DEEP RESEARCH · SMEC

SMEC: Mechanics × ICT Convergence and the M&A Re-rating

The Hyundai Wia machine-tool acquisition, a Q3 turnaround signal, and an asymmetric setup created by the SNT Group control fight

0. Bottom line first

In July 2025 SMEC moved into the "Big 2" tier of Korean machine tools by acquiring Hyundai Wia's machine-tool business; a Q3 standalone turn to profit signals a bottom. The near-term volatility comes from the SNT Group control battle, but a full-year contribution from the deal plus scale-driven cost benefits in 2026 set up the multiple re-rating.

1. Identity — Smart Mechatronics

The name SMEC stands for Smart Mechatronics, fusing mechanics, electronics, and ICT into a single platform.

- 1999-06-18: Spun off from the Samsung Heavy Industries machine-tool division — inheriting Samsung's manufacturing know-how and quality systems.

- 2011: Merged with telecom-equipment company NewGrid → completed the "Mechanics + ICT" hybrid structure.

2. Business segments

Machinery

More than 90% of revenue. Machining centers (MCT), CNC lathes, industrial robots, and semiconductor back-end equipment (wafer chip polishers). Four domestic sales offices and dealers in 60+ countries.

ICT

Small in revenue but the differentiator versus pure-play machine builders. IIoT gateways, AI-based cybersecurity, KEPCO AMI and digital TRS for power utilities.

Convergence & R&D

~3% of revenue (KRW 3.4 billion cumulative in Q3 2025) spent on R&D across the Mecha, Convergence, and ICT R&D labs. Government project on discharge/dismantling robotic cells for spent-battery recycling.

Q3 2025 cumulative product mix (KRW million)

| Segment | Item | Revenue | Share |

|---|---|---|---|

| Machinery | MCT (LCV, PCV...) | 44,870 | 41.2% |

| Machinery | CNC lathes (PL, SL...) | 57,697 | 53.0% |

| Machinery | Robots & automation | 2,357 | 2.2% |

| Machinery | Parts & others | 3,992 | 3.6% |

| Machinery subtotal | — | 108,916 | 100.0% |

| ICT | Comms/security | 4,460 | (small share of total) |

Official fact: Source — SMEC Q3 2025 quarterly report and SMEC disclosures.

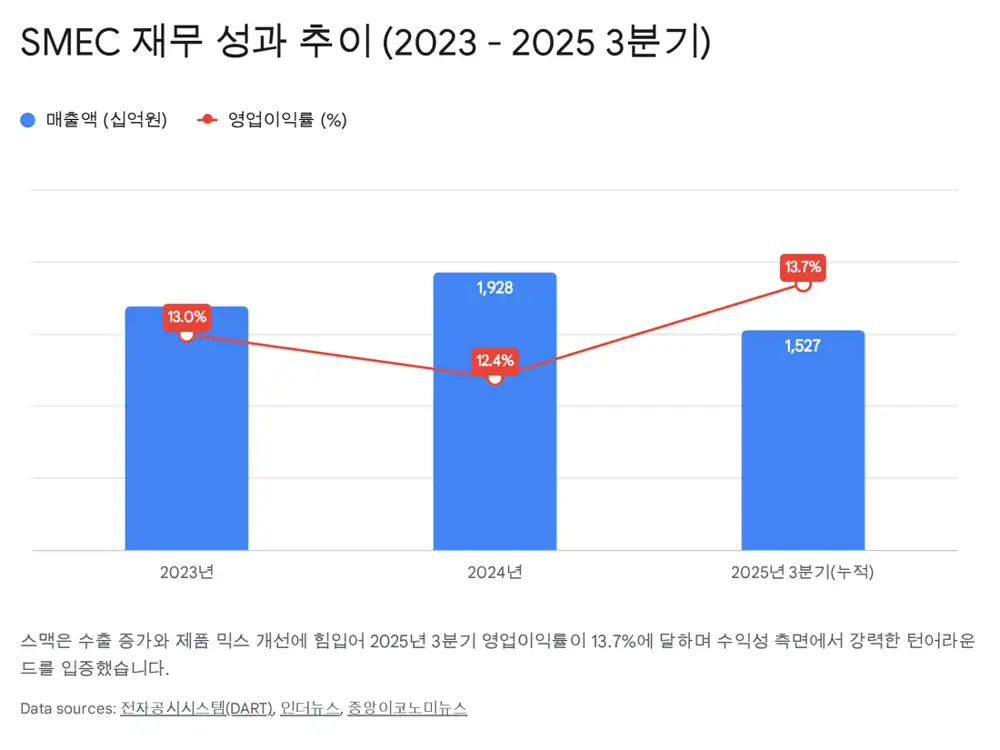

3. Q3 2025 results — bottoming signal

- Cumulative revenue: KRW 113.376 billion (about -25.8% YoY vs. ~KRW 152.7 billion) — high base from the record 2024 plus first-half global manufacturing softness.

- Cumulative operating profit: KRW 2.892 billion.

- Cumulative net profit: KRW 1.214 billion — profitable.

- Q3 standalone: Revenue ~KRW 36.2 billion with a return to net profit, driven by overseas dealer reorders and a higher MCT mix.

- Europe recovery: Germany and Türkiye benefited from eurozone stimulus plus defense/aerospace strength.

- Margin-first ordering: Avoided lowball deals; rebalanced toward higher-margin high-end machines.

Official fact: Q3 debt-to-equity ratio was 122.55%, improved from 132.42% at year-end. Cash fell from KRW 31.6 billion to KRW 4.3 billion — a transient drawdown for the acquisition payment.

4. Acquiring Hyundai Wia's machine-tool unit — the quantum jump

4.1 Domestic share scenario (2023 revenue basis)

| Tier | #1 | #2 (pre-deal) | #2 (post-deal) | #3+ |

|---|---|---|---|---|

| Player | DN Solutions | Hyundai Wia | SMEC + Wia Machine Tools | Hwacheon, etc. |

| Share | ~48.4% | ~26.5% | ~35–40% (est.) | <10% |

| Note | Dominant #1 | Selling the unit | Strong #2 emerges | Gap widens |

4.2 Synergy levers

- Scale: Bargaining power on castings/steel and key components (NC controllers, bearings) → lower COGS.

- Full lineup: SMEC (small/mid MCT, general-purpose CNC lathes) + Hyundai Wia (large automation, automotive powertrain machining) → a Total Solution Provider.

- Global footprint: SMEC (North America/Europe dealers) + Hyundai Wia (HMG global plants — U.S., Mexico, India, Europe) enables cross-selling.

5. SNT Group control battle

Just after closing Hyundai Wia and burning cash, SNT Holdings opened a three-week roller coaster of open-market buying. SNT runs machine-tool and defense-parts businesses via SNT Dynamics (formerly Tongil Heavy Industries).

- 2025-10 — surprise attack: SNT Holdings reached 11.05% and became the largest shareholder.

- Defense: CEO Choi Young-sub's side lifted holdings to 9.75%; SNT side temporarily diluted to 8.67%.

- Counter-attack: SNT added more shares to 14.74%, reclaiming the top-shareholder slot.

Vertical integration / synergy

Combine with SNT Dynamics machine tools; internalize defense-parts machining.

Investment / check on competitor

Without full takeover, participate in governance and push dividend hikes or block initiatives.

AGM vote & buying

Whether SNT continues open-market buying and what comes up for an AGM vote.

Interpretation: Control fights add short-term price momentum but, if drawn out, divert management from core operations and PMI — a real "management distraction" risk.

6. 2026 industry outlook and risks

- "Low first half, higher second half": Domestic machine-tool production is projected to fall ~3.0% in 2026 (per industry trade press). Rate cuts and a re-acceleration of semiconductor/defense capex are the second-half catalysts.

- Trump 2.0: Universal tariffs and America First posture are a potential headwind for SMEC's U.S.-exposed revenue. However, U.S. reshoring lifts on-shore equipment demand — a partial offset.

- China: Chinese builders are eating into the low/mid-range market with both price and rising technology — reinforcing the need to move up via the Hyundai Wia deal.

- End-market shifts: EV demand explodes for large aluminum-part machining (battery cases, motor housings). The semis/AI back-end super-cycle benefits SMEC's wafer-polishing equipment.

7. Valuation and strategy

Combined-entity revenue (legacy SMEC + ~KRW 300bn+ from Wia Machine Tools) compresses 2026 P/S meaningfully. The category shift from "mid-cap machine builder" to "global top-tier machine-tool solutions company" is the structural re-rating argument.

Bull / Base / Bear

- Bull: PMI sticks, Europe/U.S. recovery, control-fight resolves → multiple re-rating accelerates.

- Base: Full-year deal contribution in 2026; 35–40% domestic share; margin improvement.

- Bear: Prolonged control fight (management distraction), U.S. tariffs, Chinese price war, PMI delays.

8. Conclusion

SMEC stands at the start of a structural growth phase. Hyundai Wia = step-up in scale, Q3 turnaround = core-business resilience, control fight = volatility and value re-discovery — track all three together. When 2026 synergies kick in fully, SMEC may end up valued in a different category from today.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224152317392

- SMEC Q3 2025 quarterly report (DART): dart.fss.or.kr — SMEC search

- SnM News (steel/metals industry press): snmnews.com