DEEP RESEARCH · DANAL

Danal: Manna Risk Cleanup and the Stablecoin SaaS Thesis

A combined look at accounting insulation from affiliate losses, digital-asset legislation, and profitability defense through payment data.

0. Bottom line first

For Danal, I see two core points. The Manna Corporation issue is closer to a risk-cleanup event because the stake was already written down to zero book value at the end of 2024. And for stablecoins, Danal's strategy should be read less as direct issuance and more as SaaS infrastructure for issuance and management.

Official fact: The source summarizes Danal's Q3 2025 cumulative results as KRW 169.5bn in revenue and KRW 5.4bn in operating profit. Revenue was down 17% year over year, but the source reads it as the result of reduced low-margin transaction volume and a profit-first strategy.

Interpretation: If past investment failures were the valuation discount, the future variables are cash generation in the payment core, NDS-based bad-debt control, foreigner payments, and stablecoin SaaS.

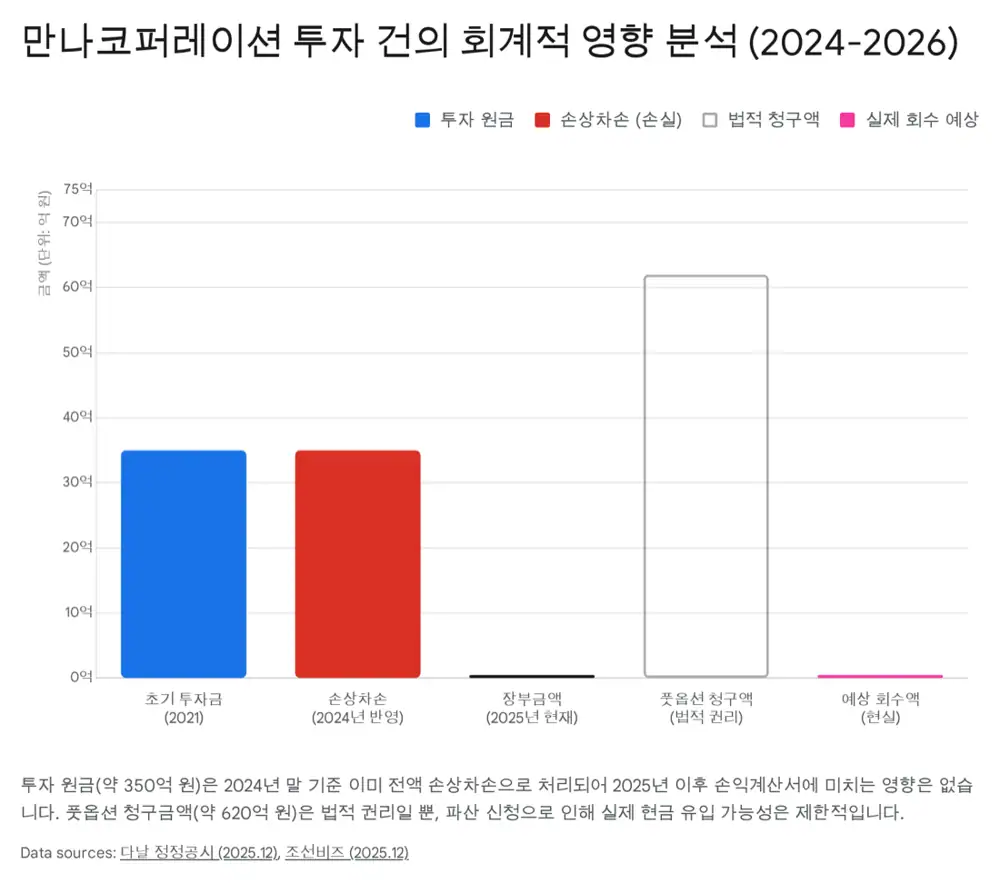

1. Manna Corporation: loss finalization and book cleanup

Official fact: In the corrected disposal disclosure dated December 17, 2025, Danal exercised a put option on 213,183 common shares of Manna Corporation. The claim was KRW 61,969,440,329, about KRW 62.0bn, consisting of roughly KRW 35.0bn principal plus 15% IRR.

Official fact: The source says Danal had already fully recognized the Manna stake's book value as an equity-method loss in the consolidated financial statements at the end of December 2024. Therefore, the source view is that additional impairment in 2025 and 2026 is KRW 0.

Interpretation: The realistic recovery rate should be treated as low given the nature of a platform-company bankruptcy. But from an investor perspective, this is closer to removal of a discount factor than the emergence of a new loss. The source also mentions a content-certified notice for legal action by December 31, 2025 and the profitability-centered management tone under CEO Baek Hyun-sook, appointed in 2024.

2. Stablecoin legislation and Danal's SaaS strategy

The source treats phase-two Digital Asset Basic Act legislation as of January 2026, especially the debate over who may issue won-denominated stablecoins, as Danal's largest policy catalyst.

Bank 51% rule

The source says the Bank of Korea and FSC favor issuance by bank-led consortiums where banks hold a majority, 50%+1 share, citing financial stability and monetary-policy effectiveness.

Fintech opening

The source says some politicians and fintech players want non-financial technology companies such as PayPal or Circle to be allowed to issue.

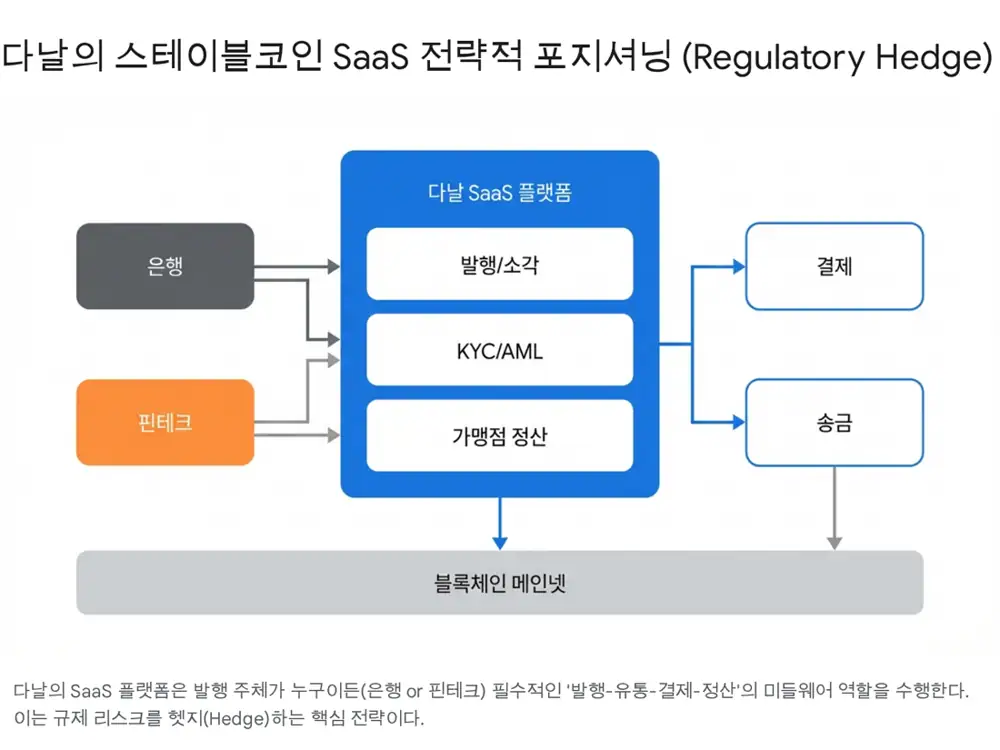

Stablecoin-as-a-Service

The interpretation is that Danal is positioning as middleware for issuance, burning, transfer, payment, settlement, and wallet management rather than only as an issuer.

Official fact: The source says Danal has operated Paycoin through affiliate PayProtocol and has a track record of connecting crypto assets to real payment processes.

- Full-stack solution: an integrated model covering issuance, distribution, payment, merchant settlement, and wallet management.

- Regulatory compliance: AML, KYC, and Travel Rule requirements are presented as embedded system capabilities.

- Legacy integration: a bridge role between credit cards, bank transfers, other legacy financial rails, and blockchain networks.

3. Two policy scenarios

| Scenario | Source interpretation | Danal benefit path |

|---|---|---|

| Bank-exclusive issuance | If the 51% rule passes, bank-centered consortiums will need technical partners. | The thesis is that Danal could supply SaaS to bank consortiums or act as the payment gateway for bank-issued coins. |

| Fintech/big-tech opening | Big-tech firms such as PayPal or Naver Financial could become issuers. | With Paycoin issuance experience and PayPal partnership experience, Danal could participate directly or act as a local partner for won stablecoins. |

Interpretation: If this structure is correct, Danal is not trying to guess the winner of the issuer-regulation debate. It is positioning to provide payment and settlement infrastructure needed by any issuer.

4. Core business and new growth: payment data, foreigner prepaid cards, Paycoin

| Business | Source content | Investment point |

|---|---|---|

| Mobile payments | A mature market, but Danal is presented as the No. 1 player with an estimated 38-40% share. | NDS, New Danal Score, built from more than 20 years of payment and delinquency data, may raise approval rates while lowering bad-debt ratios. |

| K.ONDA | Foreigner-only prepaid card launched in Q4 2024, targeting a 2025 era of 20mn inbound visitors to Korea. | WOWPASS passed 2mn users in 2024 as the first mover, but K.ONDA differentiates through app-based top-up/remittance and Danal's online merchant network. |

| Battery Card | Uses already-launched prepaid debit-card infrastructure. | Could reduce K.ONDA issuance and settlement costs. |

| Paycoin PCI | Service resumed after 2024 relisting on domestic exchanges. The crypto Mastercard converts PCI into USDC at the time of payment. | The source says it can be used at 80mn Mastercard merchants worldwide, implying global cross-border payment infrastructure. |

| Global partnerships | Ripple and Alchemy Pay partnerships are mentioned. | An option to expand from local PG into global payment infrastructure. |

5. Results, CB overhang, and peer valuation

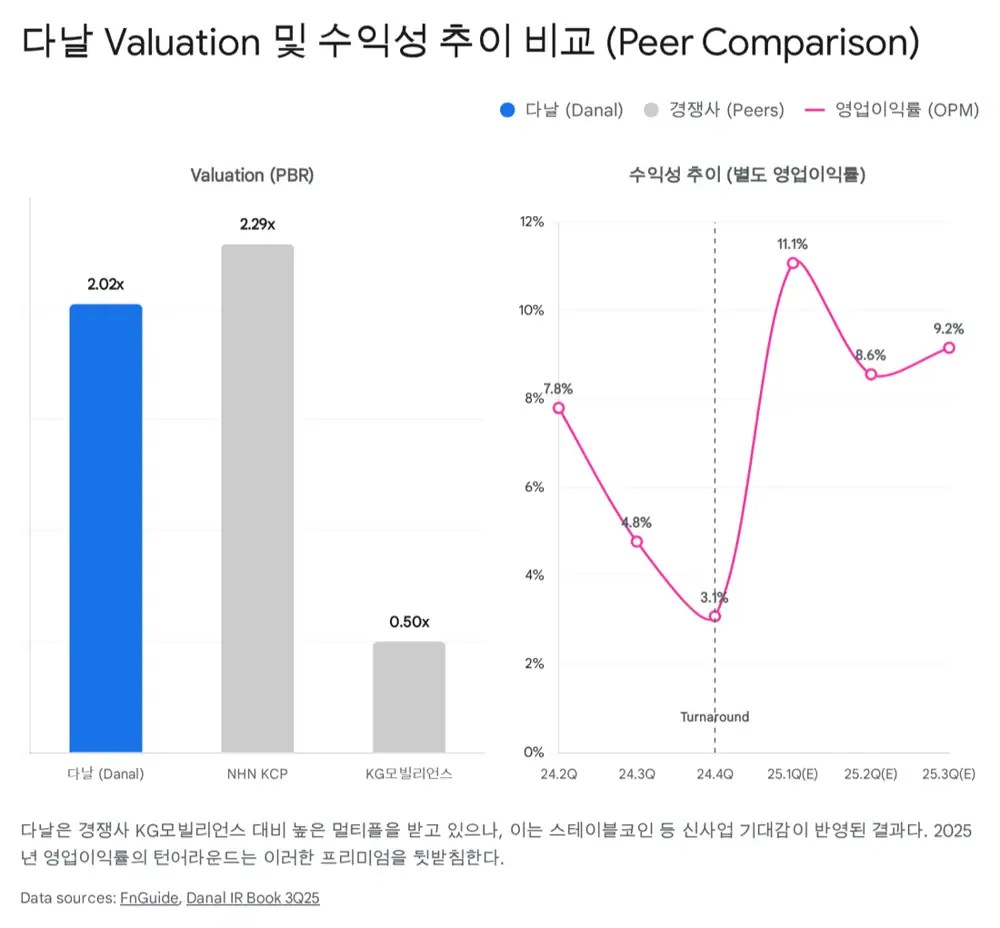

Official fact: Q3 2025 cumulative revenue was KRW 169.5bn and consolidated operating profit was KRW 5.4bn. The source says standalone operating profit was KRW 14.2bn, up 18.7% year over year.

Interpretation: The apparent revenue decline is read as the result of cutting low-margin gift-card and commerce payment volume while focusing on high-margin mobile payments and prepaid cards. Consolidated profit is lower than standalone profit because of overseas investments and stablecoin R&D spending, according to the source.

| 8th CB | Source figure | Meaning |

|---|---|---|

| Issue timing/size | October 2024, KRW 35.0bn | Potential dilution factor |

| Conversion price | KRW 3,136 after refixing | Higher conversion possibility |

| Conversion request | About KRW 14.4bn requested on October 30, 2025 | Read as substantial overhang reduction |

| Financial effect | Debt ratio declines and capital increases on conversion | Dilution and balance-sheet improvement happen together |

| Category | Danal | KG Mobilians | NHN KCP |

|---|---|---|---|

| Main business | Mobile payments, blockchain SaaS | Mobile payments, MVNO | Online PG, overseas merchants |

| Market cap | Estimated KRW 250-300bn | About KRW 170bn | About KRW 600bn |

| 2025E PBR | 0.8-0.9x | 0.49x | 2.3x |

| 2025E PER | N/A | 7.2x | 13.5x |

| Growth driver | Stablecoin, foreigner payments | KG Mobilians Card | Tesla, Apple Pay, others |

6. Scenarios and risks

- Base case: even if stablecoin legislation is delayed, the source expects PBR normalization toward 1.0x through core-business turnaround and foreigner payment growth.

- Bull case: if, after legislation, Danal SaaS becomes a bank standard or a large big-tech partnership becomes visible, the source thesis allows for 15x+ PER high-growth valuation.

- Policy risk: business speed depends on stablecoin issuer rules, interest payment permissions, and bank ownership requirements.

- Execution risk: if the SaaS platform does not convert into real financial-institution and merchant adoption, the gap between theme and earnings remains.

- Overhang risk: remaining CB conversion and share-price volatility still need monitoring.

7. My conclusion

Danal is entering a phase where it can move beyond the discount from past affiliate investment failures, but re-rating must be confirmed through actual revenue and margins from stablecoin SaaS and foreigner payments. I would track Manna's lack of further loss recognition, remaining CB balance, NDS-driven bad-debt ratios, and SaaS partner contracts in that order.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224153690178

- Source 2: https://biz.chosun.com/stock/market_trend/2025/12/18/QIDACCBTH5B2JGDNWLOVOPRWO4/

- Source 3: https://www.womaneconomy.co.kr/news/articleViewAmp.html?idxno=248590

- Source 4: https://marketin.edaily.co.kr/News/ReadE?newsId=04021286645319688

- Source 5: https://www.mk.co.kr/news/stock/11924913

- Source 6: https://www.sisajournal-e.com/news/articleView.html?idxno=418587

- Source 7: https://mobile.newsis.com/view/NISX20260109_0003471462

- Source 8: https://www.sisajournal.com/news/articleView.html?idxno=359493

- Source 9: https://www.ddaily.co.kr/m/page/view/2025111416475115757

- Source 10: https://www.techm.kr/news/articleView.html?idxno=144828

- Source 11: https://www.cuinsight.com/press-release/metallicus-and-daland-partner-to-provide-regulated-stablecoin-and-digital-asset-infrastructure-to-financial-institutions/

- Source 12: https://m.newsprime.co.kr/section_view.html?no=676016

- Source 13: https://www.mk.co.kr/news/stock/8711386

- Source 14: https://m.ddaily.co.kr/page/view/2026011916591408707

- Source 15: https://www.joongangenews.com/news/articleView.html?idxno=466051

- Source 16: http://www.iwet.co.kr/news/articleView.html?idxno=73846

- Source 17: https://www.dt.co.kr/article/11659938

- Source 18: https://xangle.io/insight/events/685e2710ca96040bfdebe970

- Source 19: https://v.daum.net/v/20251114171515732?f=p

- Source 20: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251030000744&rcpno=20251030000744&orgid=K&tran=Y&langTpCd=0

- Source 21: https://comp.fnguide.com/SVO2/asp/SVD_Comparison.asp?pGB=1&gicode=A060250&cID=&MenuYn=Y&ReportGB=&NewMenuID=106&stkGb=701

- Source 22: https://wcomp.fnguide.com/CompanyInfo/Comparison?cmp_cd=060250

- Source 23: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A046440