DEEP RESEARCH · SK NETWORKS (001740.KS)

SK Networks: From Asset Monetization to "Intelligence Assetization"

KRW 820bn in cash from the SK Rent-a-Car divestiture + Upstage/En-core AI value chain — the SKN 3.0 re-rating thesis

0. Bottom line first

SK Networks sits in the transition from "undervalued asset stock" to "AI growth stock." The SK Rent-a-Car divestiture released ~KRW 820 billion of cash and removed the balance-sheet anchor; an AI flywheel of En-core (data), Upstage (intelligence), and SK Intellix/Speedmate/Walkerhill (services) is in place. The market still values the name at the ~0.4× P/B of a trading-and-rental conglomerate.

Official fact: The note rates BUY with a target price of KRW 8,500 vs. the as-of-writing price of KRW 4,285 (2026-01-13), implying +98.4% upside.

Interpretation: The asymmetric opportunity hinges on the Upstage stake being marked to market via IPO, plus shareholder returns funded by 12.35% treasury shares and the remaining divestiture cash.

1. SKN 1.0 → 3.0: identity evolution

2. Governance and shareholder structure

| Shareholder | Stake | Strategic meaning |

|---|---|---|

| SK Inc. (largest) | ~43.90% | Alignment with the SK Group "Deep Change" strategy and SKT collaboration potential |

| National Pension Service | ~5.15% | Stewardship-code overseer of governance |

| Treasury shares | ~12.35% | Optionality for cancellation, swap, or M&A funding |

Official fact: In February 2024 SK Networks stated a policy that treasury shares — except those reserved for investment purposes — will be cancelled immediately upon repurchase. Cap-table figures are as of end-September 2025.

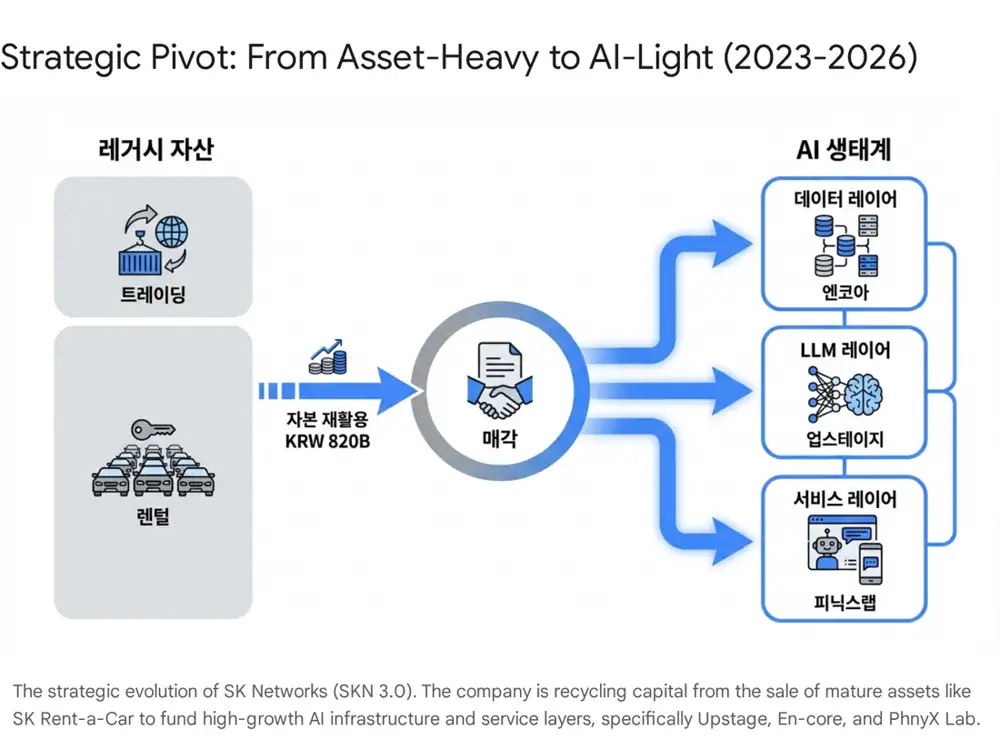

3. The reality of SKN 3.0

3.1 The liquidity event and capital reallocation

In 2024 SK Networks sold 100% of SK Rent-a-Car to Affinity Equity Partners for about KRW 820 billion. The exit cleared a debt-dependent asset-heavy business, improved gearing, and built the war chest for AI investments and shareholder returns. External outlets pegged the deal at roughly USD 591m / USD 572m.

3.2 The data-intelligence-service triumvirate

En-core

Acquired in 2023. Data governance, cleansing and warehousing. Demand for "AI Readiness" in the generative-AI age is driving YoY growth even in a soft macro — the "refinery" that turns enterprise data into AI assets.

Upstage & PhnyX Lab

External (Upstage) plus internal (PhnyX Lab in Silicon Valley). PhnyX, anchored by Stanford-trained researchers, raised a USD 4m seed on its pharma/biotech generative-AI agent "Cheiron."

SK Intellix · Speedmate · Walkerhill

The former SK Magic rebranded as SK Intellix — a "wellness robotics" company. In 2025 it launched NAMUH X, an autonomous home robot. Speedmate spun off in September 2024 and partners with Germany's DAT for AI maintenance data. Walkerhill applies AI to hospitality.

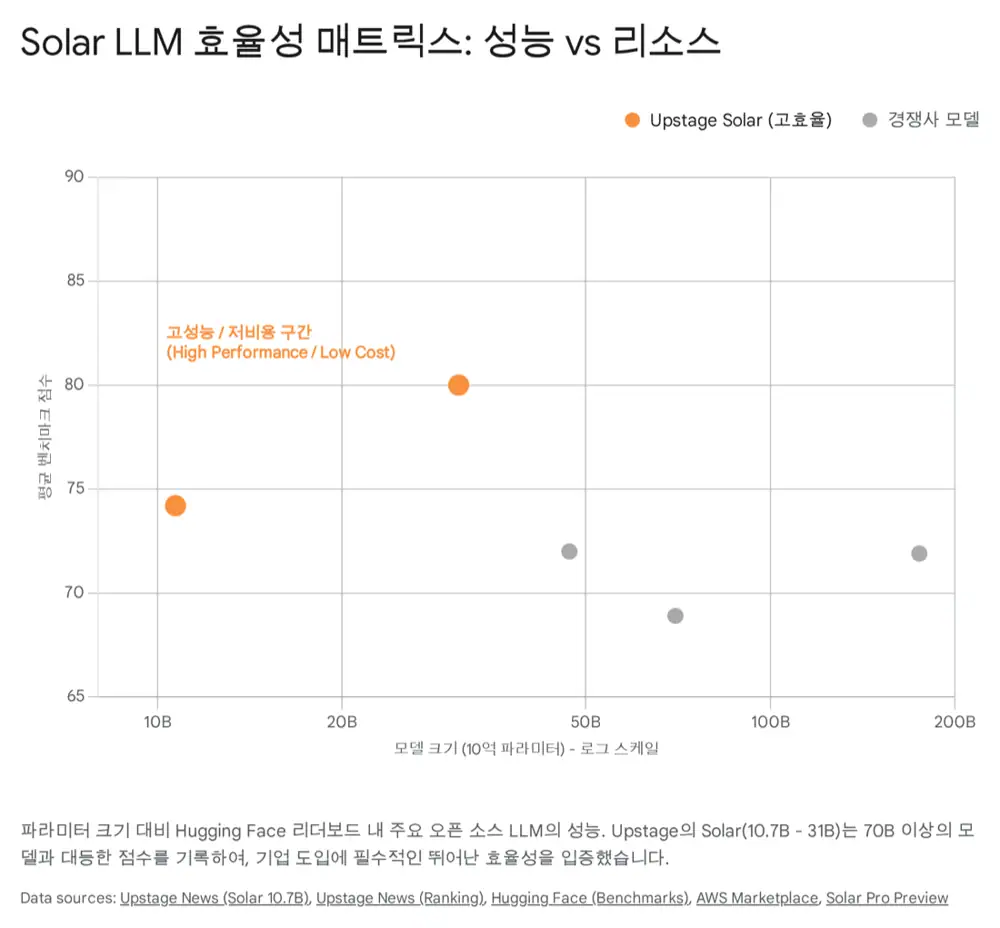

4. Upstage — the portfolio's alpha

SK Networks led Upstage's Series B with about KRW 25 billion — a strategic alliance, not just a financial check.

4.1 "Solar" — an efficiency moat

- Proprietary Depth-Up Scaling (DUS) let 10.7B–31B-parameter models match or beat far larger models such as Meta's Llama 2 70B.

- Solar topped Hugging Face's Open LLM Leaderboard.

- Solar Pro 2 runs on a single GPU — attractive to cost-sensitive enterprises.

- Strong Korean/Japanese capability and an on-premise deployment option ride the "Sovereign AI" trend.

4.2 Valuation timeline

| Round | Size | Notes |

|---|---|---|

| Series B (2024-01/04) | USD 72m (~KRW 100bn) | SK Networks led; valuation roughly KRW 400bn |

| Series B bridge (2025-08) | USD 45m (~KRW 62bn) | Amazon and AMD joined as strategic investors; post-money ~KRW 790bn; cumulative ~KRW 200bn |

| Pre-IPO (2025–) | ~KRW 400bn | Target valuation KRW 1.3tn–KRW 2tn |

| IPO outlook (2026) | — | Market cap KRW 2tn–3tn+; potentially Korea's first generative-AI unicorn listing |

4.3 Marking SK Networks' stake

~KRW 56.1bn

KRW 790bn × 7.11% (stake as of Dec 2024). ~2.2× the KRW 25bn original cost.

~KRW 213.3bn

KRW 3tn target market cap × 7.11%. ~8.5× cost basis.

AWS · AMD alliance

AWS Trainium/Inferentia + AWS Marketplace distribution; AMD reduces NVIDIA dependence.

5. The AI flywheel

| Layer | Owner | Role | Synergy |

|---|---|---|---|

| Data | En-core | Governance, cleansing, integration | High-quality AI training data + consulting revenue |

| Intelligence | Upstage | Solar LLM, Document AI | Proprietary model + licensing/subscription revenue |

| R&D Hub | PhnyX Lab | Vertical-specific AI agents | Frontier tech internalization, new verticals |

| Service | Walkerhill · Speedmate · SK Intellix | AI hospitality · predictive maintenance · wellness | Operational efficiency, real-world data feedback |

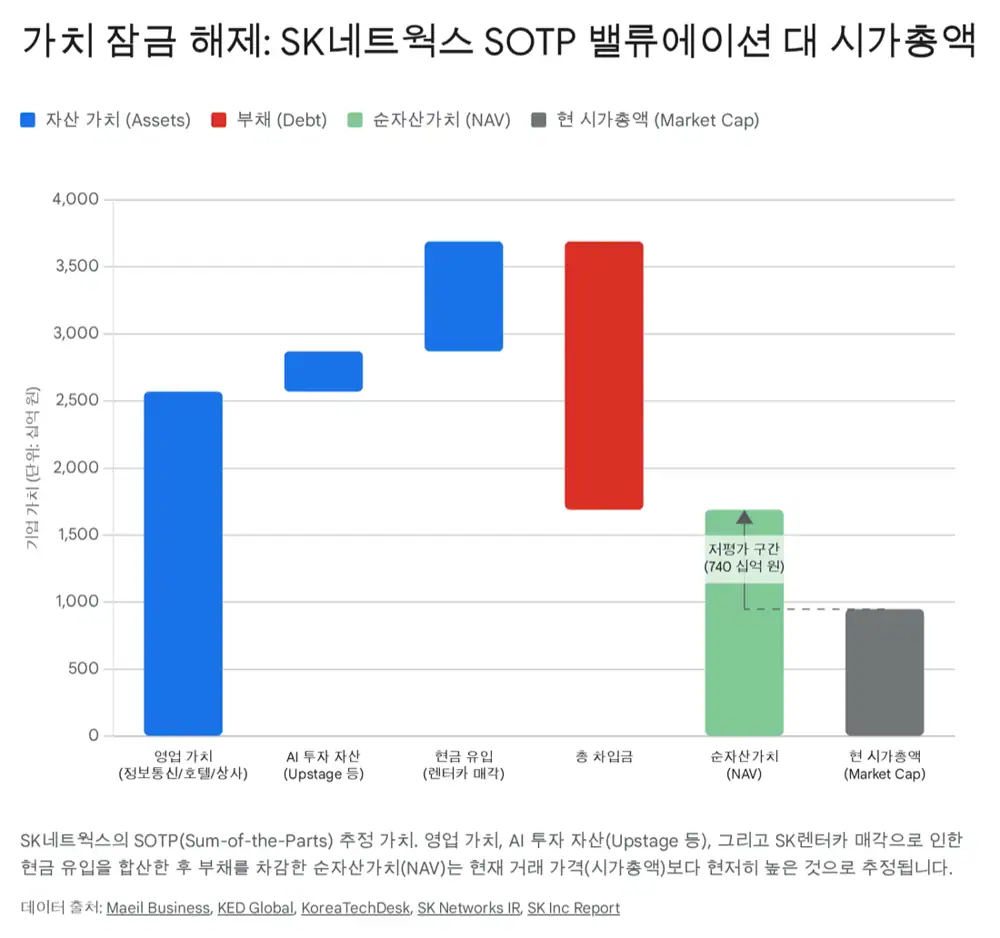

6. SOTP valuation

Today's market cap of about KRW 950 billion reflects only the divestiture cash (KRW 820 billion) plus a sliver of the operating value. A sum-of-the-parts build-up shows the gap.

| Bucket | Component | Method | Value (KRW bn) |

|---|---|---|---|

| Operating | Info-comms | 12MF NI × P/E 10 | 500–600 |

| Operating | Walkerhill | Peer EV/EBITDA 12× | 600–700 |

| Operating | Speedmate | Peer / post-split | 150–200 |

| Operating | Trading (Glowide) | Book / liquidation | 200–300 |

| Investment | Upstage (7.11%) | Assumed market cap KRW 2.5tn | ~180 |

| Investment | En-core | Acquisition + premium | 100–120 |

| Investment | Other (PhnyX etc.) | Book + premium | 100 |

| Treasury | — | Market value | ~120 |

| Net cash | Rent-a-Car proceeds | (+) | +820 |

| Gross debt | — | (-) | (2,000) |

| NAV | — | — | 1,600–1,900 |

| Market cap | at KRW 4,285 | — | ~948 |

| Discount | — | — | ~40–50% |

Interpretation: The market is paying for cash and a slice of operating value. AI portfolio optionality is essentially unpriced — visible monetization should compress the holding discount.

7. Catalysts and risks

Re-rating catalysts

- Upstage IPO (planned 2026): Marks the stake to market and erodes the holding discount.

- Shareholder-return enhancement: Concrete announcements on treasury cancellation or special dividends.

- 2026 operating profit target KRW 700bn: Operating-leverage proof point from AI in the core businesses.

Risks

- Execution risk: Transforming a trading-house culture into an AI company is hard; PMI failure caps synergies.

- Upstage valuation volatility: AI multiples are sensitive to rates and sentiment; IPO delays or down-rounds are possible.

- Capital-allocation risk: Cash deployed into low-return assets or group-support spending could deepen the Korea discount.

8. Conclusion

The Rent-a-Car exit unshackled the balance sheet and the Upstage/En-core stack adds a real growth engine. With Amazon and AMD validating Upstage and ample dry powder on hand, this is the moment to bet on the structural change. The KRW 8,500 target reflects compression of the excess discount and visible AI returns — about +98% upside from the current price.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224149999768

- KED Global — Affinity to buy Korea's No. 2 car leasing firm: kedglobal.com

- KED Global — Affinity to buy SK Rent-a-Car at $572m: kedglobal.com

- SK Networks IR — Stock prices: sknetworks.co.kr

- Dealsite — treasury cancellation: dealsite.co.kr

- SK Networks Governance: sknetworks.co.kr

- Korea Herald — AI investment firm goal: koreaherald.com

- Korea Times — Use of $617m: koreatimes.co.kr

- SK Networks Newsroom: sknetworks.co.kr

- PR Newswire — PhnyX Lab seed: prnewswire.com

- SK Speedmate: sknetworks.co.kr

- KED Global — SK Networks 2026 profit target: kedglobal.com

- Dealsite — Upstage KRW 25bn investment: dealsite.co.kr

- Upstage — Solar 10.7B global #1: upstage.ai

- Chosun English — Upstage tops Japanese leaderboard: chosun.com

- PR Newswire — Upstage $72m Series B: prnewswire.com

- PR Newswire — Upstage $45m bridge: prnewswire.com

- Tracxn — Upstage profile: tracxn.com

- KoreaTechDesk — Upstage IPO outlook: koreatechdesk.com

- Dealsite — Upstage KRW 2tn pre-IPO: dealsite.co.kr

- Namuwiki — Upstage: namu.wiki

- MK — SK Networks KRW 25bn AI investment: mk.co.kr

- MK — Speedmate spin-off plan: mk.co.kr