DEEP RESEARCH · NEUROMEKA/ROBOT AUTOMATION

Neuromeka: Vertical Integration of the Robot Automation Value Chain and Platform Expansion

A review of the company's move from collaborative robots into RaaS, MaaS, and humanoid platforms

0. Bottom line first

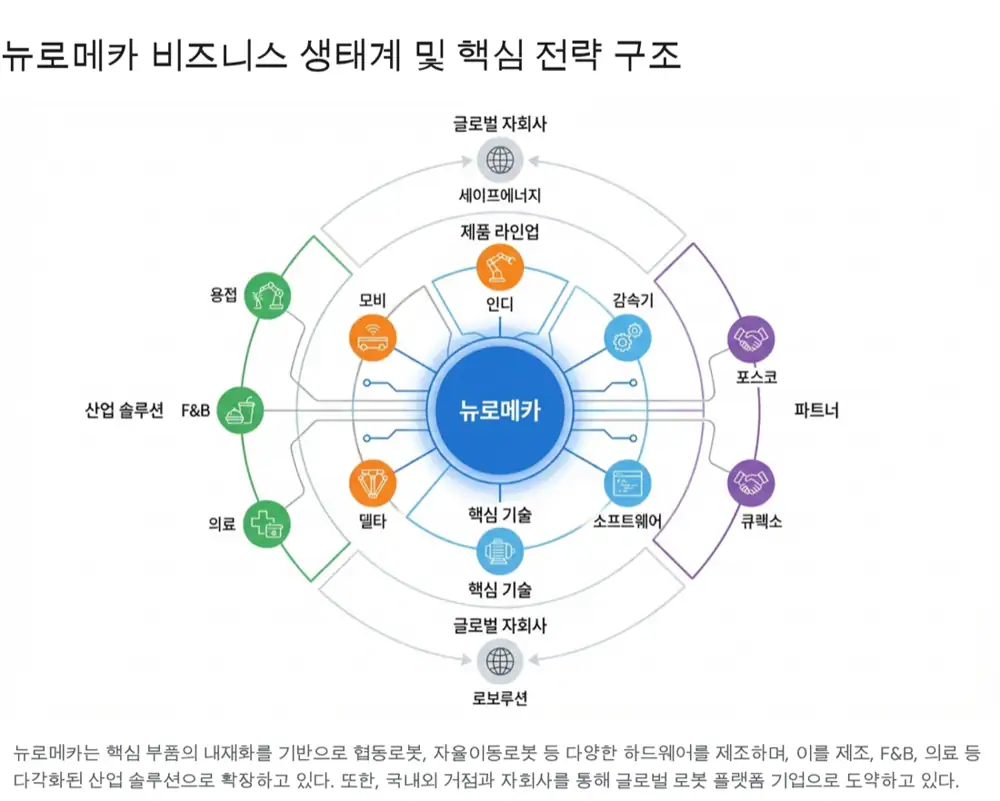

The source views Neuromeka not as a simple collaborative-robot manufacturer, but as a robot platform company combining internalized core parts, control software, industry-specific turnkey automation, and RaaS/MaaS. Vision 2026, Robolution and Safe Energy, and partnerships with POSCO, Kyochon F&B, and Curexo are presented as the key axes for rerating over the next three years.

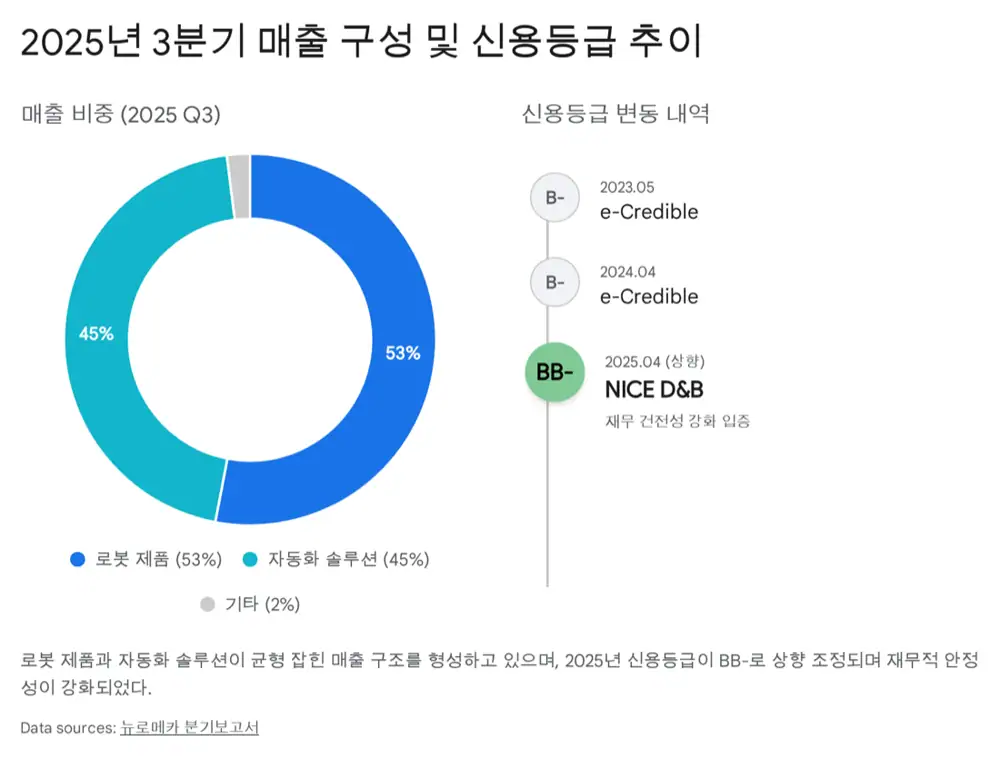

For me, the question is whether Neuromeka can move from “selling robots” to “designing, manufacturing, and operating robot platforms.” As of 3Q25, robots represented 53% of revenue and automation solutions 45%, a balanced mix that the source interprets as a base for expansion into manufacturing, F&B, and medical applications.

1. Industry background and Neuromeka's position

Official fact: The source says the global robot market is shifting from Robot 1.0, centered on traditional industrial robots, to Robot 2.0, centered on collaborative and service robots that coexist and work with humans. The drivers are shrinking labor forces, wage increases, and demand for flexibility in manufacturing sites.

Korea is also described as ranking first globally in robot density, measured by robots per 10,000 manufacturing workers. In that environment, Neuromeka is presented as a company that has built a flexible platform extendable from collaborative robots into manufacturing, F&B, medical, and service areas.

2. Company history and management

| Period | Key events | Meaning |

|---|---|---|

| 2013-2016 | Founded on February 14, 2013, in Namyangju, Gyeonggi-do. CEO Park Jong-hoon holds a POSTECH PhD in mechanical engineering. Venture certification and corporate R&D center in January 2014, headquarters moved to Seongsu in July 2014, and the first model Indy RP launched in October 2016. | The company focused early on control software and algorithms rather than hardware alone. |

| 2017-2021 | Launched Indy 3, 5, 10, and 7 models, with Indy7 in September 2017. Won the Korean Robotics Society Technology Award in December 2017, was selected among 100 technologies to lead Korea, and won Robot Company of the Year for three consecutive years from 2017 to 2019. Opened the CI Lab with POSTECH in 2018, launched IndyEye and Indy12 in 2019, and established a Vietnam subsidiary. | Built the collaborative-robot line and external recognition. |

| 2022-present | Listed on KOSDAQ as a technology-growth company on November 4, 2022. IPO proceeds supported the 2023 Pohang factory expansion and core-part internalization. In 2025, Neuromeka established Safe Energy, began robot platform foundry work through Robolution, and had five unlisted subsidiaries. | The company is expanding from manufacturer to robotics group and ecosystem operator. |

The key people are CEO Park Jong-hoon and director Shim Gyu-bun. The source describes Park as a technical leader in robot control and automation, while Shim, as head of finance operations and disclosure officer, manages listed-company finance and disclosure work.

3. Business model: manufacturing and automation solutions

Official fact: As of 3Q25, Neuromeka's revenue mix was 53% robots, including collaborative robots, and 45% automation solutions.

Robot manufacturing

Manufactures and sells hardware platforms including collaborative robot Indy, autonomous mobile robot Moby, and delta robot D.

Turnkey automation

Combines robot hardware with process-specific software and peripherals such as grippers and sensors for F&B, welding, machine tending, and medical use cases.

Robot subscription

Provides robots on a monthly subscription basis to SMEs and small businesses that find upfront adoption costs burdensome, targeting recurring revenue.

Robot foundry

Designs, manufactures, and mass-produces robots to customer specifications. The source cites the Curexo medical-robot partnership as a representative example.

4. Moat: parts internalization and partnerships

Neuromeka's economic moat is described as both technical and relational. Technically, the company develops and produces motors, reducers, brakes, and other core drive parts that account for about 60-70% of robot cost, and 100% domestic internalization of collaborative robots improves resilience to FX and supply-chain variables.

- Sensorless collision detection: Detects collisions through motor-current changes without expensive torque sensors, lowering cost while preserving safety.

- IndyEye: An in-house deep-learning vision solution that supports object recognition and robot work without a separate high-cost vision system.

- POSCO: A partnership that provides robot automation references in harsh steel-industry environments.

- Kyochon F&B: Cooperation with Korea's top chicken franchise, seen as a way to set standards in F&B automation.

- Curexo: A medical-robot partnership that signals Neuromeka's manufacturing quality can meet medical-grade requirements.

The source body includes the helper UI link http://googleusercontent.com/assisted_ui_content/3.

5. Financials and funding: what is confirmed and what is missing

Official fact: The source explicitly says detailed three-year revenue, operating-profit, and net-income figures as of 3Q25 cannot be directly confirmed because the report excerpt is missing. Instead, it uses credit-rating changes as evidence of improving financial health.

| Date | Credit rating | Agency |

|---|---|---|

| May 2023 | B- | eCredible |

| April 2024 | B- | eCredible |

| April 2025 | BB- | NICE D&B |

Cash flow is discussed qualitatively because precise figures are lacking. The source says operating cash flow may have been weak through 2023 and early 2024 due to aggressive R&D and hiring, but could have become more visible in 2025 as large orders from Curexo, POSCO, and others ramped and the source's cited “2024 annual revenue No. 1” note was reflected. The 2023 Pohang factory and 2025 Safe Energy subsidiary are investment-cash-outflow factors.

The source is also cautious on ownership. Founder CEO Park Jong-hoon is the largest shareholder, but the exact stake is not confirmed because page 168 of the quarterly report detail is missing. Funding history is summarized as pre-IPO Series A, B, and C rounds, the 2022 KOSDAQ IPO, post-listing convertible bonds, and Robolution's KRW 2.0 billion pre-Series A investment in 2025.

6. Competitive landscape and differentiation

| Competitor | Source description | Comparison point for Neuromeka |

|---|---|---|

| Doosan Robotics | Domestic collaborative-robot market-share leader with strong capital, product lineup, and global sales channels | Neuromeka must differentiate through cost effectiveness and parts internalization for SME targets. |

| Rainbow Robotics | Samsung-invested technology company with humanoid technology, parts internalization, and quadruped and other form factors | Directly comparable on humanoids and parts internalization. |

| Universal Robots | Danish global collaborative-robot leader with reliability and the UR+ ecosystem | Neuromeka is smaller in global ecosystem scale, so domain-specific turnkey solutions are the niche. |

Interpretation: Neuromeka's distinction is that it does not compete only through generic robot sales. It lowers cost through parts internalization, earns MaaS revenue by manufacturing robots for others, and lowers adoption barriers with turnkey domain solutions such as Kyochon F&B, POSCO welding, and Curexo medical robots.

7. Growth strategy and risks

The source says Neuromeka is executing Vision 2026 and has global footholds in Texas in the U.S., Jiangsu and Hangzhou in China, and Ho Chi Minh City in Vietnam. The U.S. is an automation-demand market supported by reshoring, while Vietnam is both a Southeast Asian production base and a potential automation market.

- Humanoids: The Physical AI humanoid platform Eir, planned for CES 2026, is presented as a next-generation growth driver.

- Parts localization: Localization of actuators for humanoid joints is a strategy to secure a core-component supplier position as the market evolves toward humanoid robots.

- Policy support: Korea's Fourth Intelligent Robot Master Plan and related policies aim to develop robotics as a national core industry by 2030.

- 2026 policy focus: Policy funds may concentrate on robot adoption and service-robot market creation, benefiting F&B, care, and medical robot lineups.

Risks

- Overhang: Outstanding convertible bonds and other instruments issued during listing and financing could dilute shares if converted. The source says detailed balances require checking page 143 of the report.

- Intensifying competition: Low-cost Chinese robot companies and Korean large-company robot expansion by Doosan, Hanwha, Samsung and others are threats.

- Downstream cycles: Weak manufacturing, construction, or restaurant conditions could reduce robot adoption spending. Diversification into medical, fire-safety, and Safe Energy-related fields matters.

8. Final view: the small/mid-cap robot top-pick logic

The source says Neuromeka deserves attention as a top pick among small and mid-cap robot stocks. The logic is that its market cap is relatively lighter than Rainbow Robotics or Doosan Robotics, and the robot foundry MaaS model can raise the probability of an earnings turnaround.

The three-year outlook depends on whether Neuromeka captures both robot-parts localization and service-robot market expansion. CES 2026 humanoid disclosure is a short-term momentum point, while subsidiary growth is framed as a medium- to long-term rerating factor. My checklist is Robolution's actual orders, recurring RaaS revenue, repeated expansion of POSCO/Kyochon/Curexo references, and the size of CB dilution.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224152559219

- Source helper UI link: http://googleusercontent.com/assisted_ui_content/3

- Fourth Intelligent Robot Master Plan - KDI Economic Education: https://eiec.kdi.re.kr/policy/callDownload.do?num=247119&filenum=2&dtime=20240121104657

- CES 2026 robotics industry outlook: https://contents.premium.naver.com/argos337/argos/contents/251231141919815et

- EBN Curexo supply-contract article: https://www.ebn.co.kr/news/articleView.html?idxno=1677476

- Neuromeka (348340) Naver research PDF: https://ssl.pstatic.net/imgstock/upload/research/company/1683155140361.pdf

- Neuromeka POSCO benefit-sharing contract: https://www.neuromeka.com/post/%EB%89%B4%EB%A1%9C%EB%A9%94%EC%B9%B4-%ED%8F%AC%EC%8A%A4%EC%BD%94%EC%99%80-%EB%A1%9C%EB%B4%87-%EC%9E%90%EB%8F%99%ED%99%94-%EC%84%B1%EA%B3%BC%EA%B3%B5%EC%9C%A0%EC%A0%9C-%EA%B3%84%EC%95%BD-%EC%B2%B4%EA%B2%B0-%EC%B5%9C%EB%8C%80-5%EB%85%84%EA%B0%84-%EC%9E%A5%EA%B8%B0%EA%B3%84%EC%95%BD%EA%B6%8C

- Machinery/robotics field-note PDF: https://drive.google.com/open?id=1xNsQUXrRU2NDoxbZUaaSqfVh9oIuZ5gu

- Collaborative robot market growth and trends: https://www.globalgrowthinsights.com/ko/market-reports/collaborative-robots-market-100872

- Robot medium/long-term strategy material: https://iacf.ajou.ac.kr/iacf/info/contest02.do?mode=download&articleNo=359281&attachNo=317285