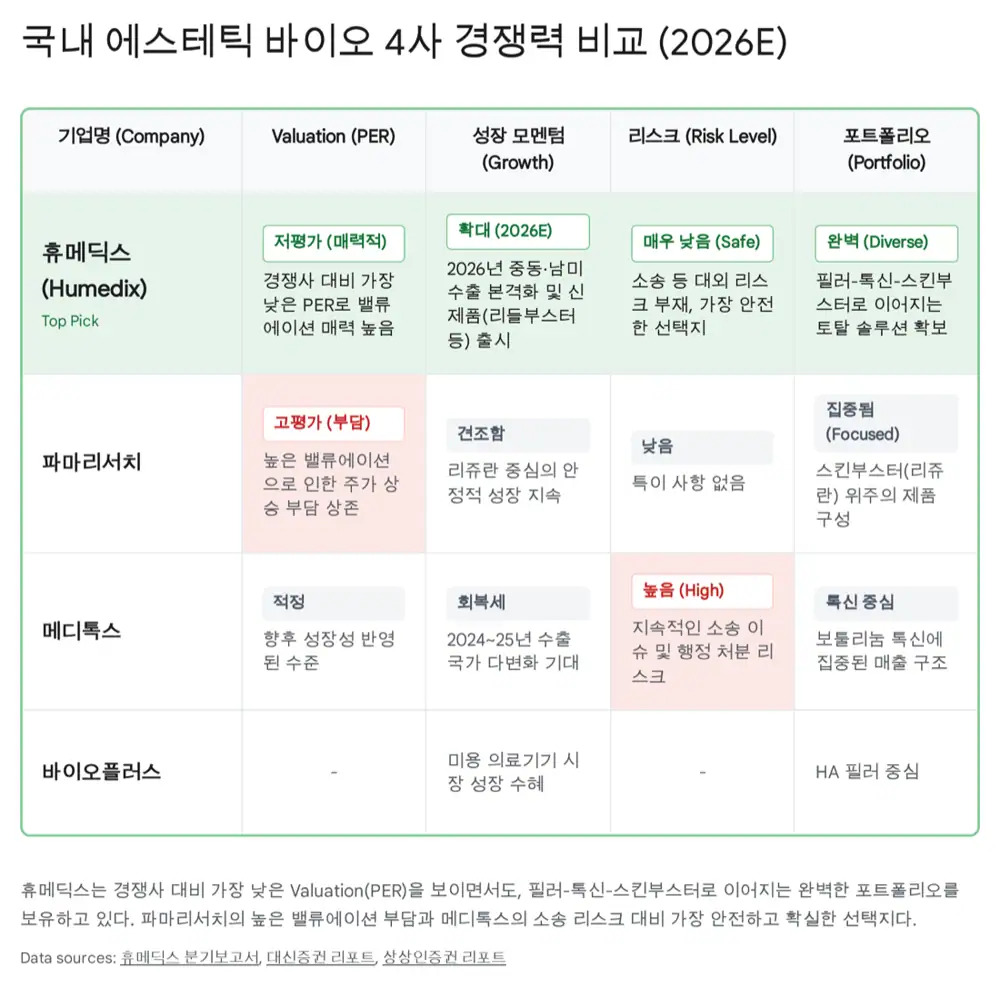

5. Peer View and Tracking Checklist

| Company | Source rank | Core view |

|---|---|---|

| Humedix | 1st | Under 10x 2026E PER, 25% OPM, broad filler/toxin/skin-booster/device/API mix |

| PharmaResearch | 2nd | Rejuran brand power is strong, but above-20x PER and single-product reliance limit upside |

| Medytox | 3rd | U.S. expansion optionality exists, but litigation and earnings volatility weigh on the case |

| BioPlus | 4th | High OPM is attractive, but Hainan project execution and filler concentration need proof |

The suggested tracking method is to combine Jecheon-si export data for HS Code 3304.99 and 3004.90, because the source says the Jecheon factory location gives this data more than 90% correlation with Humedix exports. ASP should be tracked by dividing Jecheon export value by export weight, and Huons BioPharma toxin export data can be used as a bundled-sales signal.

In the source's words, this is the moment when the ink looks more attractive than the printer. The thesis still needs quarterly proof through Valpien approval progress, Brazil/Russia/Middle East exports, ASP defense, and OCF recovery.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224156140216

- 상상인증권 휴메딕스 리포트: https://humedix.com/m/home.php?go=Emenu_04&go_pds=pds_text_list&pds_num=81&start=0&num=2789&mode=&field=&s_que=

- 메디코파마, 휴메딕스 브라질 수출 110% 성장: https://www.medicopharma.co.kr/news/articleView.html?idxno=65233

- 인더뉴스, 휴온스글로벌 2025년 2분기 실적: https://www.inthenews.co.kr/news/article.html?no=75749

- 메디톡스 관련 리포트: https://ssl.pstatic.net/imgstock/upload/research/company/1697070644086.pdf