DEEP RESEARCH · NAMUGA

Namuga: Vision Sensing for Physical AI

A structural transition from smartphone camera-module cash cow to robotics, XR, and automotive 3D sensing solutions

0. Bottom line first

My read is that Namuga is moving beyond its old identity as a smartphone camera-module vendor and being redefined as a 3D sensing solutions company that helps robots, XR devices, and vehicles perceive the physical world. Mobile still dominates revenue, but Active Align and Calibration capabilities built there are the common base for the new businesses.

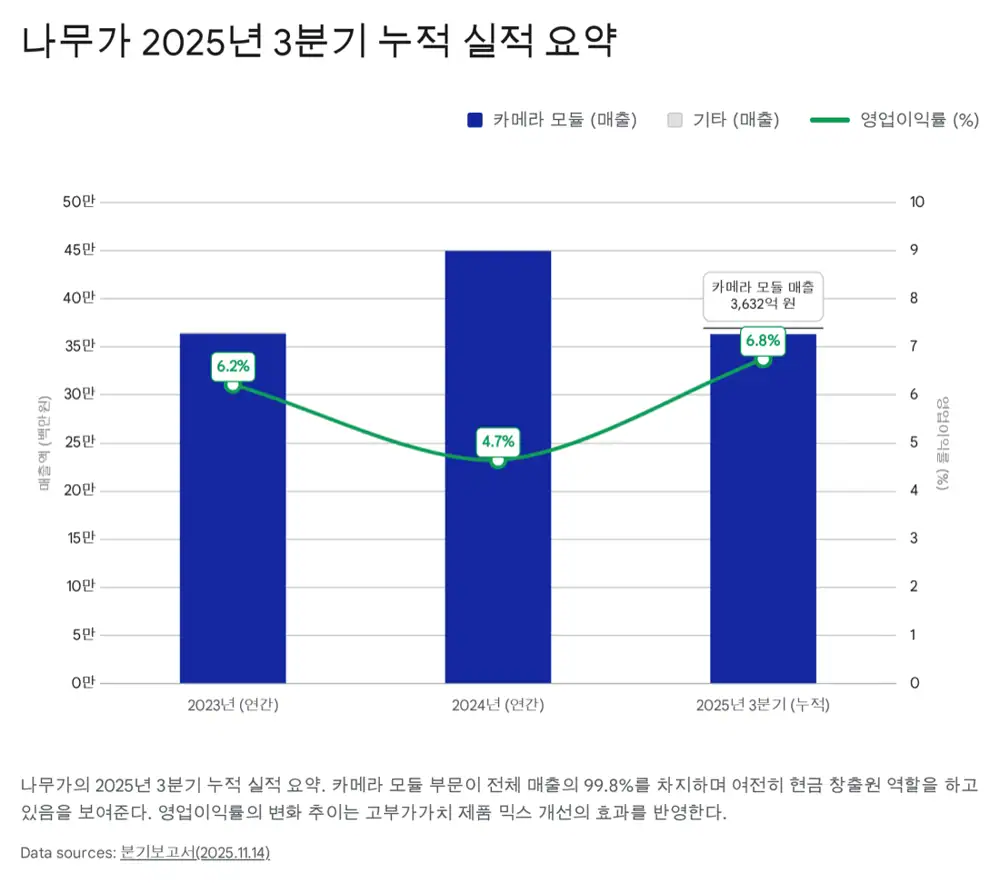

Official fact: Cumulative Q3 2025 revenue was KRW 363.8 billion and operating profit was KRW 24.6 billion. Compared with cumulative Q3 2024 revenue of KRW 346.1 billion and operating profit of KRW 16.7 billion, revenue rose about 5.1% and operating profit rose about 47.3%.

Interpretation: Despite smartphone-market stagnation, operating margin improved from the 4% range in 2024 to about 6.7% as of Q3 2025. That points to manufacturing yield, mix improvement, and higher OIS model exposure. This cash flow funds robotics and lidar investment.

1. Company profile and a new read on the legacy business

Namuga was established on October 14, 2004, started with audio modules and lens development, and listed on KOSDAQ in 2015. Its headquarters are in Pangyo, Seongnam, and it operates a large manufacturing base in Phu Tho, Vietnam. As of year-end 2024, consolidated revenue was KRW 450.4 billion, total assets were KRW 264.4 billion, and employees numbered about 1,055.

The company's technical DNA is not simple assembly; it is system engineering across optics, mechanics, electronics, and calibration software. Active Align, which aligns the optical axes of image sensors and lenses at the micrometer level, is a key process for high-pixel camera-module yield and becomes an entry barrier in more precise 3D sensing modules.

Official fact: Smartphone camera modules represented about 99.8% of Namuga's 2024 revenue. The source argues that despite market concern, a higher mix of flagship high-pixel and OIS modules and Samsung first-tier vendor status support profitability.

Smartphone CCM

Higher exposure to flagship high-pixel and OIS modules, including Galaxy S series, supports ASP and profitability.

Active Align

Micrometer-level lens and sensor alignment in manufacturing extends naturally into 3D sensing.

Calibration S/W

Algorithms and automation equipment correct lens distortion, thermal noise, and assembly tolerance to create accurate depth maps.

2. 3D sensing technology stack

2D imaging captures color and brightness; 3D sensing captures distance and shape in real time. That is foundational for robot navigation, grasping, XR gesture recognition, and automotive safety systems. Namuga is building a solution stack across ToF, stereo vision, structured light, and calibration. Links include The Elec emitter-design article and Namuga Vision Solution partnership release.

| Technology | Principle | Main use | Namuga point |

|---|---|---|---|

| iToF | Measures distance using phase shift of modulated light | Robot-vacuum obstacle avoidance, smartphone bokeh | Validated through mass production of Samsung robot-vacuum iToF modules |

| dToF | Directly measures round-trip light-pulse time | LiDAR and AR-glasses environment mapping | The source says Namuga is developing next-generation AR dToF modules with a global Big Tech company |

| Stereo vision | Triangulates distance with two cameras | Robot navigation cameras | Targets the market through Intel RealSense-compatible models |

| Structured light | Analyzes distortion in projected IR patterns | Face recognition and precision inspection | Useful where near-field precision is required |

| Calibration | Corrects lens distortion and assembly error | All 3D depth-map generation | Basis for viewing Namuga as a vision-solutions company, not just a hardware assembler |

Interpretation: As hardware specifications converge, depth-data accuracy depends increasingly on calibration. That is the technical basis for re-rating Namuga from a mobile component supplier to a sensing-solutions company.

3. Growth axis I: robotics

As robotics shifts from AGVs to AMRs and humanoids, 3D sensors become the robot's eyes. Namuga is entering this market through Samsung robot appliances and a global automaker robot platform.

Official fact: The source states that Namuga's 3D sensing module is installed in Samsung's Bespoke AI Steam robot vacuum launched in 2024. Related links: Aju Business article, Asia Economy article, and Dong-A robot vacuum market article.

Robot vacuums need to identify and avoid small obstacles such as cables, socks, and pet waste at the 1cm level. LDS alone is not enough; a vision system combining RGB camera and 3D ToF sensor is needed. If Samsung expands its robot-vacuum lineup and 3D sensors move into lower-priced models, Namuga's module shipment volume can structurally increase.

Official fact: Namuga was selected as a 3D sensor supplier for a global automaker group's robot platform, and the source says it is scheduled to supply 3D sensing camera modules for that robot product line from 2026. Links: Namuga notice and Asia Economy English article.

The source infers that this automaker group may be Hyundai Motor Group and mentions potential synergy with Boston Dynamics robots such as Atlas and Spot. Humanoid robots may need dozens of cameras and sensors per unit, creating a large quantity opportunity for sensor suppliers if the market opens.

4. Growth axis II: XR

After Apple Vision Pro, the XR market is regaining attention with the Samsung, Google, and Qualcomm alliance. The source states that Samsung plans an XR headset code-named Project Moohan using Google's Android XR OS and Qualcomm's latest chipset. Related links: Project Moohan article, Namuga AR/VR business page, and Namuga AR/VR camera article.

XR devices need to recognize the user's gaze, facial expression, hand gestures, and surrounding space in real time. Namuga is focused on ultra-small, low-power camera modules for eye tracking and face tracking. The source treats the VR9700 project name in Namuga's IR materials as a sign that XR hardware development is already well advanced.

The source also mentions an exclusive partnership with Belgium's VoxelSensors. VoxelSensors' SPAD-based sensing technology has very low power consumption and fast response, making it suitable for battery-sensitive XR devices. This partnership is read as a signal that Namuga is moving beyond hardware manufacturing toward a sensing technology platform.

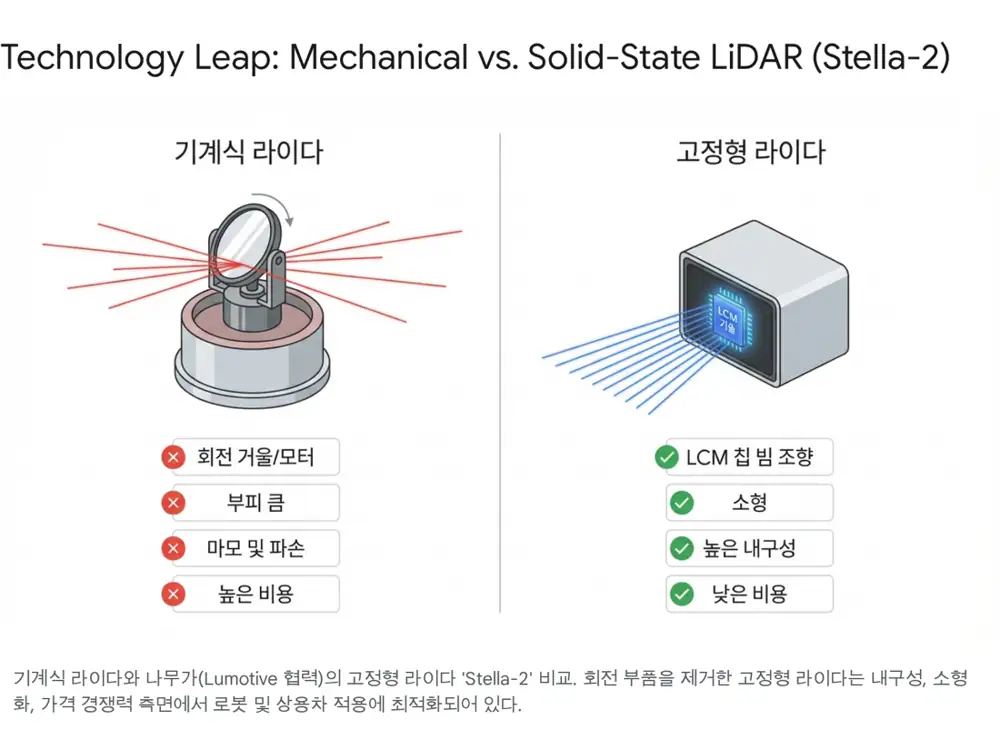

5. Growth axis III: automotive and Stella-2 LiDAR

As autonomous driving advances, cars are becoming moving sensor platforms. Namuga is targeting automotive markets with in-cabin monitoring, IR cameras, and solid-state lidar.

As safety rules such as Euro NCAP become stricter, driver monitoring systems and occupant monitoring systems are becoming important. The source says Namuga has developed an IR camera-based in-cabin solution and has supply references with Google's autonomous-driving subsidiary Waymo. IR camera modules that can recognize accurately in dark cabins may become essential safety devices for Level 3 and above autonomy.

Official fact: Namuga developed the solid-state lidar Stella-2 with U.S.-based Lumotive. Source links: Lumotive Stella-2 release and Wide Daily CES article.

The key is Lumotive's LCM, or Light Control Metasurface, chip. Mechanical lidar is large, vibration-sensitive, and expensive because it uses a rotating motor. LCM steers the beam by electrically controlling the refractive index on the semiconductor-chip surface, creating a true solid-state approach. Stella-2 is described as smaller than a palm, durable, manufacturable through semiconductor processes, and software-defined in scan range and frame rate.

Interpretation: The source says Namuga is supplying Stella-2 samples for logistics robots to a customer inferred to be a global e-commerce Big Tech company and is undergoing technical validation. Conversion from sample validation to a mass-production contract is the most important event for automotive and robotics sensing re-rating.

6. Financial structure and shareholder policy

Cumulative Q3 2025 revenue was KRW 363.8 billion and operating profit was KRW 24.6 billion. Compared with revenue of KRW 346.1 billion and operating profit of KRW 16.7 billion in the prior-year period, revenue rose about 5.1% and operating profit rose about 47.3%. The source attributes profit growth to yield improvement, higher share in Samsung flagship models, and a higher mix of high-margin OIS models.

| Metric | Cumulative Q3 2024 | Cumulative Q3 2025 / quarter-end | Meaning |

|---|---|---|---|

| Revenue | KRW 346.1B | KRW 363.8B | About +5.1% |

| Operating profit | KRW 16.7B | KRW 24.6B | About +47.3% |

| Operating margin | 4% range | About 6.7% | Manufacturing efficiency and mix improvement |

| Debt ratio | - | About 56% | The source views it as low relative to manufacturing averages |

| Cash-like assets | - | More than KRW 130B | Capacity to self-fund robotics and lidar CAPEX |

Official fact: In December 2025, Namuga decided to cancel 300,558 treasury shares, about 2% of total shares and roughly KRW 5.0 billion in value, according to the source. The cancellation uses distributable profit and is described as preserving paid-in capital of KRW 8.3 billion.

Interpretation: Low leverage, more than KRW 130B of cash-like assets, and treasury-share cancellation reduce the discount attached to a smartphone component stock. Under stable control by Dreamtech, the source also mentions the possibility that part of future FCF could be returned through dividends or additional buybacks/cancellations.

7. Risks and final read

The first risk is end-market and customer concentration. The source identifies more than 90% revenue exposure to smartphones and a specific customer, Samsung Electronics, as the main risk. The response is customer diversification toward Hyundai Motor Group, Google, Waymo, and others, plus expansion into robot sensors and automotive components.

The second risk is timing of new-business monetization. If robotics and XR markets grow more slowly than expected, early R&D spending can hurt near-term profitability. The response is to create cash flow in already-forming markets such as robot-vacuum sensors while investing gradually in lidar and XR.

| Investment checkpoint | Evidence to watch |

|---|---|

| Mobile cash cow | Galaxy S series sales, OIS mix, operating-margin stability |

| Robotics | Samsung robot-vacuum lineup expansion and start of global automaker robot-platform supply |

| XR | Entry into Project Moohan and VR9700-related supply chains |

| LiDAR | Conversion of Stella-2 sample validation into mass-production contracts |

| Shareholder returns | Further dividends, buybacks/cancellations, and FCF use |

The source estimates that the stock still trades like a mobile component supplier at below 10x PER, and that from 2026 onward robot 3D sensors and XR devices could push the multiple toward an AI/robotics solutions profile above 20x PER. Because this is a forecast, the important check is not the multiple itself but whether the new-business revenue share actually rises.

My final read is similar. Namuga still earns most revenue from mobile, but the same technology base can expand into robotics, XR, and automotive sensing. Near-term results will depend on Galaxy S and robot-vacuum modules; the medium-term re-rating depends on industrial robot sensors and Stella-2 mass-production visibility.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224153773998

- 나무가 로봇청소기 3D 센싱 모듈 공급 증가 - 아주경제: https://www.ajunews.com/view/20240717104002264

- 나무가 로봇청소기용 3D 센싱 모듈 공급 순풍 - 아시아경제: https://cm.asiae.co.kr/article/2024071715060907178

- 나무가 글로벌 완성차 3D 센서 공급사 선정: https://namuga.com/kor/invest/news_view.php?v_seqno=316

- NamuGa Selected as Global Supplier of 3D Sensors: https://cm.asiae.co.kr/en/article/2026010710103828072

- Lumotive Stella-2 press release: https://lumotive.com/press-releases/namuga-unveils-stella-2-compact-solid-state-lidar-powered-by-lumotive-at-embedded-vision-summit/

- 나무가 3D 센싱 모듈 발신부 설계능력 - The Elec: https://www.thelec.kr/news/articleView.html?idxno=28336

- NAMUGA Vision Solution partnerships: https://namuga.com/eng/invest/news_view.php?v_seqno=41

- 나무가 내년 신사업 매출 비중 5% 증대 - The Elec: https://www.thelec.kr/news/articleView.html?idxno=40852

- 삼성 로봇청소기 시장 - 동아일보: https://www.donga.com/news/Economy/article/all/20240605/125294987/1

- 삼성 XR 헤드셋 프로젝트 무한 - 빅데이터뉴스: https://www.thebigdata.co.kr/view.php?ud=202412230518264685cd1e7f0bdf_23

- AR/VR - Namuga: https://namuga.com/eng/business/arvr.php

- Enhancing AR/VR with High-Precision Cameras - Namuga: https://namuga.com/eng/invest/news_view.php?v_seqno=177

- 나무가 CES 차세대 3D 센서 스텔라-2 출시 - 와이드경제: https://www.widedaily.com/news/articleView.html?idxno=286496