DEEP RESEARCH · Lake Materials

Lake Materials: TMA Platform and Solid-State Li2S Investment

A review of Sejong Venture Valley, lithium sulfide, High-K precursors, and catalyst optionality.

0. Bottom line first

Lake Materials is a platform extending TMA core technology into semiconductor precursors, solar, catalysts, and solid-state battery materials. The December 2025 Sejong Venture Valley correction reads as progress toward a lithium sulfide production base.

1. Sejong Venture Valley investment

Official fact: The investment is KRW 19,479,300,000, about KRW 19.5bn, equal to 22.45% of 2022 year-end consolidated equity of KRW 86.7bn. The end date moved from December 30, 2025 to March 31, 2026 because ownership transfer was delayed by unresolved industrial-complex cost finalization.

Interpretation: I read this as timing slippage in ownership transfer and cash execution, not a broken business plan. The source also notes the company’s view that manufacturing-facility investment had already been completed.

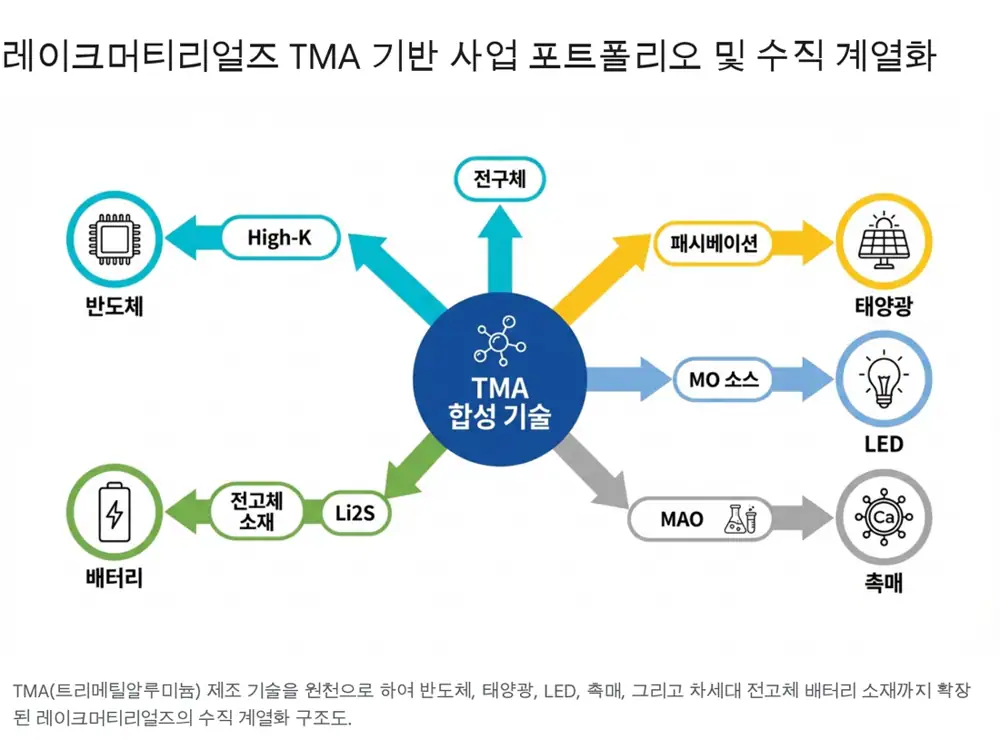

2. From TMA to Li2S

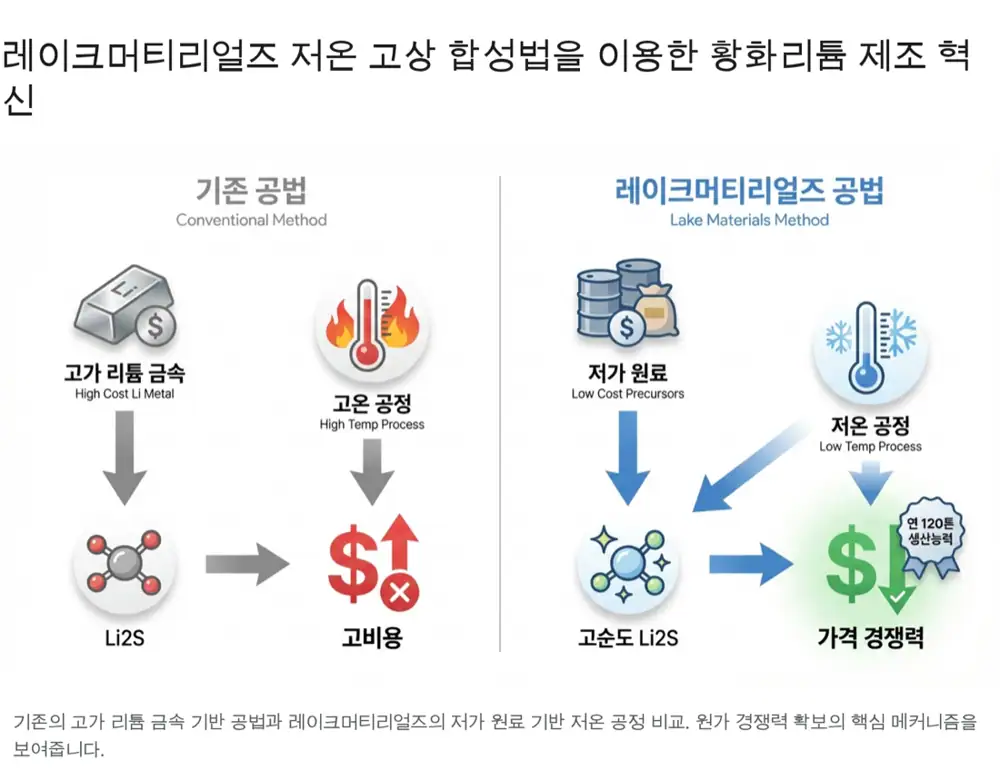

Official fact: The source gives lithium sulfide price at roughly USD 12,000/kg and says the company has low-temperature technology using cheaper lithium compounds to produce high-purity Li2S. It also mentions 120 tons per year capacity completed in late 2023.

3. Customers and numbers

| Item | Source figure/content | Check point |

|---|---|---|

| SK hynix | About 47.1% High-K share | HBM precursor orders |

| Samsung SDI | 2027 solid-state target | Li2S sample tests |

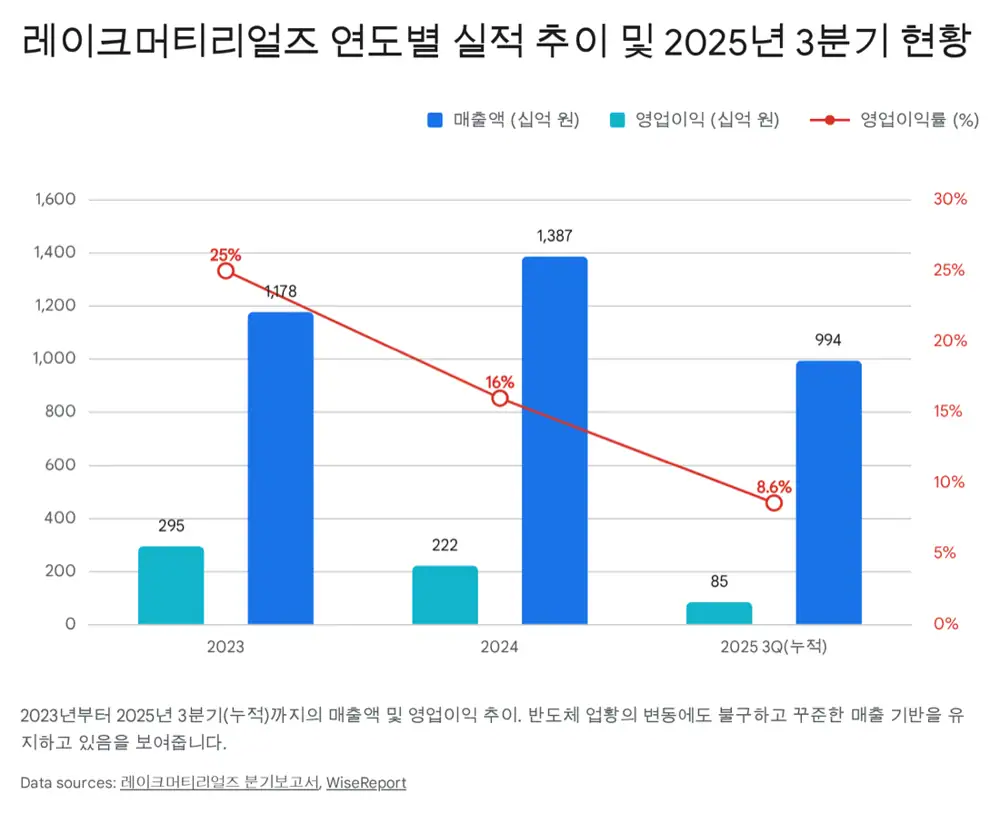

| Q3 2025 cumulative | Revenue KRW 99.4bn, OP KRW 8.5bn | Recovery after adjustment |

| Cash/current assets | KRW 24.6bn, KRW 133.2bn | Land-purchase liquidity |

| 2028 target | Revenue KRW 250bn, OP KRW 50bn | 20% OPM |

4. Risks and conclusion

- Valuation burden at roughly 70-80x PER.

- Potential delay in solid-state battery commercialization.

- Lithium and other raw-material volatility.

- Debt ratio around 172% and future CAPEX burden.

For 2026, the key proof points are Sejong ownership transfer, initial Li2S revenue, HBM precursor order recovery, and overseas catalyst sales.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224152321887

- Source 2: https://ssl.pstatic.net/imgstock/upload/research/company/1627526396585.pdf

- Source 3: https://www.digitaltoday.co.kr/news/articleView.html?idxno=594679

- Source 4: http://lakematerials.co.kr/lakematerials/introduction/location

- Source 5: http://eugene.thinkpool.com/itemdiscuss/pdsRead.jsp?name=stock_bbs&mcd=C&ctg=&page=95&slt=&key=&i_max=00116739889999&number=11673896

- Source 6: https://robonews.stockplus.com/articles/858961

- Source 7: http://www.lakematerials.co.kr/lakematerials/business/secondary

- Source 8: https://v.daum.net/v/6L2WvHf5vR?f=p

- Source 9: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20241220000779&docno=&viewerhost=&

- Source 10: https://ssl.pstatic.net/imgstock/upload/research/company/1677026630933.pdf

- Source 11: https://www.thelec.kr/news/articleView.html?idxno=50838

- Source 12: https://contents.premium.naver.com/nomadand/nomad/contents/250224054024703nm

- Source 13: https://www.businesspost.co.kr/BP?command=article_view&num=344913

- Source 14: https://www.judal.co.kr/?view=stockAI&shareToken=v0yBfp1aErSdm2Bf

- Source 15: https://www.judal.co.kr/?view=stockAI&shareToken=rSS7yOdzLWd7FuFr

- Source 16: https://www.judal.co.kr/?view=stockAI&shareToken=EbBgpQtAmXBXVCfR

- Source 17: https://comp.wisereport.co.kr/company/c1010001.aspx?cmp_cd=281740