DEEP RESEARCH · Alteogen

Alteogen: 2026 as the Year of Keytruda SC Royalties and Platform Expansion

A combined view of ALT-B4, Keytruda SC, new licensing, Tergase, Eyluxvi, and patent-litigation risk.

0. Bottom line first

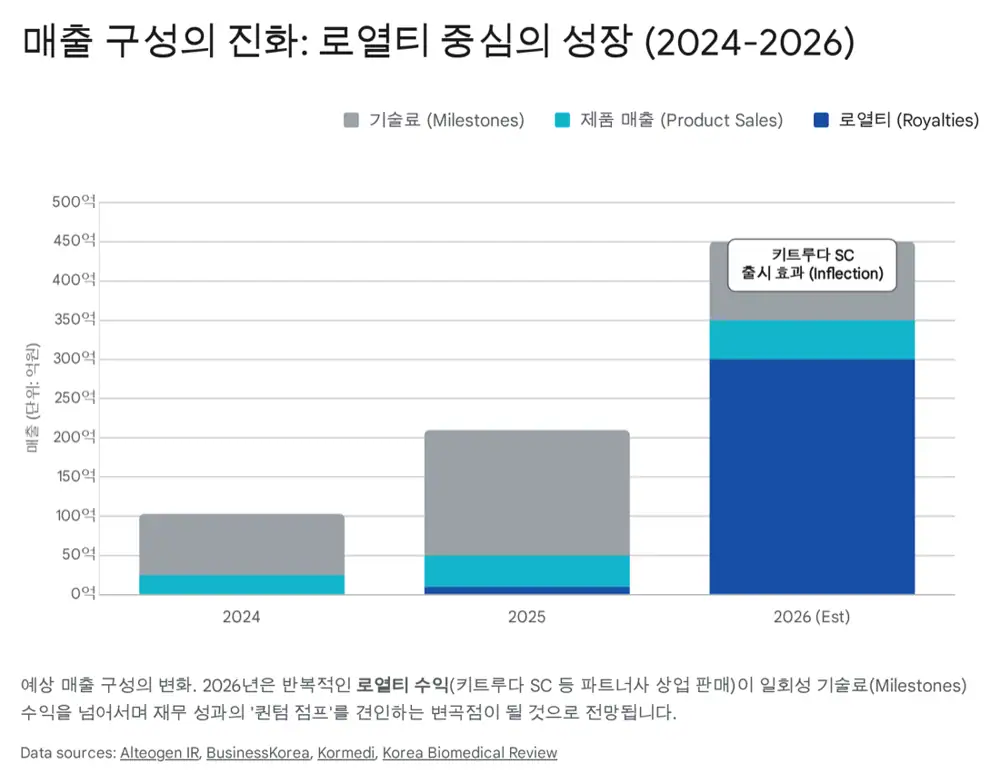

The source defines 2026 as Alteogen’s “year of commercial realization.” If 2025 was the year of regulatory approval and technical validation, 2026 is when Keytruda SC royalties, new licensing, and proprietary-product revenue are expected to become visible in numbers.

Official fact: The source presents Merck/MSD’s Keytruda SC commercialization, Hybrozyme platform expansion, Tergase and Eyluxvi, and the Halozyme patent dispute as the key 2026 variables.

Interpretation: My key issues are Keytruda SC penetration in the U.S. and Europe, the royalty structure estimated at about 5% of net sales, the possibility of a new trillion-won-scale license-out, and whether German/EPO patent proceedings slow actual launch speed.

1. From IV to SC: why Alteogen’s technology matters

The global biologics market is shifting from intravenous injection to subcutaneous injection. Patient convenience, lower chair time, healthcare-cost savings, and originator patent-defense strategies are all working together.

Official fact: The source says existing IV formulations require more than 30 minutes of dosing and preparation in hospitals under medical-supervision. ALT-B4-applied SC formulations are presented as cutting dosing time to within 1-5 minutes.

2. Keytruda SC: start of 2026 royalty economics

| Item | Source content | Meaning |

|---|---|---|

| U.S. approval | Merck received FDA approval for Keytruda QLEX in September 2025 | 2026 becomes the first full year of U.S. sales ramp |

| Europe approval | European Commission approved Keytruda SC in November 2025 | Country-level pricing and reimbursement in Germany, France, and others become watch points |

| Market weight | The U.S. accounts for about 60% of global Keytruda sales | U.S. early penetration determines Alteogen royalty scale |

| Royalty | Market analysts estimate Alteogen royalties at about 5% of net sales | High-margin royalty revenue can change the earnings structure |

| Switching target | The source says Merck targets switching 30-50% of Keytruda patients to SC | SC conversion rate is the key sensitivity |

Official fact: The source says 2024 Keytruda sales exceeded about USD 25bn and are expected to keep growing through 2028. It presents a scenario in which a 2026 SC conversion rate of 10-20% could mean billions of dollars in SC revenue and hundreds of billions of won in royalties for Alteogen.

3. Halozyme patent dispute: the key risk

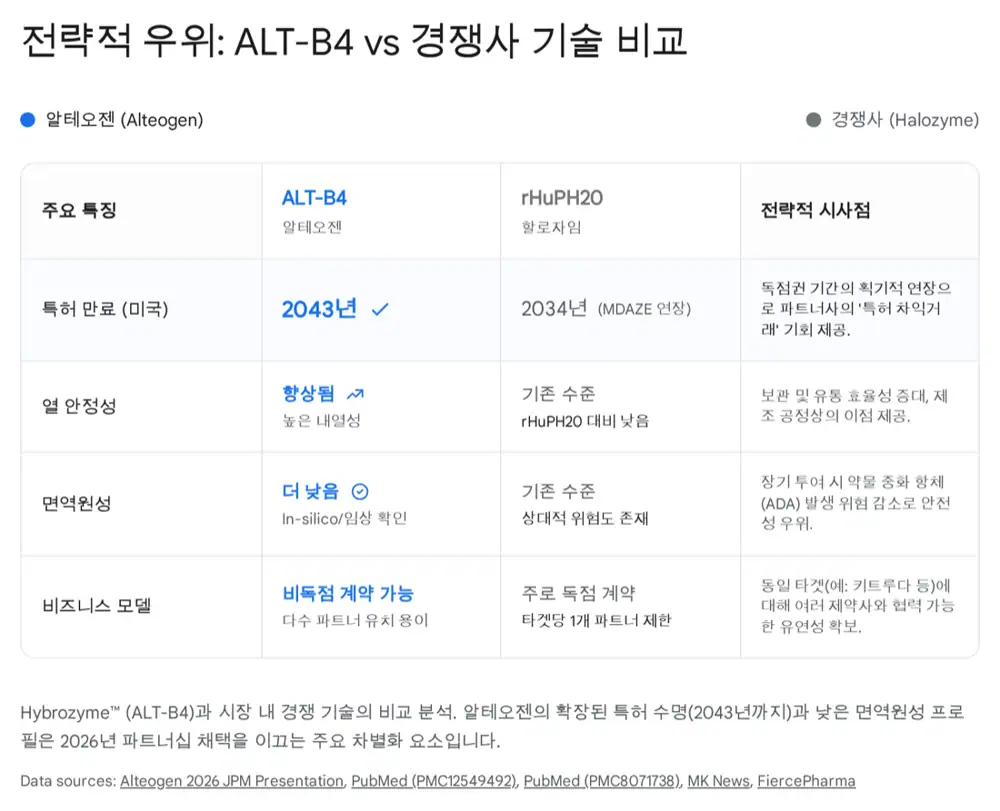

Official fact: The source says Halozyme claimed infringement of European patent EP 2 797 622 and obtained a preliminary injunction from a German court. Merck is appealing and pursuing invalidation, and the source expects possible outcomes from the German appellate court and European Patent Office procedures in 2026.

Interpretation: Alteogen’s defense logic is that ALT-B4 has a different polypeptide sequence from Halozyme’s rHuPH20 and is differentiated in areas such as thermal stability. The dispute can affect European launch speed and investor sentiment, but if the technical distinction is legally recognized, it may strengthen platform value.

4. Hybrozyme platform expansion

Potential trillion-won contract

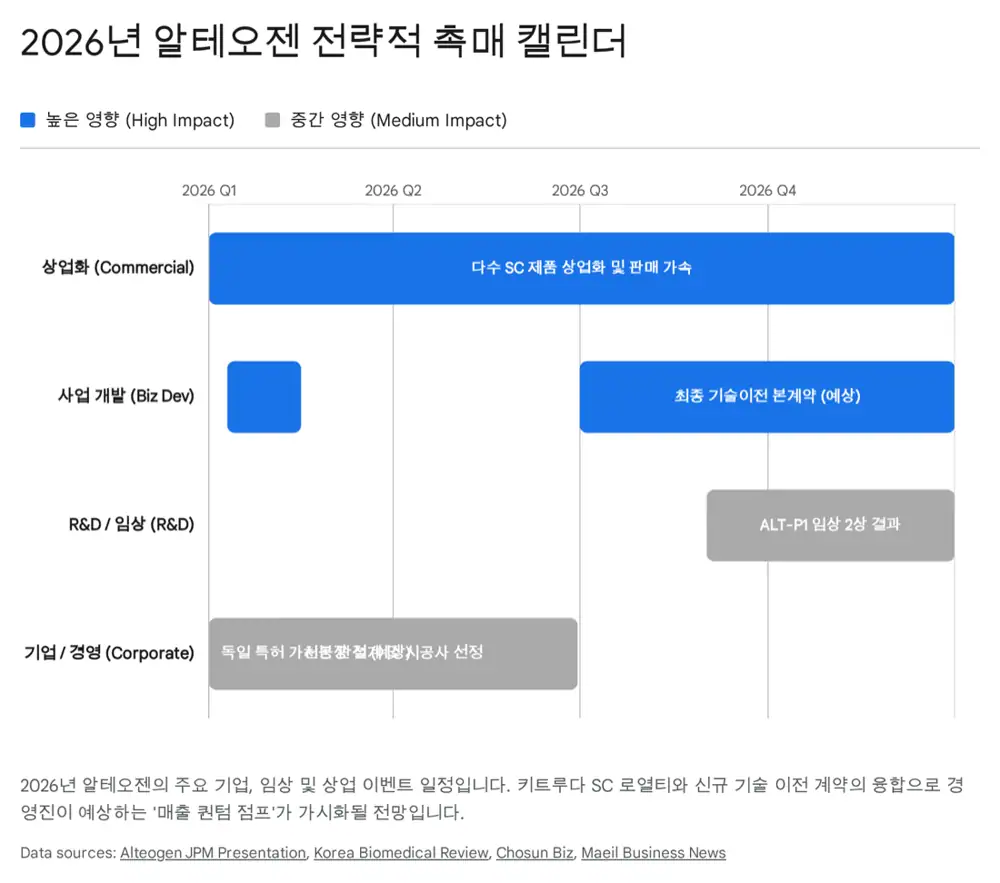

The source says CEO Tae Yeon Jeon suggested at the January 2026 J.P. Morgan Healthcare Conference that a new technology-transfer deal was in final coordination.

ALT-B4 patent to 2040

The source frames “patent arbitrage” as a pharma incentive: key Halozyme patents expire between 2027 and 2034, while ALT-B4 patents last until 2040.

Daiichi Sankyo and AZ

Enhertu SC and Imfinzi SC progress would test platform repeatability after Keytruda.

| Partner/product | Source content | 2026 watch point |

|---|---|---|

| New big-pharma L/O | Based on prior Merck and AstraZeneca contract sizes, from about USD 135m to several billion dollars, the source sees potential for a large deal | Partner, total size, exclusivity, and target product |

| Daiichi Sankyo / Enhertu SC | Exclusive license for Enhertu SC development signed in late 2024 to early 2025 | Development milestones such as phase 3 entry and related fee inflows |

| AstraZeneca / Imfinzi SC | SC formulation development for immuno-oncology drugs such as Imfinzi | Clinical data, transition toward filing preparation, and additional milestones |

5. Proprietary pipeline and products

| Product/pipeline | Source content | Meaning |

|---|---|---|

| ALT-P1 | Global phase 2 readout in pediatric growth hormone deficiency expected in 2026 | NexP fusion-based biobetter improving daily growth hormone into weekly dosing |

| ALT-P1 competition | Compared with Pfizer’s Ngenla, Ascendis Pharma’s Skytrofa, and Novo Nordisk’s Sogroya | Key is proving annual height velocity comparable to Genotropin plus convenience |

| Eyluxvi / ALT-L9 | European Commission approval in November 2025, European launch planned for 2026 | Addresses both Eylea 2mg and high-dose 8mg markets |

| 8mg patent | Filed formulation-technology patent in January 2026 for the high-dose Eylea market | Lifecycle strategy for a competitive biosimilar market |

| Tergase | Standalone recombinant hyaluronidase. The source says it launched domestically in May 2025 and completed MFDS approval in November | Expansion into pain management, aesthetic filler correction, and ophthalmic surgery support based on higher purity and lower immunogenicity than animal-derived products |

6. Governance and financial strategy

KOSPI transfer push

The source says Alteogen is pursuing a transfer from KOSDAQ to KOSPI in 2026 and selected Korea Investment & Securities as underwriter.

GMP production facility

CEO Tae Yeon Jeon presented a vision to secure GMP-level in-house production by 2030, with design, contractor selection, and equipment orders expected in H1 2026.

KRW 151.4bn Q3 2025 cumulative sales

The source cites KRW 87.3bn operating profit and a swing to profit, and says 2026 sales could exceed the KRW 500bn range according to market consensus.

Official fact: The source presents the in-house production-facility investment at about USD 150m-200m. The purpose is to reduce CDMO dependence and improve production efficiency for proprietary products such as Tergase and the Eylea biosimilar.

7. Risk factors

- Halozyme patent litigation: the German preliminary injunction can temporarily slow Keytruda SC launch in Europe, and Merck’s appeal plus invalidation proceedings can create H1 2026 volatility.

- Intensifying competition: growth hormone and Eylea biosimilar markets already have many competitors, so ALT-P1 and Eyluxvi need superior clinical data and marketing strategy.

- Switching-rate risk: the Keytruda SC royalty scenario is sensitive to conversion speed among patients, physicians, and payers.

- CAPEX execution risk: if the USD 150m-200m in-house production investment grows or is delayed, cash-flow pressure can increase.

8. My conclusion

In 2026, Alteogen will be tested on whether “possibility” turns into “earnings.” If Keytruda SC penetrates quickly in the U.S. and Europe, a royalty-based profit structure opens up; if new licensing and Enhertu/Imfinzi SC follow, platform repeatability is proven. The first risks to watch are the Halozyme case and the actual SC conversion rate.

Sources

- Source 1: Naver Blog original

- Source 2: Keytruda Market Size - Grand View Research

- Source 3: Keytruda SC FDA approval and Europe obesity drug battle

- Source 4: European Commission approves subcutaneous Keytruda

- Source 5: Halozyme preliminary injunction against Merck Keytruda SC

- Source 6: Alteogen licensing after Keytruda SC clearance

- Source 7: Keytruda subcutaneous injection receives FDA approval

- Source 8: Alteogen royalty windfall article

- Source 9: Alteogen response to Halozyme patent challenge

- Source 10: Alteogen trillion-won ALT-B4 export deal article

- Source 11: Alteogen export deal announcement article

- Source 12: MSD patent filing article

- Source 13: Daiichi Sankyo SC Enhertu licensing article

- Source 14: ALT-BB4 phase 1 study

- Source 15: JPM 2026 Alteogen CEO interview

- Source 16: Alteogen Q3 sales surge article

- Source 17: Alteogen stock data - Eulerpool

- Source 18: Alteogen stock data - Stockopedia