DEEP RESEARCH · TAESUNG

Taesung 2025-2027 Strategic Analysis

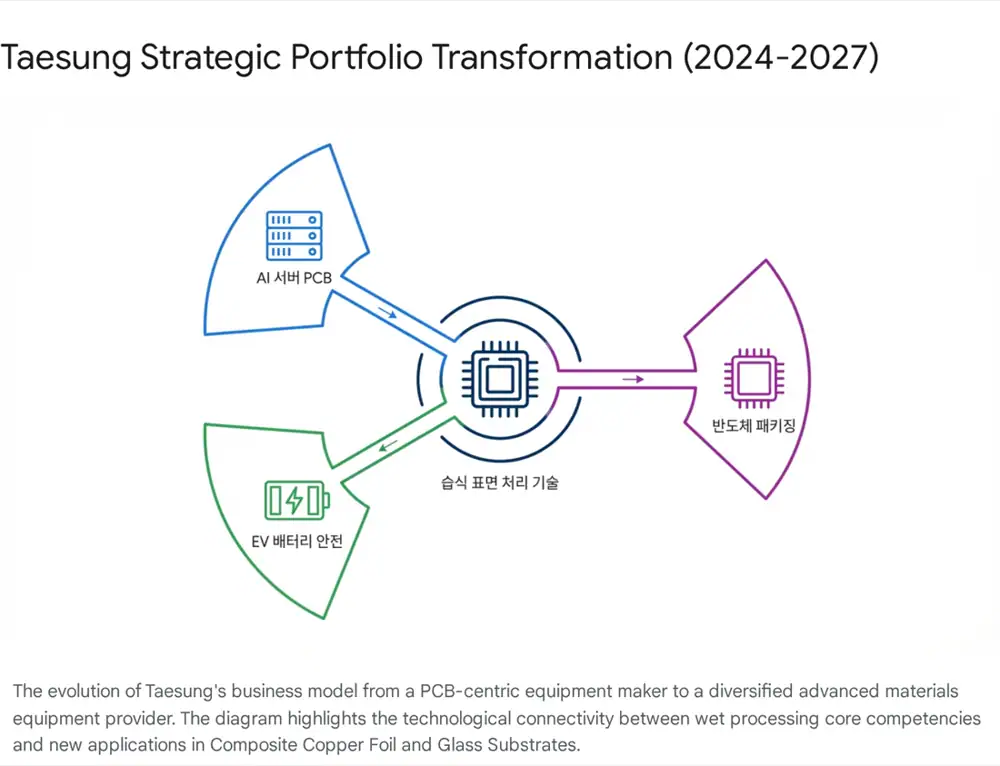

How AI server PCBs, composite copper foil, and glass-substrate equipment can transform a traditional wet-process equipment maker

0. Bottom line first

My read is that Taesung is using its existing PCB wet-equipment cash cow to move into two future bottlenecks: composite copper foil and glass-substrate equipment. 2025 is the buildout year, 2026 is when the new plant and new-business revenue must become visible, and 2027 is when capacity and diversification should be tested.

Official fact: The source states that as of September 30, 2025, Taesung's paid-in capital was KRW 3.05007 billion and shares outstanding were 30,500,730. That is about 18% above year-end 2024 paid-in capital of KRW 2.58907 billion and 25,890,730 shares, while the par value remains KRW 100. The source also cites news that monthly orders in December exceeded KRW 10 billion as a signal of visible top-line growth.

Interpretation: The capital increase reads as preparation for large projects such as the Cheonan new plant, glass-substrate demo equipment, and composite copper foil RTR equipment. Still, new businesses require customer production schedules and yield proof, so order disclosures and plant progress matter.

1. Starting point: from PCB wet equipment to next-generation tools

Taesung, 323280.KQ, is described as a company with more than 20 years of experience in PCB wet-process equipment. The global hardware industry is undergoing simultaneous shifts in AI compute demand, EV battery safety, and semiconductor packaging limits, and Taesung is exposed to equipment demand across all three axes.

Operationally, Taesung's industry category, other special-purpose machinery manufacturing C29299, is order-based and technology-intensive. With high fixed costs, operating leverage can become large once revenue passes breakeven. The source estimates composite copper foil RTR equipment at about $4 million per unit, or roughly KRW 5-6 billion, and expects glass-substrate etching equipment to carry higher margins than legacy PCB tools because of process difficulty.

AI PCB supercycle

AI servers such as GB200 increase demand for HDI and high-layer-count boards. Desmear, surface treatment, and uniform plating become yield bottlenecks.

Composite copper foil RTR

The company targets composite current-collector equipment that plates copper on both sides of PET/PP film for battery safety and lightweighting.

Glass-substrate wet process

In the move toward TGV-based glass cores, etching, stripping, and cleaning tools are presented as core bottlenecks.

2. AI server PCB: the legacy cash cow

NVIDIA Blackwell and GB200 server systems require PCBs with more than 20 layers and ultra-low-loss materials. Fine-circuit reliability between AI chips and mainboards requires higher precision in desmear and surface-treatment processes. The source states that Taesung's vacuum suction and two-fluid spray technologies help remove micro-via contamination and secure uniform plating thickness. Background links include 36Kr AI server article, PCB Directory market article, Rocket PCB article, Creating Nano Technologies post, and ICAPE PCB trends.

Official fact: The source says the global PCB market is projected to reach $94.17 billion by 2032, with AI servers and HPC driving growth. Source link: Printed Circuit Board Market Outlook 2026-2032.

| Category | 2024E | 2025E | 2026E | 2027E | 2028E | CAGR |

|---|---|---|---|---|---|---|

| AI server PCB market | $12.5B | $16.2B | $21.0B | $26.5B | $33.0B | About 27% |

| Average layers | 16-18 | 20-24 | 24-28 | 30+ | 32+ | - |

| Main technology needs | HDI, Low Loss | Ultra-Low Loss | Early TGV adoption | Glass Core | Hybrid | - |

| Relevance to Taesung tools | Precision cleaning | Uniform plating required | Advanced stripping/etching | Dedicated glass-substrate line | Composite process | Very High |

The source argues that leading PCB makers such as ZDT, Samsung Electro-Mechanics, and LG Innotek are entering a CAPEX cycle to expand AI server substrate capacity. Taesung is positioned as a proven first-tier vendor with long customer relationships, giving it an opportunity in new lines and replacement demand.

3. Composite copper foil: battery safety and lightweighting equipment

Composite copper foil is a sandwich structure with thin copper layers on both sides of PET or PP polymer film. Versus conventional electrolytic copper foil, it can reduce copper usage and weight, while the polymer film can melt during an internal short and act as a fuse to reduce thermal-runaway risk. Background links include SMM composite copper foil article, VentureSquare Taesung article, and SMM Taesung equipment article.

Official fact: The source states that the global composite copper foil equipment market is expected to grow from $750 million in 2024 to $1.2 billion by 2033.

Taesung's core technology is roll-to-roll, or RTR, horizontal electroplating. The clamping approach used by many Chinese competitors holds the film edges during transport, which can create uneven edge plating, film tearing, and tension-control problems in ultrathin 4.5µm-6.5µm films. Taesung's RTR method maintains uniform tension across the whole film, performs continuous plating, and can reduce process steps through double-sided plating without auxiliary film. The source cites production speeds above 10m/s.

| Roadmap | Content | Investor checkpoint |

|---|---|---|

| 2025 | Build mass-production line, supply samples/demo tools to global battery makers, complete quality certification | Joint-development agreements and certification results |

| 2026 | Customer certification completed, orders begin, meaningful composite copper foil equipment revenue expected | Order disclosures and revenue recognition |

| 2027 | Standardize RTR plating as a global process and expand customer base in North America and Europe | Customer diversification and possible materials entry |

Interpretation: The attraction of composite copper foil equipment is high ASP and bottleneck resolution. The offsetting risks are customer yield, battery-investment pacing, and exposure to Chinese customers.

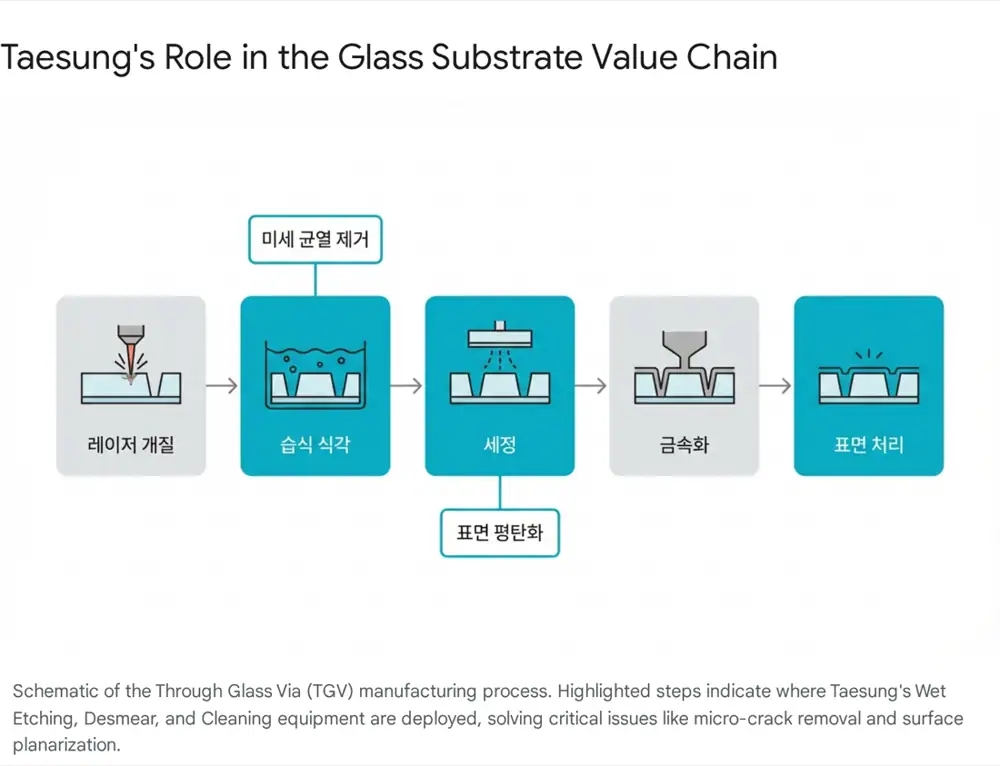

4. Glass substrates: the wet-process bottleneck in advanced packaging

AI and HPC chip performance is exposing limits in organic substrates around fine circuits, thermal management, and large-area packaging. Glass is gaining attention because of surface flatness, low thermal deformation, and low electrical signal loss. Intel and SKC subsidiary Absolics are cited as leaders targeting commercialization in 2026-2030. Background links include 36Kr glass-substrate article, MDPI glass-substrate review, Semiconductor Engineering article, and BusinessWire market report.

Taesung's strength comes from large-area glass-processing know-how in the display industry. Thin and fragile glass must be handled with semiconductor-level precision, and the source argues that Taesung's LCD and OLED glass-processing equipment experience supports competitiveness in etching, stripping, and cleaning.

Official fact: The source states that Taesung is known as the only domestic company able to provide the full wet-process flow for glass substrates, from TGV cleaning to surface etching and stripping, on a turnkey basis. Related post-process cleaning equipment link: VentureSquare cleaning equipment article.

Interpretation: Glass substrates are a post-2026 market-opening theme, so the gap between expectation and actual orders is large. Taesung's demo tests, customer specification finalization, and mass-production equipment schedule are the key evidence for re-rating.

5. Cheonan new plant and three-year roadmap

Taesung is building a new plant in the Cheonan North BIT general industrial complex in Chungcheongnam-do. The source frames it not as simple capacity expansion but as a dedicated production base for composite copper foil RTR plating equipment and glass-substrate manufacturing equipment.

| Item | Source figure | Strategic meaning |

|---|---|---|

| Land | 10,000 pyeong, about 33,000 square meters | Dedicated base for next-generation equipment |

| Gross floor area | 17,000 pyeong | Can separate advanced tools from the legacy Ansan PCB line |

| Completion timing | After June 2026 | Aligned with front-end customer production schedules |

| Annual capacity | KRW 1 trillion | Prerequisite for a step-change in revenue |

| Capacity mix | Composite copper foil KRW 600B, glass substrates KRW 300B, PCB KRW 100B | Numeric basis for a larger new-business mix |

Foundation

Cheonan construction, glass-substrate demo tests, composite copper foil tool specification finalization, and AI server PCB tool orders.

Scale-up

June plant completion and headquarters relocation, glass-substrate equipment aligned with customer mass production, and composite copper foil equipment revenue recognition.

Global expansion

Expand glass-substrate equipment customers to global OSATs and IDMs, standardize RTR plating, and explore direct composite copper foil materials production at a 5GWh target scale.

6. Risks and monitoring indicators

The first risk is delayed technology adoption. Glass substrates and composite copper foil both change existing process standards, so if customer standardization or end-product yield is delayed, equipment orders can also slip. The offsetting argument is that PCB equipment cash flow can fund R&D and waiting time.

The second risk is geopolitics. Since CATL and BYD are referenced as key composite copper foil players, U.S.-China trade tension and IRA issues matter. The source says Taesung is strengthening cooperation with Korean battery makers such as LG Energy Solution and Samsung SDI while seeking North American and European customers to lower China dependence.

The third risk is raw-material volatility in steel, copper, and other inputs. New-plant construction and equipment manufacturing costs can pressure margin. The source argues that high-ASP new tools and customer demand to reduce copper usage can support pricing power.

| KPI | Why it matters |

|---|---|

| Composite copper foil equipment order disclosures | Evidence that demos and certification are converting into orders |

| Glass-substrate demo completion | Proof point for turnkey wet-process competitiveness |

| Cheonan plant progress | Leading indicator for 2026 capacity expansion |

| AI server PCB equipment backlog | Shows whether the cash cow can fund new-business waiting time |

| Customer diversification | Confirms whether China and customer concentration risks are easing |

7. Final read

In sum, Taesung is evolving from a simple PCB equipment maker into a hybrid equipment company that addresses bottlenecks in AI, EV batteries, and semiconductor packaging. 2025 is preparation, 2026 is when the new plant and new-business revenue should become visible, and 2027 tests the KRW 1 trillion capacity vision.

The indicators I would watch most closely are actual orders for glass-substrate and composite copper foil equipment, the Cheonan plant schedule, and AI server PCB equipment backlog. If expectations convert into numbers, a valuation re-rating is possible; if delayed, the stock can be discounted back as a traditional equipment name. A long-horizon approach can make sense, but evidence on orders and capacity should drive the judgment.

Sources

- 네이버 블로그 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224151914685

- 2026: AI Servers to Be Extremely Expensive - 36Kr: https://eu.36kr.com/en/p/3590983777108229

- Global PCB Market to Grow by $26.8 Billion from 2025-2029: https://www.pcbdirectory.com/news/global-pcb-market-to-grow-by-26-8-billion-from-2025-2029-driven-by-rise-of-ai-and-smartphones

- Company Visit: Taesung growth - Asia Economy: https://cm.asiae.co.kr/en/article/2024052916360130504

- Glass Substrates: The Dark Horse in 2026 - 36Kr: https://eu.36kr.com/en/p/3636277088814085

- 태성 AI PCB, 복합동박, 유리기판 재평가 - 뉴스프라임: https://m.newsprime.co.kr/section_view.html?no=713719

- AI technology drives HDI PCB demand - Rocket PCB: https://www.rocket-pcb.com/ai-technology-drives-surge-in-demand-for-high-density-interconnect-pcb-servers-and-storage-devices-lead-a-new-growth-cyc

- Printed Circuit Board Market Outlook 2026-2032: https://www.intelmarketresearch.com/printed-circuit-board-market-21879

- Global Semiconductor Jet Scrubber Market: https://marketpublishers.com/report/industry/other_industries/semiconductor-jet-scrubber-market-gir.html

- PCBs become the unsung heroes of computing power: https://www.creating-nanotech.com/en-US/newsc270-pcbs-become-the-unsung-heroes-of-computing-power-ushering-in-a-golden-decade-for-the-ai-era

- Top 5 Trends in 2025 PCB Market - ICAPE: https://www.icape-group.com/top-5-trends-in-2025-pcb-market/

- Composite Copper Foil Technology - SMM: https://news.metal.com/newscontent/103286780/Composite-Copper-Foil-Technology-Could-Potentially-Revolutionize-Lithium-Batteries

- Taesung supplies composite copper foil materials - VentureSquare: https://www.venturesquare.net/en/1023220/

- Taesung composite copper foil equipment - SMM: https://news.metal.com/newscontent/103692782

- A Review of Glass Substrate Technologies - MDPI: https://www.mdpi.com/2674-0729/4/3/37

- The Race To Glass Substrates - Semiconductor Engineering: https://semiengineering.com/the-race-to-glass-substrates/

- Global Glass Substrates for Semiconductors Market Report 2026-2036: https://www.businesswire.com/news/home/20251009327475/en/Global-Glass-Substrates-for-Semiconductors-Market-Report-2026-2036-with-Profiles-of-35-Players-Including-Absolics-BOE-Corning-Intel-JNTC-KCC-LG-Innotek-LPKF-NEG-Plan-Optik-Samsung-Toppan---ResearchAndMarkets.com

- Taesung semiconductor post-process cleaning equipment - VentureSquare: https://www.venturesquare.net/en/1023152/