DEEP RESEARCH · ISU Specialty Chemical

ISU Specialty Chemical: the H₂S moat and lithium sulfide solid-state battery option

A Q/P/C review of the precision-chemical cash cow, TDM oligopoly, and Li₂S commercialization roadmap

0. Bottom line first

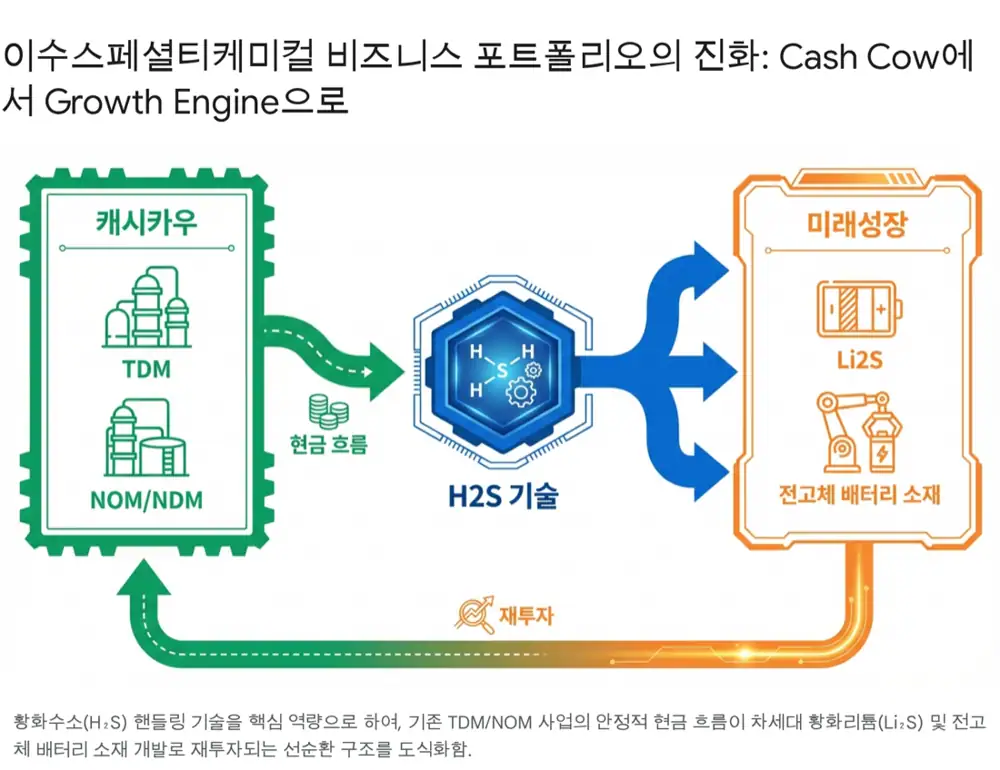

My core view is that ISU Specialty Chemical is not just a precision chemical company. Its ability to safely handle difficult hydrogen sulfide, H₂S, connects today's TDM cash cow with tomorrow's Li₂S solid-state battery material option.

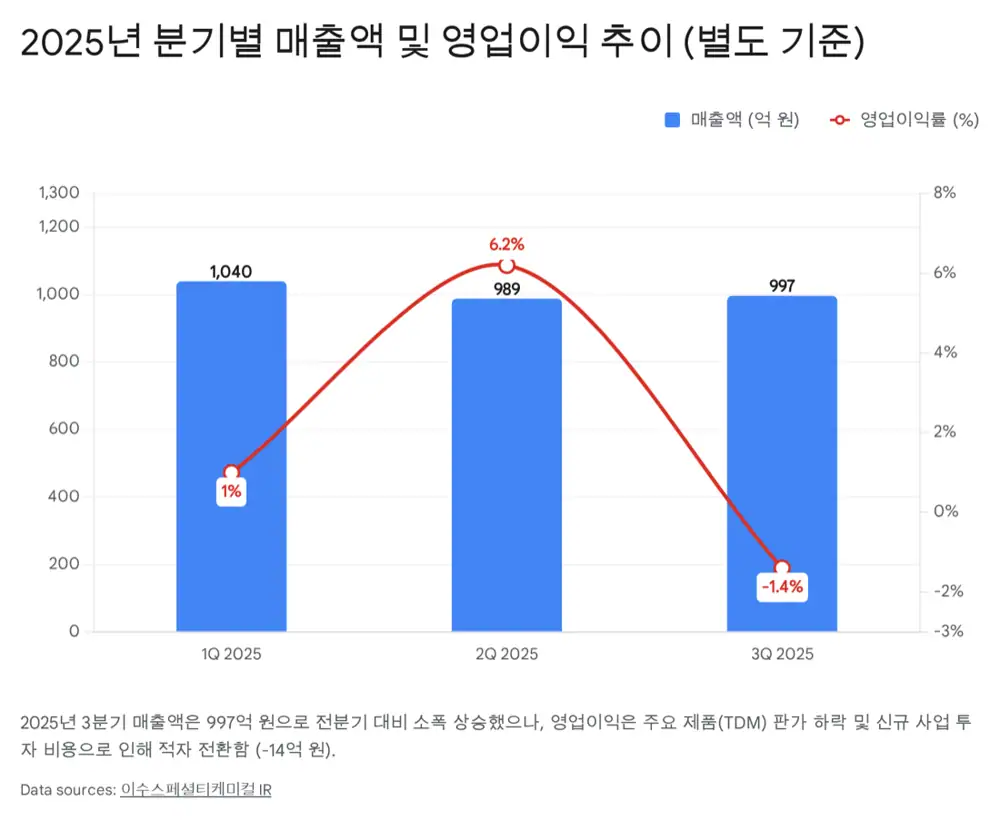

Official fact: The source highlights a corrected disclosure dated December 16, 2025 for a roughly KRW 23bn supply contract with China Petroleum Materials, equal to 19.6% of recent revenue and running through March 2026.

Interpretation: Weak TDM pricing and the Q3 2025 operating loss of KRW 1.4bn are cyclical pressure, but H₂S integration and oligopoly structure could make the legacy business a buffer during new-business investment.

TDM oligopoly

The source lists ISU Specialty Chemical, Arkema, and Chevron Phillips as the three commercial producers.

KRW 23bn

The CPMC contract shows that ISU's material position remains relevant in the Chinese ABS chain.

20t → 150t → 500t+

The roadmap moves from a 20-ton demo plant to a 150-ton commercial facility, with design capacity expandable above 500 tons.

1. Company essence: reshaped into a precision-chemical pure play

ISU Specialty Chemical was created in May 2023 through the spin-off of ISU Chemical's precision-chemical and all-solid-state battery material businesses. The source argues that the split made the high-margin precision-chemical business and solid-state material potential more visible after being masked by the cyclicality of petrochemicals.

In April 2024, the company absorbed the precision-chemical sales business of ISU Exachem through a small-scale merger. The purpose was to unify manufacturing and sales, reduce sales commission leakage, speed pricing and production decisions, and improve technical sales for new materials such as Li₂S.

2. Legacy business: TDM and NOM/NDM resilience

Official fact: TDM is an essential additive used to control molecular weight in SBR and ABS polymerization, and the source emphasizes customer lock-in because changing suppliers can affect product quality.

| Product | Use | Source investment point |

|---|---|---|

| TDM | SBR and ABS resin polymerization additive | Global oligopoly and structural demand from Chinese ABS capacity expansion |

| NOM | Raw material for LED and semiconductor chemicals | A high-value niche linked to IT industry growth |

| NDM | Lubricant additives, metalworking fluids, optical film coatings | Sales volume increased after new Asian customers in Q3 2025 |

| Base-oil and others | Complementary precision chemicals | The source cites 28% quarter-on-quarter sales-volume growth. |

Interpretation: European ABS utilization weakness and low-price competition pressured TDM pricing, but a producer with structural cost advantage can usually endure a downcycle longer. ABS utilization recovery in 2026 is the key legacy-business watchpoint.

3. Solid-state material: why Li₂S is the option

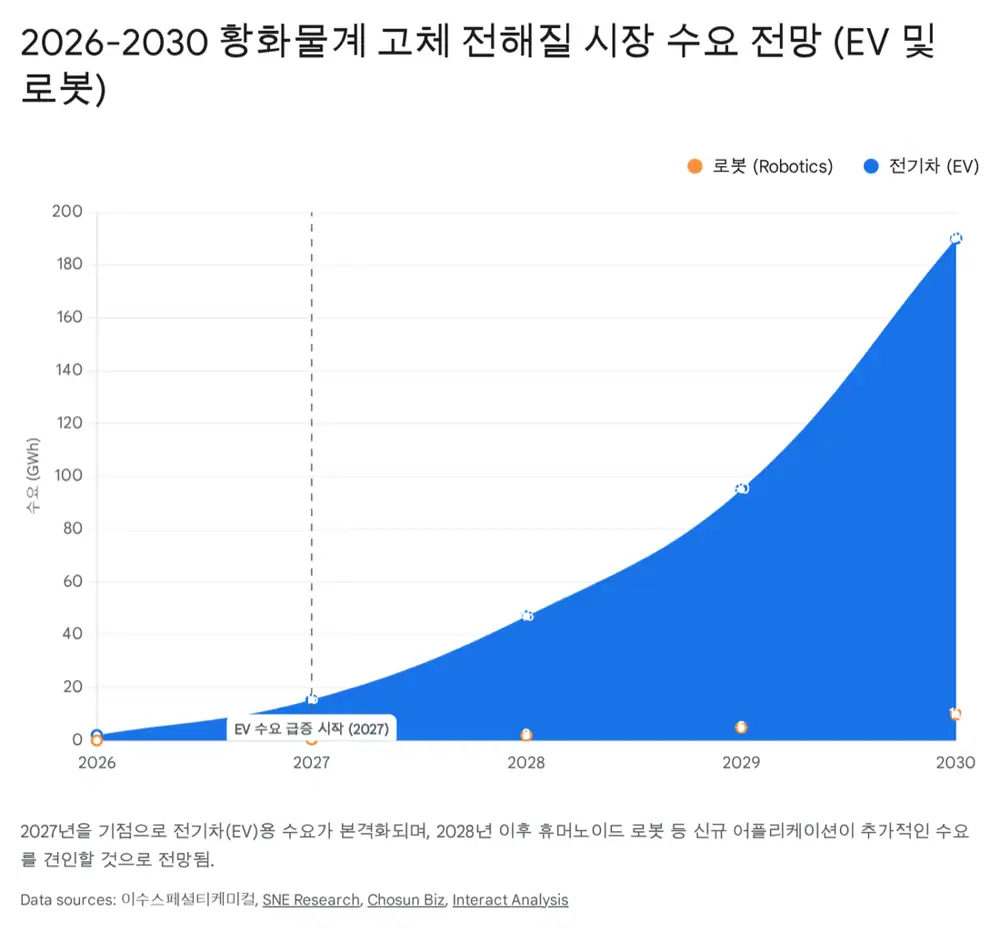

All-solid-state batteries replace liquid electrolyte with solid electrolyte, improving fire safety and energy density. The source argues sulfide chemistry is favored for EV applications because of ion conductivity and formability, and it links that to adoption by major players such as Samsung SDI, Toyota, and CATL.

Lithium sulfide, Li₂S, is the key raw material for sulfide solid electrolytes. The source says it can account for about 70-80% of electrolyte cost, while difficult manufacturing and high price have been commercialization bottlenecks. ISU's differentiator is a wet process using relatively cheaper lithium hydroxide, LiOH, and internally supplied H₂S instead of expensive lithium metal.

LiOH + H₂S

A process designed to lower cost by using cheaper raw materials and integrated H₂S supply.

High purity control

Solid-state materials are highly moisture-sensitive, so ultra-high-purity chemical know-how matters.

KRW 85.2bn investment

The source describes an August 2025 board decision to invest in a dedicated Li₂S plant in Ulsan.

4. Capacity and partnership roadmap

| Timing | Event | Meaning |

|---|---|---|

| November 2022 | 20-ton-per-year demo plant completed | Moved beyond lab scale into sample production |

| First half 2023 | Samsung SDI's Suwon S-Line began operation | Sample supply and quality certification process |

| September 2025 | Ulsan commercial facility construction began | Preparation for initial 150-ton commercial capacity |

| June 2026 expected | Target plant completion | Aligned with customer mass-production schedules around 2027 |

| Later | Designed for potential expansion above 500 tons | Stepwise quantity growth if demand is proven |

On partnerships, the source mentions Samsung SDI, an MOU and sample supply with Solid Power, Solid Power's BMW and Ford backing, possible connection through SK On, and joint development with Korean material companies such as EcoPro BM, Lotte Energy Materials, and Heesung Catalyst.

5. End market: beyond EVs into humanoid robots

The source stresses that early solid-state battery demand should not be viewed only through EVs. Humanoid robots operate near people, so fire safety is critical, while limited body space makes high energy density valuable for longer operating time.

Interpretation: EV adoption can be delayed by price sensitivity, but special-purpose markets such as robots and UAM may value performance and safety first. Those niches could become the early demand bridge for Li₂S.

6. Q/P/C and risks

| Category | Positive factor | Risk to verify |

|---|---|---|

| Quantity | CPMC contract and potential volume growth after the 2026 Li₂S plant | Customer mass-production delays in solid-state batteries |

| Price | Early Li₂S scarcity and customized TDM specifications | TDM price decline and Li₂S ASP decline after scaling |

| Cost | Integrated H₂S and lower logistics/storage burden | Fixed costs from the new plant, hiring, and financing |

| Strategic risk | IRA and supply-chain preference away from China | Chinese entry into Li₂S and overhang from CBs or equity issuance |

On current numbers alone it can look like a chemical stock, but the true risk is the timing of solid-state commercialization. The sequence to monitor is Li₂S plant completion, concrete supply contracts with partners such as Samsung SDI, and real demand from robots or other applications.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224152323244

- ChosunBiz humanoid batteries: https://biz.chosun.com/en/en-industry/2026/01/18/UT5LZAWMPZA33KW6OMKA7XXMAI/?outputType=amp

- SMM ISU lithium sulfide project: https://news.metal.com/newscontent/103526166/overseas-solid-state-battery-construction-begins-on-south-koreas-150-mt-lithium-sulfide-project-in-yisu-with-an-investme

- Samsung SDI BMW Solid Power agreement: https://www.samsungsdi.com/sdi-now/sdi-news/4565.html

- Interact Analysis humanoid robots and batteries: https://interactanalysis.com/insight/humanoid-robots-and-lithium-ion-batteries/

- Newspim humanoid robots: https://www.newspim.com/news/view/20260114000416

- ChosunBiz Korean battery opportunity: https://biz.chosun.com/industry/company/2026/01/18/3Y2N2L3EERCSHHA5A6ANCSAJRE/