DEEP RESEARCH · KAKAOPAY

Kakao Pay Deep Dive: Fundamental Turnaround Under Governance and Regulatory Pressure

A combined review of Alipay overhang risk, won stablecoin regulation, and the 3Q25 operating turnaround

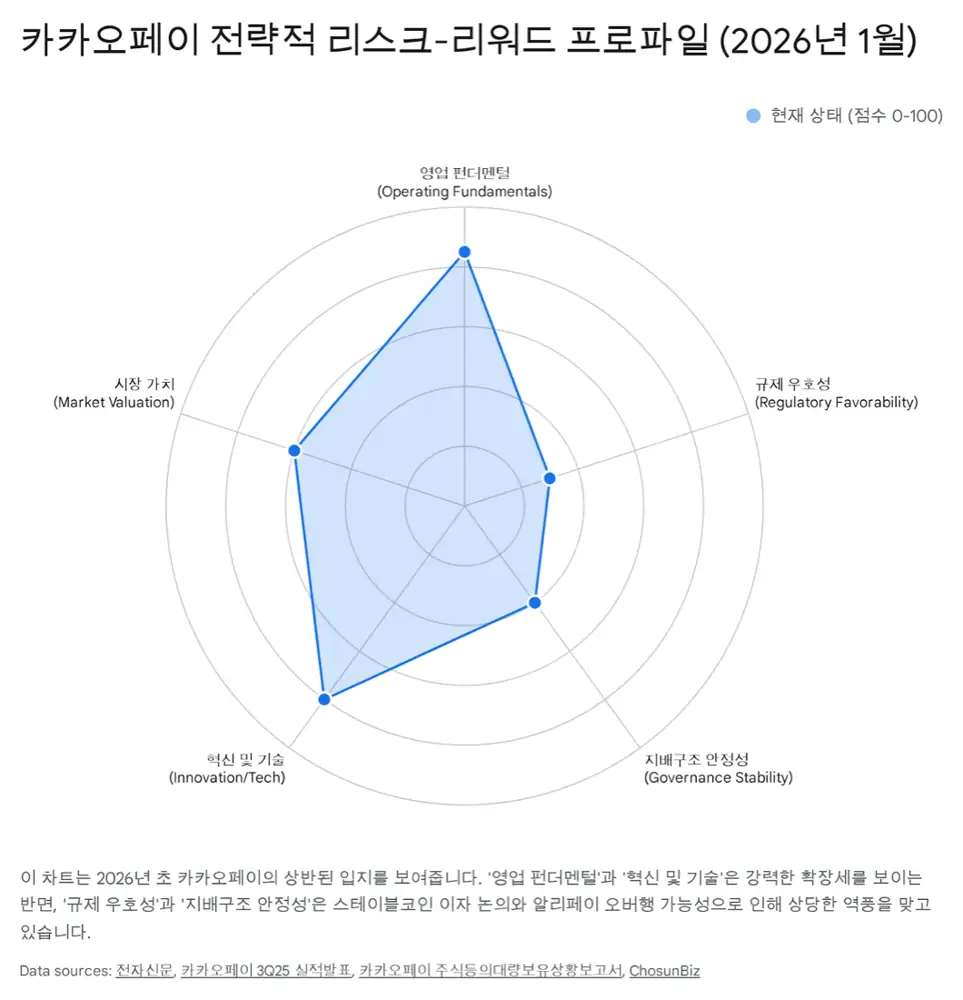

0. Bottom line first

As of January 2026, Kakao Pay sits where a real fundamental turnaround collides with external risk. I see the 3Q25 earnings improvement as meaningful progress, but until the Alipay share-return issue and bank-led stablecoin debate are resolved, I would frame the stock more as a watch-and-scale or trading idea than an aggressive buy.

Alipay overhang

As of January 14, 2026, 11,648,791 shares returned after a stock-lending agreement ended, lifting Alipay's holding to 36,577,072 shares, or 27.07%.

Bank stablecoins

If interest is allowed only on bank-issued coins, cash could move from non-interest-bearing Kakao Pay Money to bank stablecoins.

3Q25 turnaround

3Q25 revenue was KRW 238.4 billion, operating profit KRW 15.8 billion, and net income KRW 19.1 billion, the company's highest quarterly profit.

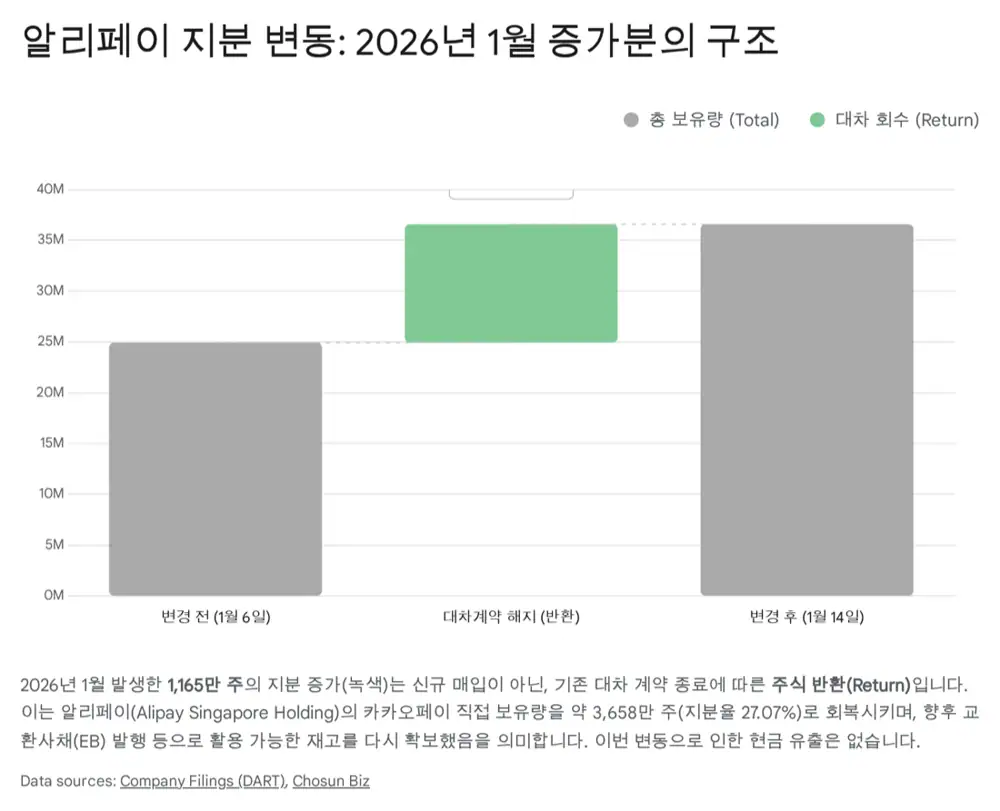

1. Alipay share change: return, not purchase

Official fact: The source says the Alipay Singapore Holding stake increase disclosed on January 16, 2026 was not strategic buying but a “share recovery following termination of a stock-lending agreement.” The recovered amount was 11,648,791 shares, increasing total holdings from 24,928,281 shares to 36,577,072 shares.

| Item | Source number | My read |

|---|---|---|

| Disclosure reference date | January 14, 2026 | The starting point of the January supply-demand issue |

| Returned shares | 11,648,791 shares | Shares previously lent moved back into Alipay's direct holding |

| Total holding | 36,577,072 shares | A sharp increase from 24,928,281 shares |

| Ownership ratio | 27.07% | Potential disposal by the second-largest shareholder comes back into focus |

| Potential sale inventory | About 8.6% of total shares outstanding | Could become resistance whenever the share price rises |

The background is Alipay's exchangeable bond issuance in July and October 2025. EB investors and underwriters borrowed Kakao Pay shares from Alipay for delta hedging, and the January return suggests that part of the lending or hedge position ended.

Interpretation: I do not read this stake increase as a bullish purchase signal. Shares under lending are harder for Alipay to dispose of freely; once returned, they can again be used for a block deal or as collateral for another EB. Alipay has already reduced its stake through block deals of 5 million shares in June 2022 and 2.95 million shares in March 2023, so this looks closer to overhang being reloaded.

2. Stablecoin regulation: defending the prepaid-balance model

Official fact: The source says the Korea Federation of Banks gathered major commercial banks on January 15, 2026 to discuss a bank-centered single stablecoin issuance model and permission to pay interest. The banks' rationale is deposit defense and extending deposit-taking into tokenized digital form.

Kakao Pay Money is the base for payments and transfers, but it does not pay interest. If bank stablecoins offer annual interest of 2-3%, rational users would have an incentive to move idle cash into bank coins. Prepaid balances keep users inside the platform, so lower balances could reduce visit frequency, time spent, and cross-selling opportunities in loans and investments.

Interpretation: The U.S. GENIUS Act, which generally bars stablecoin issuers from paying holders interest or yield, supports the fintech industry's argument. But under the source timeline, the ruling party was expected to finalize a draft around January 20, while opposition parties resisted a bank-monopoly model, so the legislative outcome remains central to Kakao Pay's valuation discount.

Kakao Pay's response has two tracks. First, it is trying to compete on convenience and universality through a super wallet that can hold NFTs, local currencies, and different kinds of stablecoins. Second, it is leaning on Kakao Pay Securities accounts, where deposit-use fees can legally be paid, to offset the limits of non-interest prepaid balances.

3. 3Q25 earnings: the financial-platform shift in numbers

Official fact: In 3Q25, Kakao Pay recorded revenue of KRW 238.4 billion, operating profit of KRW 15.8 billion, and net income of KRW 19.1 billion. EBITDA was KRW 24.1 billion, up 1,306% year over year.

| Category | Source number | Meaning |

|---|---|---|

| Financial services | KRW 94.7 billion, YoY +72.0%, 40% of revenue | Higher-margin securities and insurance are becoming the growth axis |

| Platform services | YoY +69.2% | Advertising and card-recommendation monetization is progressing |

| Payment services | KRW 129.7 billion, YoY +5.5% | Still the largest revenue source, but growth is stabilizing |

| Stickiness | 27.8% | DAU as a share of MAU improved |

| ATPU | 75 transactions, YoY +43% | Users are doing more payments, transfers, investing, and insurance activity |

Interpretation: These earnings show Kakao Pay moving from a lower-margin payments app toward an investment, insurance, and wealth-management app. Revenue scale is starting to create operating leverage, while user engagement is becoming a defense asset against the banks.

4. Valuation: discount factors and rerating conditions

The source gives a 12-month average analyst target price of about KRW 52,370 as of January 2026, versus a current trading range of KRW 48,000-51,000. It also cites roughly 22.9x 12-month forward EV/EBITDA, expected 2026 operating-profit growth of +38-47%, and P/B around 1.9x.

Bull case

- The Digital Asset Basic Act allows fintech companies to issue or distribute stablecoins.

- Kakao Pay Securities turns profitable on a full-year basis.

- Overseas payments through Alipay+ become material and support valuation expansion.

Bear case

- Banks monopolize the right to pay interest on stablecoins.

- Alipay uses returned shares for another block deal.

- If overhang and regulatory risk surface together, the stock could remain near the lower end of its range or correct.

5. Checklist

- National Assembly discussion of the Digital Asset Basic Act expected in late January to early February

- Whether interest is allowed on bank-issued stablecoins

- How Alipay uses the 11,648,791 returned shares

- Whether Kakao Pay Securities turns profitable and financial services keeps its revenue share

- Whether stickiness of 27.8% and ATPU of 75 transactions continue to improve

In conclusion, I view Kakao Pay as a company between growing pains and a possible step-up. The revenue model has diversified and the user base has become sturdier, but overhang and regulatory risk still remain as valuation discounts.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224153680263

- Reference 1: Shinhan Securities cautions Kakao Pay on overhang risk, maintains neutral rating

- Reference 2: The Stablecoin Dilemma: Between Bank Control and Fintech Innovation in Korea's New Digital Asset & Cryptocurrency Act

- Reference 3: Alipay accelerates Kakao Pay divestment as stock price plunges after bond issuance

- Reference 4: Alipay Issues Another Exchangeable Bond Backed by Kakao Pay Shares

- Reference 5: Ant Group's Stake Sale Sparks Concerns Over Kakao Pay Stock Volatility

- Reference 6: South Korean Banks Push for Interest-Bearing Won Stablecoin

- Reference 7: What You Need To Know About the New Stablecoin Legislation

- Reference 8: GENIUS Act means for stablecoin issuers and banks

- Reference 9: Kakao Group digital financial ecosystem report

- Reference 10: Hana Financial Group consortium report

- Reference 11: KakaoPay Corp Q3-2025 Earnings Call

- Reference 12: KakaoPay Corp stock forecast and price target

- Reference 13: KakaoPay Corp stock price

- Reference 14: Kakao Pay public comps and valuation multiples

- Reference 15: Kakao research report

- Reference 16: Kakao Pay valuation