DEEP RESEARCH · Ford-BYD Battery Supply Chain

Ford and BYD: What Ford’s Battery Reset Means for Korea

A review of EV demand weakness, OBBBA, LFP economics, and Korean battery strategy.

0. Bottom line first

Ford’s move is not simply the end of the Korean battery alliance. It is a supply-chain redesign driven by the EV chasm, OBBBA, and LFP cost advantage. Korean makers need price, product breadth, and local operating flexibility, not only NCM technology.

1. Why the strategy changed

Official fact: The source gives Ford Model e’s 2025 operating loss at about USD 5.5bn, roughly KRW 7.5tn. North American and European EV demand cooled from late 2024, and Ford shifted weight toward HEV and EREV.

Interpretation: Jim Farley’s China visits exposed the cost efficiency, digital ecosystem, cell-to-body integration, and vertical integration of BYD, Xiaomi, and Zeekr.

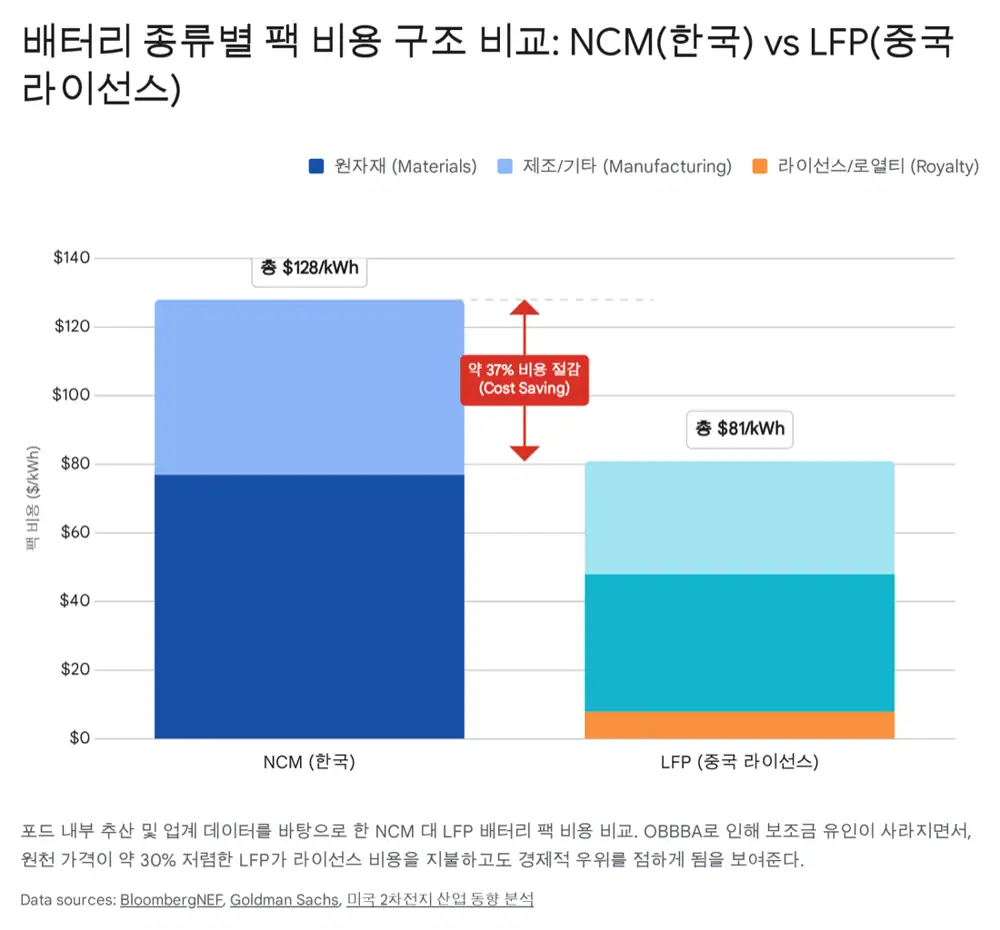

LFP edge

LFP packs are presented at about USD 80/kWh versus USD 110-130/kWh for NCM.

Model e deficit

The roughly USD 5.5bn 2025 loss forced an EV reset.

Operating control

Ford wanted the ability to pivot lines toward ESS and LFP.

2. Friction with Korean suppliers

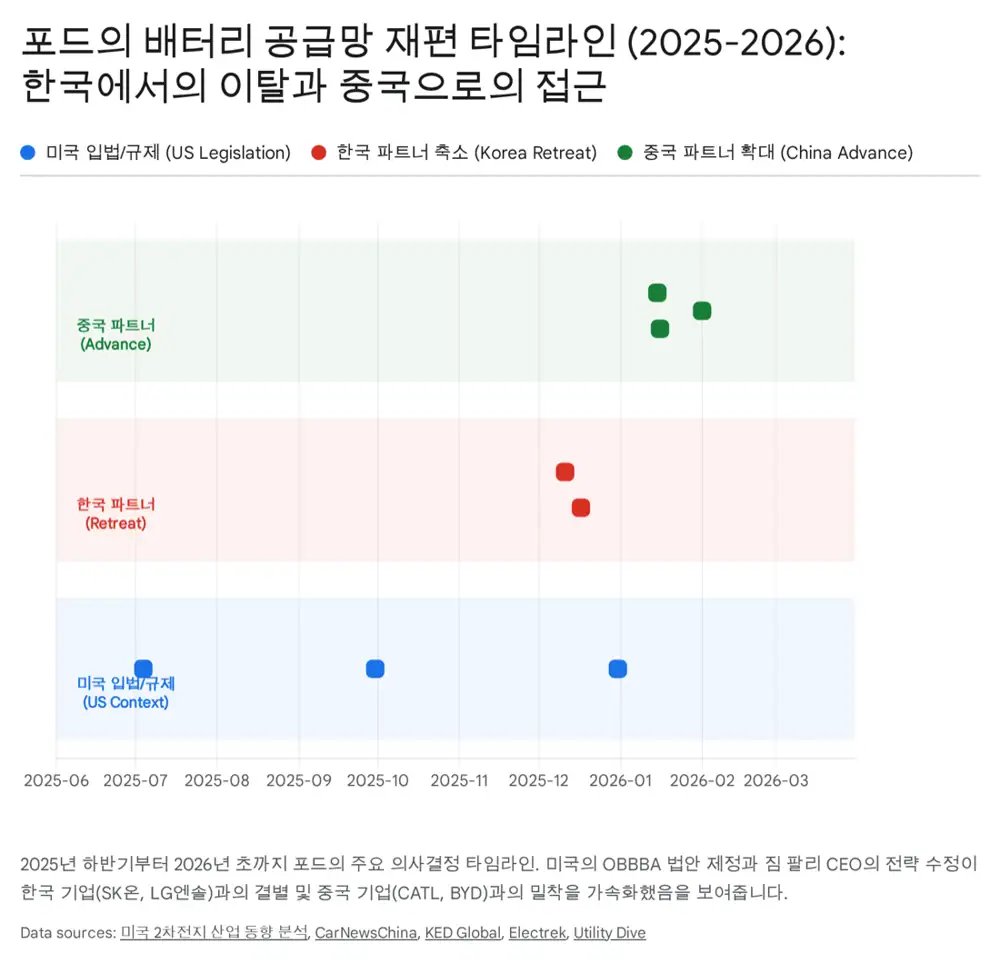

Official fact: BlueOval SK involved USD 11.4bn and three plants in Kentucky and Tennessee, but the source says it effectively moved toward dissolution in late 2025. Ford sought control of the Kentucky plant to secure operating flexibility.

- SK On: yield, skilled labor, equipment optimization, chemical leakage, and stoppages are cited as trust issues.

- LG Energy Solution: the Türkiye JV and E-Transit battery volume cancellation are mentioned.

- For commercial vehicles and affordable EVs, low-cost LFP is judged more suitable than premium NCM.

3. CATL and BYD by market

Official fact: BlueOval Battery Park Michigan is described as 100% Ford-owned, with CATL providing licensing, equipment, and operating support. As of January 2026 reports, Ford was in talks with BYD for HEV/PHEV batteries in Türkiye and Europe.

4. OBBBA and Korean battery tasks

Official fact: The OBBBA signed on July 4, 2025 is described as eliminating the IRA 30D EV purchase credit of up to USD 7,500 from September 30, 2025 and strengthening PFE rules. The source reads the pre-July 2025 technology-license grandfather clause as support for Ford-CATL.

| Task | Content | Meaning |

|---|---|---|

| Customer diversification | Tesla, Hyundai, Toyota, Mercedes-Benz | Reduce Ford dependence |

| Product expansion | Mid-nickel, LFP, high-voltage mid-nickel | Address affordable demand |

| ESS | Data centers and renewables | Protect utilization in EV slowdown |

5. My conclusion

Ford’s China strategy is a gray-zone survival design. Korean battery makers must defend through cost innovation, broader product lineups, and ESS flexibility.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224149818732

- Source 2: https://www.claimsjournal.com/news/national/2025/09/30/333258.htm

- Source 3: https://insideevs.com/news/782099/ford-ev-reset-multibillion-dollar-hole-battery-industry/

- Source 4: https://ev.com/news/ford-ceo-jim-farley-warns-company-cant-miss-china-as-tech-gap-widens

- Source 5: https://www.carscoops.com/2025/02/fords-ceo-says-china-is-10-years-ahead-of-us-in-ev-batteries-needs-to-access-their-ips/

- Source 6: https://www.utilitydive.com/news/ford-skon-dissolving-blueoval-sk-ev-battery-joint-venture/808012/

- Source 7: https://electrek.co/2025/12/11/ford-sk-on-kill-massive-us-battery-joint-venture-split-factories-between-them/

- Source 8: https://www.whas11.com/article/news/local/blueoval-sk-union-vote-plant-closure/417-8511521f-7cd5-4c18-815a-5475c1c81d44

- Source 9: https://www.reddit.com/r/Louisville/comments/1pnk9p2/ford_will_lay_off_all_1600_kentucky_battery_plant/

- Source 10: https://ev.com/news/ford-battery-plant-shift-leaves-kentucky-community-hopeful-but-uneasy

- Source 11: https://www.wkyufm.org/news/2025-12-15/blueoval-sk-in-kentucky-is-out-of-the-ev-battery-business-and-will-lay-off-entire-workforce-as-ford-announces-restructuring

- Source 12: https://www.reddit.com/r/Louisville/comments/1pk449t/ford_ends_sk_on_partnership_takes_full_control_of/

- Source 13: https://www.kedglobal.com/batteries/newsView/ked202512170012

- Source 14: https://media.ford.com/content/fordmedia/feu/en/news/2023/02/21/ford--lg-energy-solution--and-koc-holding-to-establish-a-joint-v.html

- Source 15: https://www.electrive.com/2025/12/18/after-strategy-shift-ford-cancels-battery-order-with-lges/

- Source 16: https://electrek.co/2026/01/15/ford-battery-deal-byd-evs/

- Source 17: https://www.fromtheroad.ford.com/us/en/articles/2025/ford-owned-american-battery-plant-future-electric-vehicles

- Source 18: https://www.evinfrastructurenews.com/ev-technology/bloomberg-nef-lithium-ion-battery-pack-prices-drop-worldwide-ev-applications-hit-by-higher-materials-cost

- Source 19: https://www.billbrownford.net/ev-charging/new-ford-lfp-battery-will-make-evs-more-affordable-accessible/

- Source 20: https://carnewschina.com/2026/01/16/ford-in-talks-with-byd-for-battery-supply-deal/

- Source 21: https://www.gurufocus.com/news/4114932/ford-in-talks-to-source-byd-batteries-for-overseas-plants

- Source 22: https://trendsresearch.org/insight/byds-1-billion-investment-in-turkiye-a-catalyst-for-electric-vehicle-growth-and-industry-transformation/

- Source 23: https://www.just-auto.com/news/ford-byd-hybrid-battery-supply/

- Source 24: https://www.autoblog.com/news/ford-in-talks-with-byd-for-its-next-gen-hybrids

- Source 25: https://drive.google.com/open?id=1cwe-_DbCuHbBMdJjETmuyTz9AQCgzzEbilWKAN-aeuQ

- Source 26: https://www.mwe.com/insights/the-one-big-beautiful-bill-act-navigating-clean-energy-tax-credits-in-a-new-era/

- Source 27: https://www.rebiogroup.com/post/insight-battery-industry-changes-triggered-by-the-one-big-beautiful-bill-act-obbba

- Source 28: https://news.gm.com/home.detail.html/Pages/news/us/en/2025/may/0513-GM-LG-Energy-Solution-pioneer-LMR-battery-cell-technology.html

- Source 29: https://insideevs.com/news/757794/ford-breakthrough-lmr-ev-battery-chemistry/

- Source 30: https://www.koreaherald.com/article/10563938

- Source 31: https://www.spglobal.com/ratings/en/regulatory/article/credit-faq-the-us-changes-policies-the-korean-battery-firms-change-strategy-s101653182