DEEP RESEARCH · Asterasys

Asterasys: Aesthetic-Device Growth After FDA Clearance

A review of HIFU, RF, recurring consumables, and the U.S. expansion scenario.

0. Bottom line first

Asterasys combines technology differentiation, recurring consumables revenue, and FDA momentum. FDA clearance is permission to sell, not proof of U.S. success, so 2026 distribution traction matters.

1. Company and governance

Official fact: It was founded in July 2015 as Daehan Biomedical, originating from Daehan Scientific’s healthcare business. As of September 30, 2025, CEO Seo Eun-taek held 34.53%, CTO Kim Jong-seok 6.40%, and CFO Lee In-ho 3.88%.

Technology build

HIFU localization and pen-type Liftera launch.

Global expansion

CE, ANVISA, MOH, and the 2022 USD 7mn export award.

Takeoff

KOSDAQ listing, Coolfase FDA clearance, and CoolSoniq launch.

2. Product portfolio

Official fact: Liftera TDT forms thermal coagulation points at 10Hz while reducing pain. Coolfase, launched in 2024, is a monopolar RF device using DCC direct cooling to reduce cryogen gas cost and pain. The source also includes an assisted content link.

3. Numbers and outlook

| Item | Source figure | Meaning |

|---|---|---|

| Consumables mix | 62.0% | Recurring revenue |

| Overseas revenue | 66.1% | Global expansion |

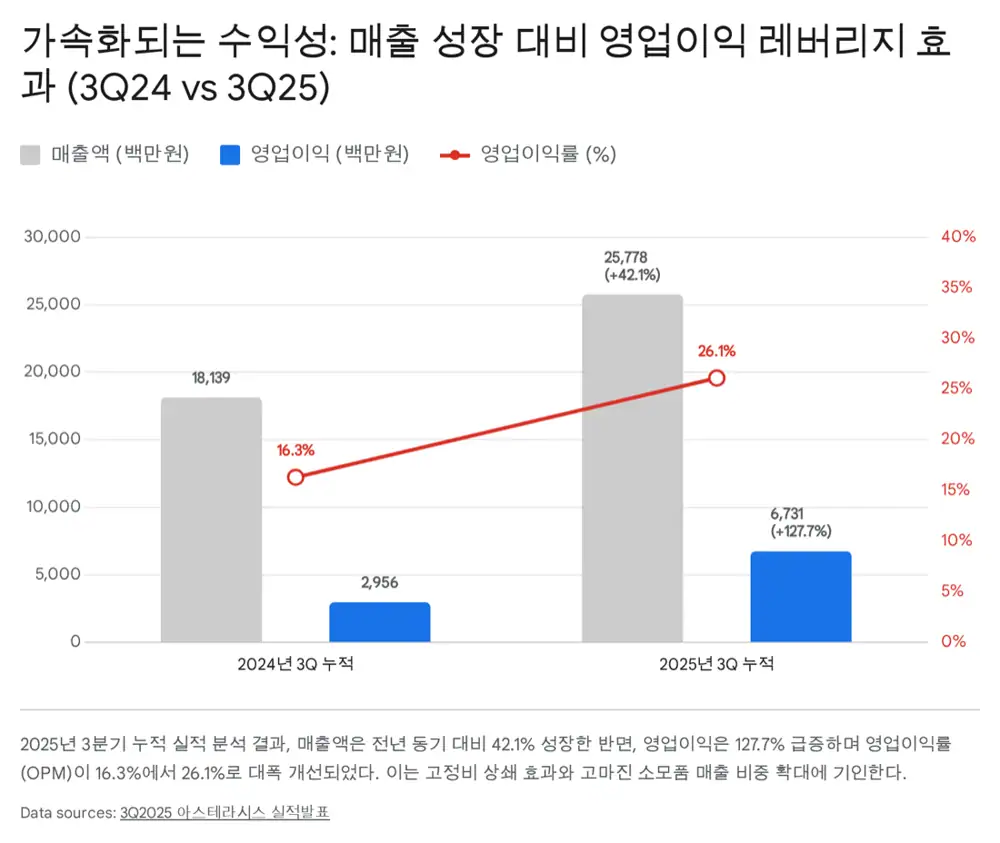

| Q3 2025 revenue | KRW 8.75bn, YoY +29.2% | Continued growth |

| Q3 2025 cumulative | KRW 25.78bn, YoY +42.1% | New products and overseas |

| Q3 2025 OPM | 26.3% | Improved from 16.3% in 2024 |

| Debt ratio | 7.27% | Financial stability |

4. Valuation and risks

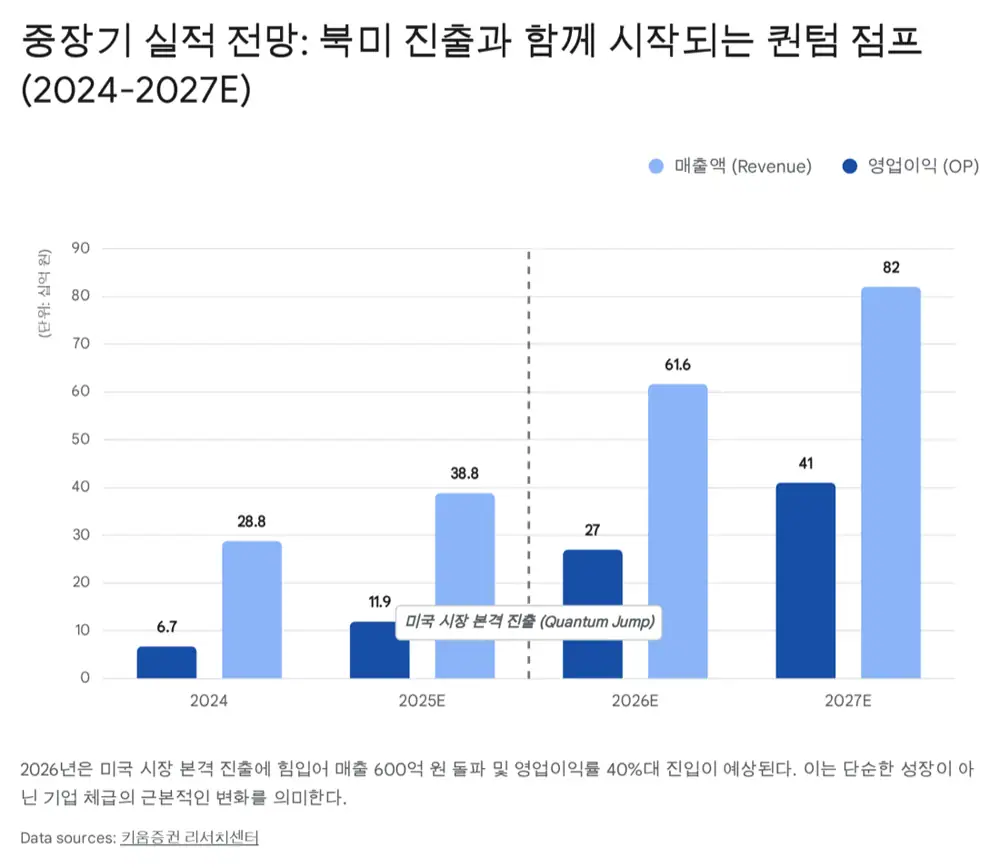

- 2025E revenue KRW 38.8bn, operating profit KRW 11.9bn, OPM 30.7%.

- 2026E revenue KRW 61.6bn, operating profit KRW 27.0bn, OPM 43.8%.

- 2027E revenue KRW 82.0bn, operating profit KRW 41.0bn.

- Forward PER is presented at about 14-20x using 2026E net income of KRW 24.1bn.

- Risks are U.S. distribution, key-doctor marketing, lock-up and stock-option overhang, FX, and emerging-market volatility.

5. My conclusion

Asterasys rests on 62.0% consumables mix, 66.1% overseas revenue, and FDA-cleared products. The key is whether U.S. revenue reaches 10-15% in 2026.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224155107138

- Source 2: http://googleusercontent.com/assisted_ui_content/2

- Source 3: https://asterasys.com/products/coolfase/

- Source 4: https://v.daum.net/v/3mjPzWNdNo

- Source 5: https://www.accessdata.fda.gov/cdrh_docs/pdf25/K250852.pdf

- Source 6: https://asterasys.com/

- Source 7: https://asterasys.com/about-us/history/

- Source 8: https://luxaestheticclinic.com/treatment/hifu/liftera/

- Source 9: https://www.sycamoremedispa.com.au/post/liftera-cool-painless-face-lift

- Source 10: https://coolfase.com/

- Source 11: https://asterasys.com/blog/imcas-asia-2025/

- Source 12: https://biz.chosun.com/stock/market_trend/2025/10/20/BUPQCSXV6VEIBFIFTSLFQNKEDU/

- Source 13: https://oec.world/en/profile/bilateral-country/tha/partner/bra

- Source 14: https://biz.chosun.com/en/en-finance/2025/01/03/NIVX7XB6ARFN7GURG5VVCGVWRE/

- Source 15: https://pharm.edaily.co.kr/News/Read?newsId=01164406642334560

- Source 16: https://www.globalnewstop.com/news/articleView.html?idxno=1744

- Source 17: https://simplywall.st/stocks/kr/healthcare/kosdaq-a214150/classys-shares/future

- Source 18: https://www.gangnamskincenter.com/blog/shurink-vs-liftera-korea

- Source 19: https://enprimiclinic.com/column/6819

- Source 20: https://www.gangnamdermatologyclinic.com/blog/oligio-vs-thermage-koreas-most-popular-rf-treatments-compared

- Source 21: https://enyaanclinic.com/trend/oligio-lifting-vs-thermage-flx-in-korea/