DEEP RESEARCH · BIOPLUS

BioPlus: From DVS Fillers to a Global Bio-Beauty Platform

A read-through on MDM technology, distribution reset, Hainan and U.S. expansion, GLP-1, and toxin pipelines.

0. Bottom line first

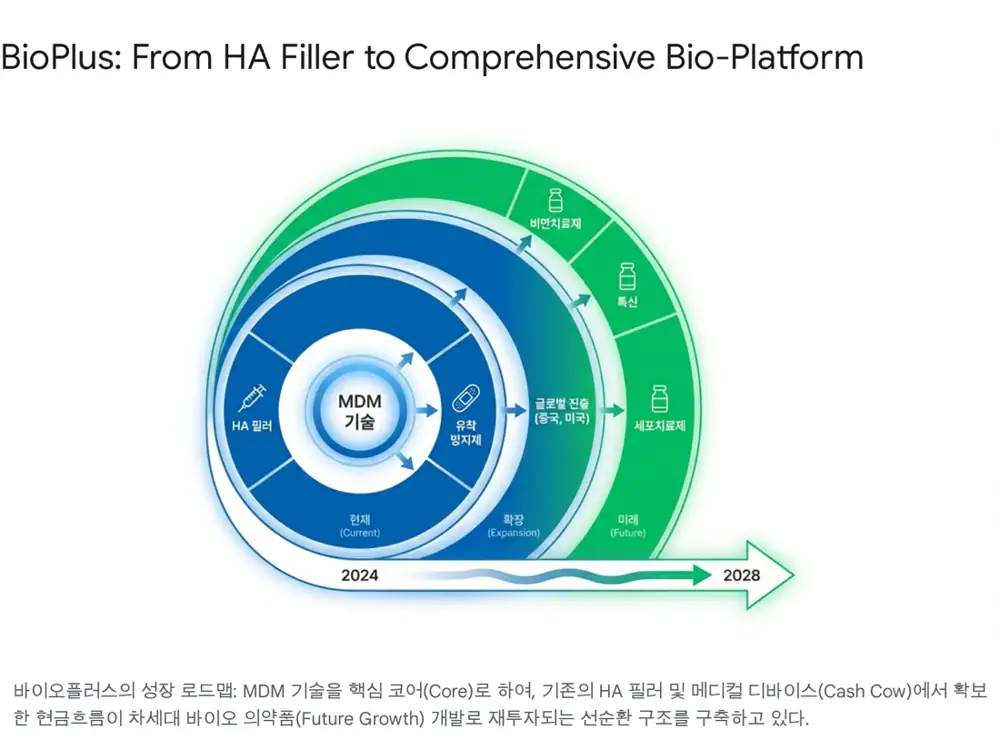

My core read is that BioPlus should not be viewed only as a small/mid-cap HA filler maker. The original post frames it as a bio-beauty platform built on DVS crosslinking and MDM® technology, extending into fillers, adhesion barriers, joint and bladder repair products, GLP-1, toxins, and cosmetics.

Official fact: The source highlights 2025 nine-month sales of KRW 67.7bn, 3Q operating profit of KRW 14.0bn, roughly 81% YoY sales growth, exports above about 72% of revenue, around KRW 160bn invested in the Eumseong Bio-Complex, Hainan class-II medical-device GMP approval, and establishment of BioPlus USA Inc.

Interpretation: Near-term results were pressured by distribution clean-up and new-factory fixed costs, but the quality of earnings should improve if the company is really moving from low-margin distributors and ODM volumes toward own-brand exports, direct sales, and larger partners. The key is whether Hainan sales, FDA clinical milestones, and lower indirect-export risk show up in 2026 numbers.

DVS and MDAP™

In a BDDE-standard filler market, the source argues that DVS crosslinking plus purification supports premium physical properties.

Distribution reset

Since 2024, BioPlus has reduced small-distributor exposure and moved toward direct sales and larger global partners.

Eumseong and Hainan

The Eumseong Bio-Complex and Hainan plant are the physical base for moving from boutique production to global scale.

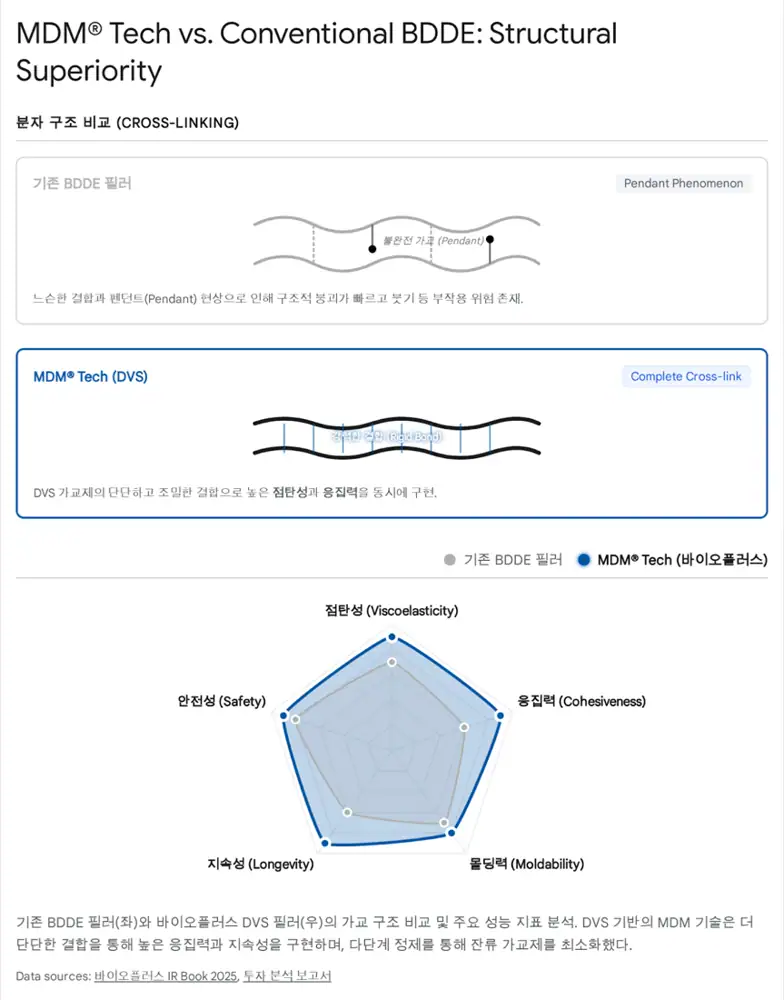

1. Technology moat: DVS versus BDDE

More than 90% of the global HA filler market uses BDDE(1,4-Butanediol diglycidyl ether) as the crosslinker. The source presents BioPlus as challenging that standard with DVS(Divinyl Sulfone) crosslinking.

Official fact: The post describes BDDE as difficult to remove completely after reaction and notes that higher input can create a pendant phenomenon, where only one side of the crosslinker binds. DVS is described as forming a shorter and stronger bond, but with much higher purification difficulty because of its strong reactivity.

Interpretation: The important point is not just DVS itself. It is the purification capability that lets DVS become commercial product. The post says BioPlus solved residual toxicity and impurity issues with MDAP™(Multiple Degree Amphiphilic Purification), making that combination the basis for premium pricing and high OPM defense.

2. Portfolio: expansion beyond fillers

The source argues that MDM is not limited to filler manufacturing and is being extended into medical devices and drug candidates.

| Product or pipeline | Role in the source | Investment watch point |

|---|---|---|

| InterBlock | Gel-type adhesion barrier for spine and abdominal surgery | Syringe convenience versus film products and optimized residence time |

| HyalSyno | Joint repair product replacing reduced synovial fluid | Aging-demand exposure and high-viscoelastic HA application |

| Blad-Care | Temporary GAG-layer supplement for chronic cystitis patients | Non-covered treatment market for pain and symptom relief |

| GLP-1 | Obesity and diabetes therapy in development with Ubiprotein | Bio-better and microneedle patch formulation, possible licensing option |

| Next-generation toxins | Pure and recombinant toxins designed to reduce resistance | Bundling with filler sales |

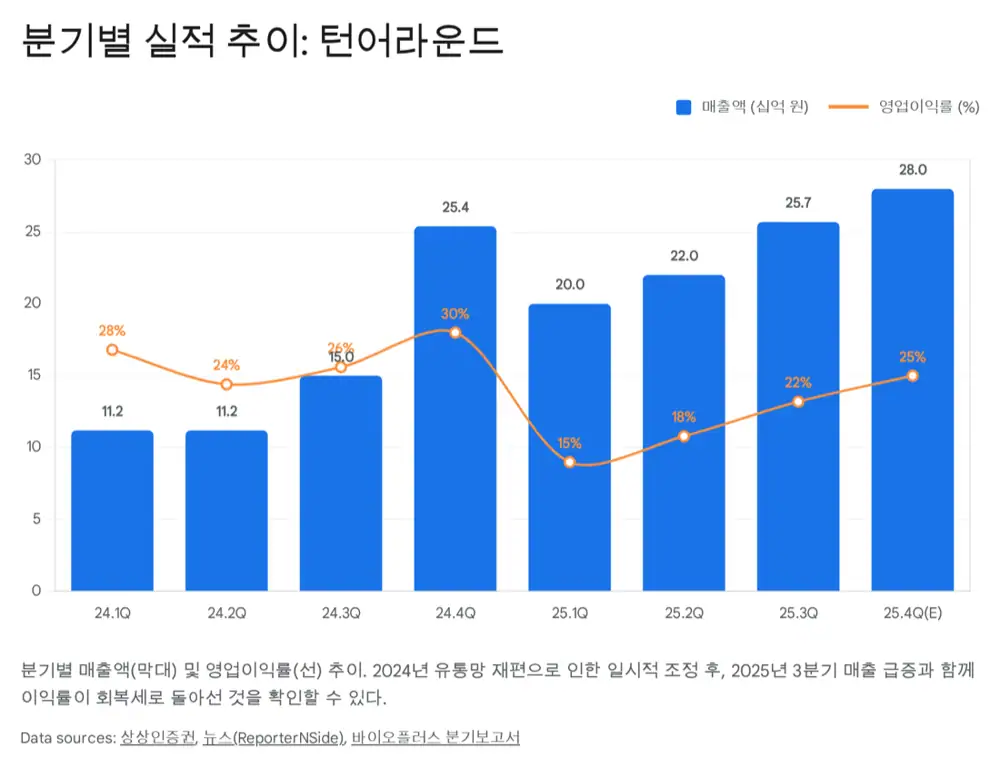

3. 2025 results: transition into recovery

2025 nine-month consolidated sales were KRW 67.7bn. The source says the company suffered temporary sales volatility after restructuring its small-distributor network in 2024, but the benefits of the new large-partner/direct-sales structure began to appear in 2025.

Official fact: The post gives 3Q sales growth of roughly 81% YoY and 3Q operating profit of KRW 14.0bn, up 43% YoY. BioPlus historically generated 40-50% OPM, but depreciation from new-factory preparation and higher global marketing SG&A brought recent margin down to the low-20% range.

Interpretation: Revenue quality matters more than revenue alone. If low-margin ODM declines while own-brand sales, overseas direct exports, and large-partner receivable stability improve, the business becomes less volatile.

| Item | Source figure/content | Meaning |

|---|---|---|

| 2025 nine-month sales | KRW 67.7bn | Recovery after distribution reset |

| 3Q sales growth | About +81% YoY | Turnaround signal even after base effect |

| 3Q operating profit | KRW 14.0bn, +43% YoY | Profit defense despite fixed-cost pressure |

| Export mix | About 72%+ of sales | Directionally lowers indirect-export exposure |

| Eumseong Bio-Complex CAPEX | About KRW 160bn | Major investment cycle ending, possible FCF improvement |

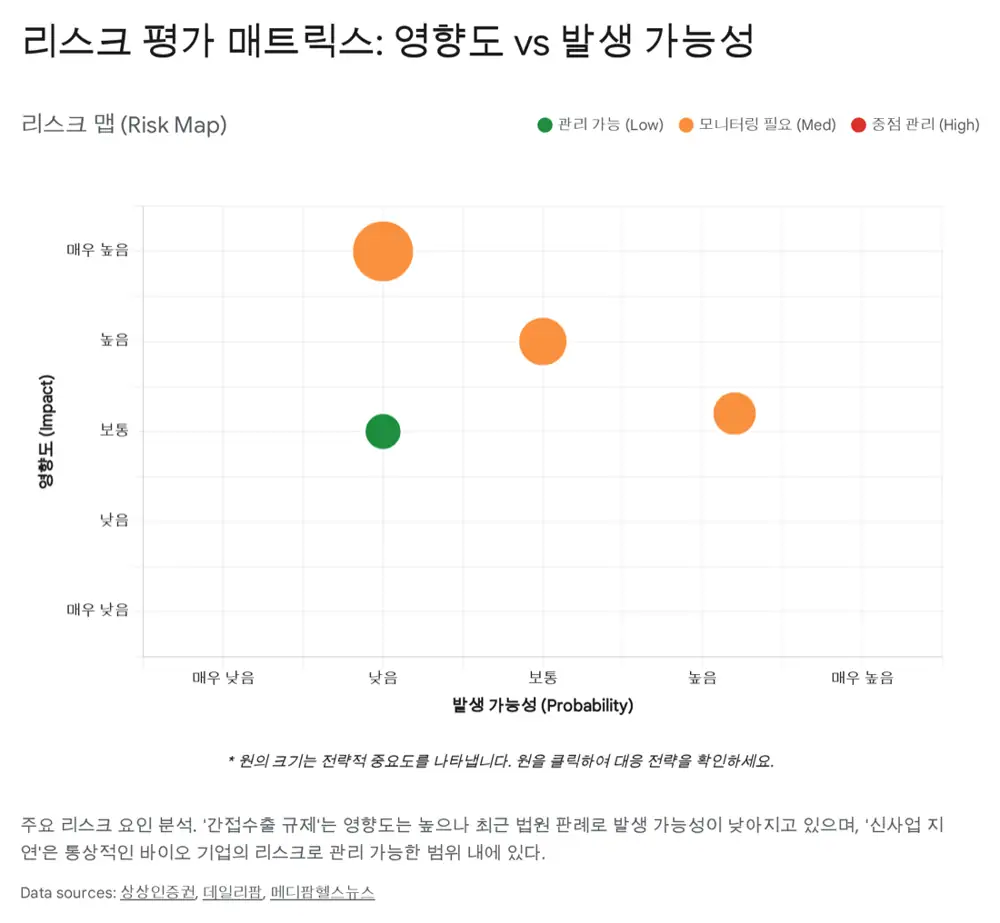

4. Risks: regulation, approvals, and competition

The most direct risk is the indirect-export issue that affected Korean botulinum toxin and filler companies. The post explains that the MFDS interpreted exports through domestic trading companies as domestic sales, creating administrative-sanction risk around national lot release.

- Indirect exports: Related companies, including BioPlus, are in administrative litigation, and courts have granted stays in many cases. Legal uncertainty remains until final rulings.

- Response: The post says a key aim of the 2024 distribution reset was lowering dependence on indirect exports. More direct exports through overseas entities and partners should dilute the risk.

- Approvals: U.S. FDA and China NMPA timelines can slip. The source says U.S. entry is targeted for 2026 but a one- to two-year delay should be conservatively considered.

- Competition: BioPlus must gain share between low-cost Chinese players and global majors. Its chosen strategy is a DVS-based premium niche rather than a low-price market.

5. 2026-2028 roadmap: Hainan, the U.S., and new businesses

Hainan

Class-II medical-device GMP approval is complete, while class-III and cosmetics production approvals are in progress. Local production may help tariffs and cost competitiveness.

BioPlus USA

BioPlus established wholly owned BioPlus USA Inc. in 3Q25. FDA approval targeted in 2026 is a key re-rating variable.

GLP-1 and toxins

Microneedle GLP-1 and resistance-reducing toxins are long-term growth options beyond fillers.

Official fact: The source expects Hainan filler and skinbooster sales, including the Bonics brand, to begin meaningfully from late 2025 and says FDA approval would serve as a global quality signal, not just U.S. market access.

Interpretation: Re-rating after 2026 should be stronger when approval milestones are accompanied by Hainan utilization, U.S. clinical progress, and direct-export data.

6. Governance and capital policy

CEO Hyun-Kyu Jung is described as an environmental-engineering PhD with a technology-centered management philosophy. The post interprets this as a preference for expansion connected to the company’s biomaterials core rather than unrelated diversification. Major shareholder and related-party ownership is described as stable, with limited owner risk.

At the same time, convertible bonds and employee stock options remain potential dilution factors as of 3Q25. The post says these can create overhang when the share price rises, but potential share buybacks and shareholder-value actions may limit the market impact. My checklist is to keep watching CB refixing terms, maturities, and option exercise risk.

7. Monitoring checklist

- Quarterly export data from Korea Customs TRASS, especially direct-export mix to the U.S. and Europe

- China Hainan plant utilization and actual sales contribution

- FDA clinical progress and concrete milestones

- Final direction of indirect-export litigation and direct-export mix

- CB refixing, maturities, stock-option exercise, and other overhang items

Overall, BioPlus can be read as a structurally growing company with technology completeness and a high-margin history. My condition is simple: after 2026, overseas approvals and production capacity must convert into revenue and cash flow.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224156138986

- Dec. 18, 2024 securities report: BioPlus 4Q recovery and 2025 growth outlook: https://contents.premium.naver.com/nomadand/nomad/contents/241218054106730et

- MediPharm Health News: BioPlus completes GMP approval for Hainan medical-tourism-zone plant: https://www.medipharmhealth.co.kr/news/article.html?no=106446

- DailyPharm news search: https://m.dailypharm.com/user/news/search?dropBarMode=search&searchOption=any&searchKeyword=%23%EC%9D%B4%EA%B4%80&view_mode=pc&page=3

- ReporterNside release: BioPlus 3Q cumulative sales of KRW 67.7bn, up 81% YoY: https://press.reporternside.com/newsRead.php?no=1023035

- Asia Economy CORE: BioPlus 4Q recovery and 2025 high-growth expectation: https://core.asiae.co.kr/article/2024121607520586161

- Newsis: BioPlus completes GMP approval for Hainan plant in China: https://mobile.newsis.com/view/NISX20250411_0003135418